September 2020

This UK regulatory round-up provides insights on where the agenda is heading and implications for firms. As we move beyond the pandemic and as the post-Brexit landscape takes shape, we track the direction of UK regulation and highlight key developments.

Two sides of the same conduct coin…

This update is heavily weighted towards conduct matters, reflecting the volume of updates published with a conduct angle this period. It also covers broader regulatory framework topics, as well as on-going topics relating to COVID-19 and the UK's withdrawal from the EU.

The latest conduct papers issued by the FCA cover both aspects relating to conduct: ensuring firms have the correct awareness, expertise, processes and procedures in terms of determining and deploying an appropriate conduct culture while ensuring that customers are receiving appropriate outputs in terms of the outcomes they experience. To illustrate the point, the two most impactful papers this period are the FCA's “5 Conduct Questions” paper and its Call for Input on the retail investment sector. Whilst both are designed to achieve the same objective, the 5 Conduct Questions paper looks at firms' inputs to generating an appropriate culture and conduct, whereas the Call for Input focuses more on the outcomes experienced by the end customer.

Highlights featured in this update:

- More to do on conduct and culture

- High Court finds in favour of business interruption insurance policyholders

- FCA proposed significant changes to how General Insurers price products

- Championing customer outcomes: from football to financial resilience

- COVID-related measures: arrivals and departures

- Maintenance of the regulatory framework

More to do on conduct and culture

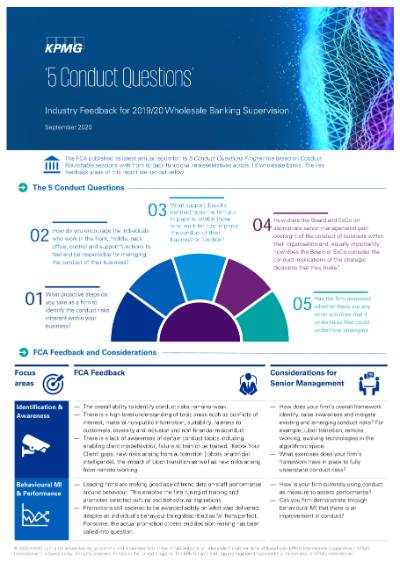

The FCA has released it latest ”5 Conduct Questions” findings (PDF 450 KB), an annual publication relating to wholesale banks. However, the contents will be of interest to retail firms, too, as the report provides insights into good and poor practice on meeting regulatory expectations on key conduct and culture topics. The key findings were:

- Firms' identification and awareness of conduct risk remains weak. Firms may show understanding of topic areas such as conflicts of interest, suitability, fairness to customers, non-financial misconduct and technology. However, identification (or consideration) of the underlying, specific or granular conduct risks underpinning these topic headings is less well understood. This can mean that firms gain false reassurance that they have designed and implemented an appropriate conduct risk framework.

- Generally, a firm's purpose and values are not well understood by its employees (nor how their own roles and responsibilities contribute to that purpose). Participants made it clear that alignment of a personal sense of purpose and core values with those of the firm was very important, but rarely discussed. A clear articulation of a firm's purpose and its alignment to an individual's role is pivotal in ensuring a firm's strategy, proposition and associated control environment are appropriately and consistently aligned.

- The FCA found that “speaking up” varies significantly between firms and between different parts of the same firm. Escalation channels (including whistleblowing) are largely unused and reserved for the most serious cases. Psychological safety is a strong characteristic of a healthy culture. Firms need to strive to create an environment where employees feel safe to share ideas and speak up where they see issues. Ultimately, it results in more productive and innovative businesses. It also reduces the potential for inappropriate risk-taking or behaviour that can result in major incidents of misconduct, causing harm to consumers and markets.

- Some firms' approach to rewarding performance was still solely linked to output/delivery, regardless of their conduct. For other firms, the consideration of conduct in a “balanced” scorecard mechanism was still weighted too heavily toward commercial success and lacked appropriate consideration of key conduct-related metrics. The practice of rewarding performance (either through promotion or bonus) regardless of behaviour has a strong reverberating effect through a firm and can perpetuate an unhealthy culture.

- Linked to the above, leading firms are making good use of trend data on staff performance around behaviour. However, more needs to be done by peer firms to factor in these considerations to identify, and react to, shortfalls in behavioural expectations. Lack of awareness of key behavioural traits can manifest as a lack of commitment to values and adherence to process and can consequently lead to firms failing to meet regulatory expectations and deliver poor outcomes.

Wholesale banks will be expected to use the further detail and granular examples set out in the paper to benchmark their performance and make necessary improvements in advance of the next review. However, as noted above, this exercise would benefit all firms and could include considerations of the following key components:

- How effective is the firm's overarching framework (in design and operation) in identifying sufficiently granular conduct risk together with appropriate associated mitigation activity?

- How well-articulated are the firm's purpose and values? Is there clear line of sight from them through the firm's strategy, propositions and control environment to specific roles and responsibilities? Are they supported by the cultural indicators and behaviours displayed by employees within the firm?

- How well-drafted and utilised are the firm's escalation processes for non-financial misconduct? How aware are employees of the processes, and how does the firm encourage employees to speak up and provide the requisite psychological safety for them to do so?

- What behaviours, attributes and performance are rewarded within in the firm in terms of promotion and bonuses? Do they align with the purpose and values of the firm? Do they reflect the firm's documented remuneration and performance management policy and procedures?

- Is sufficient focus being given to support management to drive appropriate conduct, and behaviours on an ongoing, basis (rather than just point-in-time)?

The FCA's continued focus on the wholesale sector is borne out by figures from its Annual Report and Accounts annex relating to enforcement activity. Current enforcement activity, directly attributable to wholesale, account for more than 25% of the FCA's open investigations. The warning signs are there for wholesale firms.

High Court finds in favour of business interruption insurance policyholders

Following our previous updates, the High Court has now handed down a decision on the test case brought by the FCA to resolve the lack of clarity and certainty that existed for many policyholders making business interruption claims. The Court found in favour of policyholders on the majority of the key issues. The ruling presents another hurdle for insurers, as they will face a significant uptick in claims and complaint activity and will therefore need to increase resource on processes and operations. The priority now will be to respond to policyholders' claims in a fair and timely manner. There are also material, consequential prudential implications that firms will need to fully assess.

FCA proposed significant changes to how General Insurers price products

The FCA have published its final Market Study paper (PDF 542 KB) on GI Pricing Practices, together with a Consultation Paper (PDF 2.4 MB) on proposed remedies (PDF 542 KB). The FCA's proposals cut straight to the heart of the issue of fair pricing.

They have proposed the following remedies:

- For all retail motor and home products – the renewal price offered to a customer cannot exceed the equivalent new business price through the same channel. This will tie together new and renewal prices, reduce shopping around and thereby reduce the frictional costs.

- Enhanced product governance rules to ensure that pricing practices deliver good outcomes for all customers. This will apply to all GI products and will require firms to consider fair value in their product governance processes (across core products, add-ons and premium finance).

- Rules to stop auto-renewal being used as a barrier to switching.

- Enhanced supervision and monitoring by the FCA (including pricing governance, adherence to the new rules, ensuring firms are actively considering value.

The proposed remedies will have a significant impact on the market, affecting both consumer behaviour, distributors and insurers themselves. It is likely to lead to a significant change in pricing approach with the impact on individual insurers varying in a number of ways. Prices for new customers are likely to increase, although the FCA believe that these discounted prices were previously “unsustainable”.

Insurers will need to consider the impact on their strategy, customer proposition and business model which could lead to more product or proposition innovation as insurers seek to compete on more than just price.

Championing customer outcomes: from football to financial resilience

The FCA has published a Call for Input (PDF 818 KB) looking to reform the retail investment sector - both its product manufacture and distribution. The FCA has determined that the consumer investment market is not working as well as it should. It has highlighted that there have been too many scams and scandals; too often consumers are also being offered unsuitable products or advice. The Call for Input includes seeking views on how firms could offer a range of products that meet straightforward investment needs, how to ensure that those that do buy higher risk investments understand the risks, how to ensure that the public is better protected from scams and how to ensure that firms strive to offer better products and services. Aligned to this, the FCA has also issued a Dear CEO letter (PDF 132 KB) to flag a risk that there has been increased client money balances occurring since COVID-19, which can lead to poor customer outcomes.

In relation to General Insurance, the focus has been on brokersas well as insures. Like many other firms before them, GI brokers are the latest to receive a portfolio letter (PDF 122 KB) which, beyond the standard FCA fare relating to governance, culture and EU withdrawal, draws out financial resilience as a prominent area of focus.

The impact of COVID-19 had seen a general reduction in the use of cash. However, for retail banks, the FCA has confirmed its guidance formally requiring them to consider the impact of a planned closure of a branch or ATM on their customers. This risk of consumer harm is exacerbated by the high proportion of customers with vulnerable characteristics that tend to use these services. Hence, the regulatory intervention in seeking to ensure that customers are formally part of the decision-making process.

COVID-19 has also seen an increase in the number of pension scams. The FCA and TPR have joined forces to raise customer awareness with four simple steps for pension savers to remember. Over £30m has been reportedly lost to pension scammers since 2017. This time, regulators have tried to use football as the theme to cut through the lack of awareness and engagement on this key cause of consumer harm.

COVID related measures: arrivals and departures

The FCA has announced a series of measures designed to ensure that firms provide tailored support to customers who continue to face difficulties due to COVID-19. These extensions of further support include guidance for insurance and premium finance firms and mortgage lenders and proposed new guidance for consumer credit and overdraft firms.

Conversely, the PRA has published updates to end some COVID-19 contingencies - the temporary approach to VAR back-testing exceptions and specific payment deferrals under IFRS 9 and capital requirements.

Maintenance of the regulatory framework

Two key publications illustrate that the FCA is continuing to actively monitor its regulatory framework. The first, more progressed, paper is a consultation on extension of its annual Financial Crime reporting obligation to include activities which, in the FCA's view, pose a higher money laundering risk. The second, significantly earlier on in its infancy, accompanied the news that Chris Woolard is to leave the FCA. Before he departs, Woolard will head up a review focusing on how regulation can better support a healthy unsecured lending sector.

The Financial Services Regulatory Initiatives Forum has issued the second edition of its Regulatory Initiatives Grid. The Grid is designed to help firms manage the operational impact of implementing initiatives from a wide range of regulators (now expanded to include ICO and TPR). New upcoming work includes LIBOR transition and broader Government reviews, including the payments landscape review and the future regulatory framework review.

Activity relating to the UK's withdrawal from the EU continues and is, understandably, expected to ramp up as we head towards Christmas. This activity also features in the updated Regulatory Initiatives Grid. The PRA published a letter from Sam Woods highlighting the importance of firms being operationally prepared to enter the Temporary Permission Regime and being able to meet the regulatory requirements that will apply once in it. The FCA's latest Market Watch (PDF 101 KB) echoed these sentiments in relation to MiFID II transaction reporting.

Finally, it has been regulator reporting season with both the FCA and PSR publishing their annual report and accounts. Much of both are backward-looking or detail future regulatory priorities already well-communicated. However, as ever, they provide a useful summary of key activities and a source of rich MI on what they have been busying themselves with. Responses to COVD-19 feature heavily.

Stay up to date with what matters to you

Gain access to personalized content based on your interests by signing up today

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia