Agriculture

It was a slow year for dealmaking in the agriculture sector. Deal values shrank 30 percent year-over-year on the back of 8 percent lower deal volume (at around 455 deals). Many of the bigger deals were driven by vertical integration strategies and about a quarter took place in Asia. However, global market value for the agriculture sector is expected to grow at 5.66 percent (CAGR) until 2028, to reach US$4.86 trillion1 in value

One big challenge facing the sector is climate change. According to the OECD, the food system accounts for 12 percent of global greenhouse gas emissions. Yet the sector is one of the most ‘at risk’ due to climate change and natural disasters like flood, drought and hail. It is in everyone’s best interest to find ways to reduce agriculture’s footprint.

Governments will need to play a key role. Indeed, many are facing growing pressure to realign their policies in ways that drive greater international cooperation around the types of structural adjustments that will need to be taken in order to meet the world’s sustainability goals. Yet policy reform takes time. And investors are somewhat nervous about the direction it might take.

In 2024, expect to see significant activity around agriculture technology companies. Recent data suggests agricultural production needs to increase by 68 percent by 2050 in order to meet the needs of the growing population2. New farming technologies will be key. M&A is expected to focus on technologies that enable farmers to derisk their farming system, especially where traditional agri-tech companies look to buy agricultural businesses because of the innovation present within their farming systems.

In 2023, most deals in Asia involved farm management or farm technology start-ups – companies using technologies like blockchain, AI and computer vision to improve crop yields, enhance supply chains and drive sustainability. Perhaps not surprisingly, private equity played a key role in many of those transactions

Food and Beverage

The deals should keep flowing into 2024

2023 brought increased deal volume to the sector with non-alcoholic deal volume increasing 3.5 percent and alcoholic beverage volume increasing 2 percent. More than US$13.3 billion changed hands with the largest deal of the year (Swire Pacific selling it’s Coca-Cola USA unit) valued at US$3.9 billion3.

The sector will continue to work through some risks in 2024, however. Sustainability will be key – not only due to shifting customer preferences but also to better manage volatile natural resource costs. The sector is highly reliant on water, energy and oil prices, which creates a number of environmental vulnerabilities. Competition is also expected to remain high with smaller players innovating on their channel offerings and larger players mastering the art of differentiation.

Looking ahead, three interesting sub-sectors seem set for growth – and potential M&A activity.

- Spirits and wine: Spirits are expected to grow at 5.6 percent4 to US$191 billion between 2023 and 2028, and wine is anticipated to grow at 4.3 percent to US$457 billion5. As investors consolidate into the markets, this sector may become a deal party favorite.

- Nutritious beverages: Analysts expect this sector to enjoy growth rates of 6.5 percent over the next five years (to reach a US$203 billion market size) led by a shift towards healthier lifestyles, reduced sugar consumption and consumer desire for convenience.

- Ready-to-drink (RTD) beverages: Globally, the RTD beverage segment is expected to grow by 7 percent, into a US$327 billion market, by 2028. Many prominent beverage players are making strategic acquisitions to expand their portfolio and capitalize on growing demand6.

- No/low-alcohol beverages: Consumer health consciousness is also behind the expected rise in demand for these beverages, with growth of 13 percent expected. By 2030, the market is expected to top US$70 billion7.

Looking forward to a healthier year

Demand for food is increasing with the food segment expected to see 8.5 percent growth over the next five years from a base of US$ 42.1 trillion in 2023. Yet that has not translated into massive deals. In fact, the sector saw a 59 percent decline in deal volume year-over-year with only around 1,000 deals conducted in 2023.

A few pockets of activity have emerged however. About 40 deals in 2023 (worth a total of around US$14 billion) were for ingredient assets as companies looked to drive vertical integration. The frozen food market also saw some activity (such as the Nestlé/PAI Partners Joint Venture for frozen pizza in Europe).

However, after more than a year of constant price increases, we are seeing the food price index start to fall, with consumer manufacturing and retailers alike managing price dynamics on a full-time basis. While this reduces the level of volatility in margins that has made deal making more difficult, we continue to see headwinds in tightening in consumer disposable income. Labor shortages are also creating challenges for food manufacturers, who are now increasingly turning to automation to help ensure continuous and efficient production.

Two big trends in the C&R industry may increasingly influence M&A activity going forward. The first is a focus on health which has seen brands start to enhance the nutrition of packaged and frozen food products. The vegan category was particularly hot with around 60 deals inked in 2023. Sustainability will also likely remain a hot topic as the pressure to decarbonize picks up.

Food retail

The dealmakers left the dinner table in 2023. M&A activity in the food retail sector was down 15 percent year-over-year. Value was down by a whopping 4 percent to just US$ 22 billion. However, it should be noted that 2022 was already a correction year for deals after record breaking deal activity in 2021; current deal volume and value are now close to where they were in 20208.

Interestingly, private equity saw a significant uptick in activity in the sector, with deal volume rising 27 percent versus 2022, primarily focused on casual dining. In fact, casual dining was the most active sub-sector for dealmakers with more than 400 deals conducted in the year – driven largely by low valuations.

With inflation remaining relatively high and disposable income at recent lows, many investors are carefully watching how consumers sentiment impacts the sector. Restaurants in key markets such as the UK, US and Canada saw retail activity cut in half as purchasing power decreased and consumers shifted away from restaurants. A multitude of options in food retail is also spreading consumer spend more thinly.

As such, KPMG professionals expect to see continued deal activity as larger players look to consolidate their footprints and grow into new markets. Carrefour’s acquisition of Cora and Match assets from Louis Delhaize, for example, gives Carrefour a stronger presence in Eastern and Northern France. On the other end of spectrum, Casino, another France-based food retailer, has been undergoing restructuring and is expected to sell some of its hypermarkets and supermarkets.

We may also see continued activity on the technology side – particularly in Asia. Walmart, for example, has made 10 deals over the past three years in India alone, mostly to capture technological capabilities. Also, Nestlé ventured into food delivery again through its acquisition of Wonder Group for US$100 million, suggesting increased confidence in the sector.

Home and personal care

Valuations are up but volumes remain steady. Largely driven by demand for personal care assets, the home and personal care deal market remained fairly resilient in 2023. Analysts expect strong growth in many segments over the next few years; the sexual wellness market is forecast to grow by almost 10 percent per year to 20289, cosmetics are expected to grow by 5.7 percent annually, home care by 4.7 percent and personal care by 3.3 percent.

Average global deal multiples in the beauty and wellness segment hit 16x earnings over 2022-23, outperforming the S&P 500 average of 14x. And these types of valuations are expected to remain into 2024, even as deal volume shrinks somewhat due to continued economic uncertainty.

The sector is set to experience growth across various segments, influenced by technological advancements and strategic realignments. While the growth prospects are impressive, home and personal care companies will need to deal with a number of urgent risks going forward. Labor costs are rising, eroding profitability and reducing business agility. Supply chain disruptions – while largely improved – continue to influence prices and availability. Intense competition in the sector is making it difficult for new entrants to get a foothold.

However, there are a number of hot spots that could drive continued dealmaking activity into 2024. As large FMCG conglomerates continue to refine their portfolios, we will likely see the disposal of some attractive businesses. Unilever, for example, is considering selling Elida Beauty to a PE in its pursuit to dispose non-core personal care and beauty brands.10

With consumers looking for personalization and convenience, deals that improve players’ omnichannel capabilities and experience are expected. AI is predicted to be behind 95 percent of customer interactions in the next two years which should drive interest in assets that deliver or enable emerging technologies.

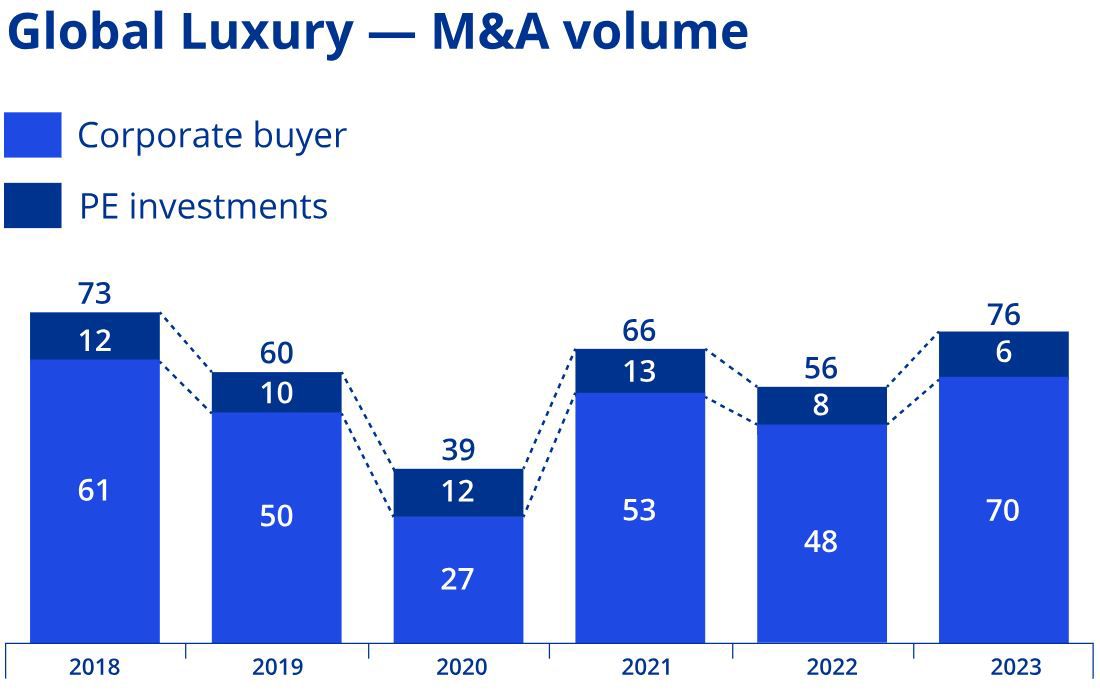

Luxury goods

Consumers in China and America kept the luxury market growing through 2023. Indeed, despite a fallback in demand due to weaker discretionary spending and massive macroeconomic uncertainty triggered by socioeconomic and geopolitical disruption, analysts expect the market to grow by 3.4 percent per year to reach US$355 billion in size by 2028.

M&A activity has been frothy. Deal volume in 2023 rose by around 30 percent with 80 deals announced in 2023. A number of deals – such as Tapestry’s acquisition of Capri Holdings (parent of Versace and Michael Kors) – were designed to consolidate top brands to drive scale and enhance competitive power.

However, a decline in earnings in the third quarter (Kering, owner of Gucci, Balenciaga and other luxury brands, reported a 9 percent drop in sales in the quarter) might suggest a slowdown in industry growth. With China accounting for around 22 percent of industry sales, all eyes will be on that market’s economy in 2024.11.

In this environment, many luxury brands are looking for opportunities to enhance profitability. Some are considering how they might optimize their order and delivery processes to improve the customer experience and reduce costs. Reducing losses, for example by better managing counterfeit returns, will be key. Most are also looking at their supply chain to see how they can better respond to ESG, regulatory and technology pressures.

On the growth side, luxury brands are seeking to innovate and grow in their markets by exploring new revenue models and channels. At the same time, partnerships and consolidation in many markets are expected as players search for even small-size luxury brands with distinct propositions (LVMH has made 13 such acquisitions in Mainland Europe and US to reach a diverse range of customers). The secondhand market is expected to grow considerable, accounting for up to 20 percent of revenues by 2030. Expect to see more deals as leaders emerge in these growing segments.

Non-food retail

While global non-food retail markets enjoyed considerable growth over the past few years, deal activity in the sector is now slowing as economic uncertainty prevails. Deal volume contracted by around 10 percent in 2023 (to around 440 deals). Apparel and accessory retailers saw the most activity (with 154 deals) yet here, too, volume was down about 10 percent versus 2022.

Economic uncertainty is being compounded by a number of risks and challenges in the sector. Regulatory complexities are making some investors nervous as retailers are asked to digest a range of new regulatory requirements on product safety, labeling, packaging and import/export restrictions. ESG considerations (as set by both regulators and society) are raising a number of red flags for investors, particularly around the apparel segment. Non-compliance can be costly, time-consuming and detrimental to brands.

At the same time, intense competition is creating pricing pressures as incumbents and new entrants fight for market share, pushing down prices and thinning profit margins. That is making potential investors take pause.

There is also growing pressure to reduce waste – both due to sustainability concerns and efficiency requirements. Our conversations suggest that strategic investors are looking at metrics like unsold inventory (which currently accounts for US$4.3 billion or about 3 percent of global turnover) when valuing target acquisitions12.

Online retail

With inflation rising and consumer discretionary spending constricted, investors kept on the sidelines in the online retail space. Global deal volume fell by around 50 percent in 2023. Private equity participation fell by 60 percent. Valuations plummeted. And a number of failures were announced, particularly in the D2C space (such as SmileDirectClub , which was once valued at more than US$8.9 billion)13.

That being said, it is clear that online retail remains a growth sector. The global market is expected to grow to US$7 trillion in the next two years, driven by the increasing popularity of mobile shopping and subscription services. It is expected that AI and emerging retail technologies will help boost the market further as digital and physical become more integrated and personalized.

The economic trends will remain challenging this year. However, some online retailers are expected to invest in new technologies in order to make the business more profitable overall. Some are exploring how automated micro-fulfillment centers could help them more efficiently close the final mile. We are also seeing online retailers use machine learning, AI and risk-scoring analysis to spot fraud (global fraud losses reached US$48 billion in 202314).

Over the coming year, KPMG professionals expect to see three trends start to influence dealmaking in the sector.

- Bifurcation of D2Cs: Success in the D2C space requires good unit economics, strong differentiation, low customer acquisition costs and access to great talent. Those that demonstrate all of these are likely to see valuations rise. Those that do not risk failure.

- Building omnichannel: With average conversion rates of under 3 percent, digital retailers are expanding into new channels in order to increase their customer touchpoints and drive sales. Increasing deal activity is expected around assets that deliver offline presence in particular.

- Sustainable packaging partners: With consumers increasingly willing to pay a premium for sustainable products with less packaging, some dealmaking activity is expected as industry players look for packaging partners that deliver sustainability and differentiation.

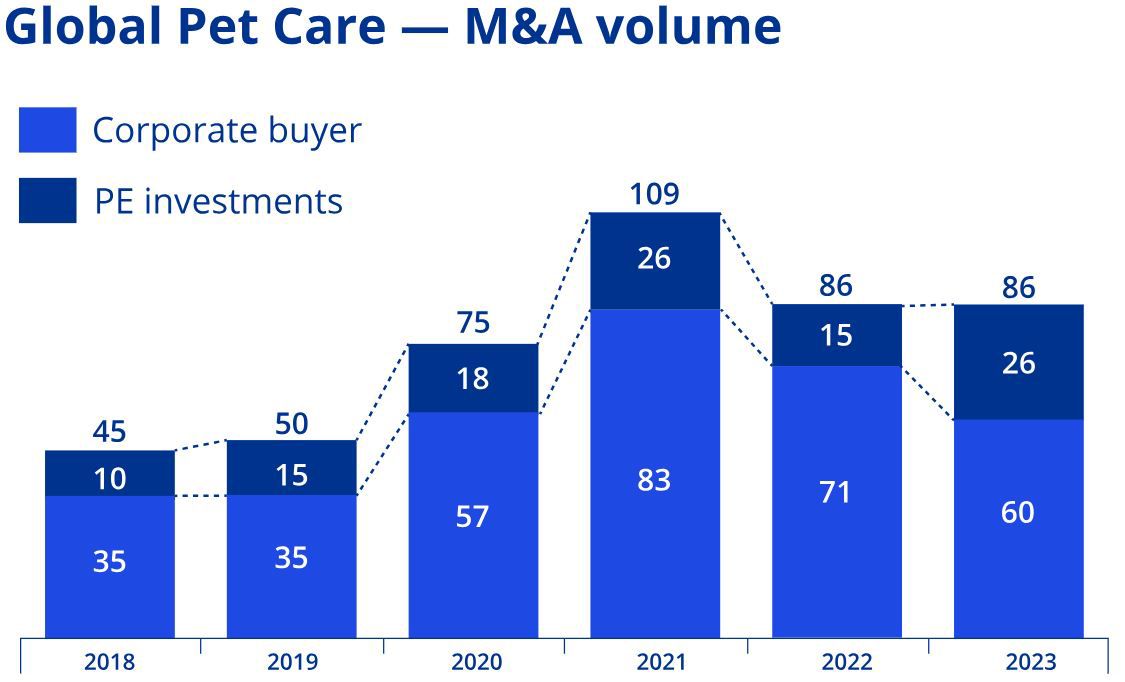

Pet care

Price inflation has taken a bite out of pet sector margins. High raw material costs have driven input costs up by 18 percent and brands are reaching the end of their customers’ tolerance for price increases. Between 2022 and 2023, unit prices across the pet care department rose 17.6 percent – pet food increased by 21.8 percent, pet supplies by 9.8 percent and pet treatments by 3.9 percent. As a result, sales in pet food grew 17 percent (by revenue).

Yet margins are tightening. Indeed, KPMG research shows that public company players saw their EBITDA dip slightly (0.17 percentage points) in 2023 as topline growth slowed.

Even so, M&A volumes remained steady in 2023 with more than 80 deals announced. Private equity made up a quarter of all deals and nearly half of all deals were conducted in the US or UK.

Interestingly, venture capital seemed particularly active in developing markets. Some investors with higher risk appetite have been looking at ‘second tier’ pet markets. The largest markets are the US (with 155 million dogs and cats) and China (with 141 million). Now investors are looking at next tier of markets like Brazil (with 78 million pets), Mexico (46 million) and India (20 million)15.

Two other trends seem set to influence activity in this sector. The first is the shift towards end-to-end care. Mars Inc, for example, one of the world’s largest pet food producers, acquired five veterinary services assets in 2023. The second is a trend towards premiumization and fresh food which is expected to grow to a US$6 billion market in the US by 2030.

Explore

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia

1 Agriculture - Worldwide | Statista Market Forecast

2 AT2050_revision_summary.pdf (fao.org)

3 Hong Kong's Swire Pacific sells U.S. drinks unit to shareholder for $3.9 billion | Reuters

5 Wine Market Size, Industry Share, Global Analysis, Future Demand, 2030 (fortunebusinessinsights.com)

6 Ready-to-Drink Beverages Market Size | Growth Forecast [2030] (fortunebusinessinsights.com)

7 A public health perspective on zero- and low-alcohol beverages (who.int)

9 Sexual Wellness Market Size, Share, Growth | 2024 to 2029 (marketdataforecast.com)

10 Unilever to sell Elida Beauty to Yellow Wood Partners | Unilever