Reporting Update 23RU-13

Australian Sustainability Standards taking shape

The Australian Accounting Standards Board (AASB) has released Exposure Draft ED SR1 Australian Sustainability Reporting Standards – Disclosure of Climate-related Financial Information.

ED SR1 includes three proposed Australian Sustainability Reporting Standards (ASRS Standards) that include modifications to the baseline of IFRS® Sustainability Disclosure Standards1 :

- [draft] ASRS 1 General Requirements for Disclosure of Climate-related Financial Information – based on IFRS S1 but limited to climate-related financial disclosure

- [draft] ASRS 2 Climate-related Financial Disclosures – based on IFRS S2 with Australian-specific requirements

- [draft] ASRS 101 References in Australian Sustainability Reporting Standards, a draft service Standard to list the relevant versions of any non-legislative documents published in Australia and foreign documents that are referenced in ASRS Standards.

The draft ASRS 1 and draft ASRS 2 are aligned internationally to IFRS S1 and IFRS S2 and build on the global baseline for investor-focused sustainability reporting in Australia – with a climate-first approach.

The main differences to the ISSB™ Standards are small and specific and have been made to fit the Australian context and Australian Regulations.

The ASRS Standards are proposed to be applicable for both profit and not-for-profit entities.

Treasury is yet to release its position paper following its second consultation in June 2023, to provide clarity on which entities will be in scope of the ASRS Standards and when. The AASB is proposing the standards would apply to annual reporting periods beginning on or after 1 July 2024. However, the financial period in which an entity is first required to apply these ASRS Standards would be subject to decisions of the Australian Government.

The AASB draft standards are fit for purpose for the Australian context – aligned wherever possible with the international standards for consistency, but with a number of sensible variations to fit the Australian regulatory context.

Download the Reporting Update

Further details of the [draft] ASRS Standards and comparison to the ISSB Standards are set out in this Reporting Update.

ED SR1 has a 120-day comment period with submissions due by 1 March 2024.

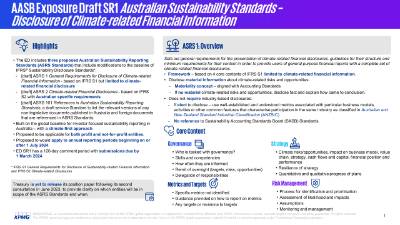

Executive summary for Directors

For a high level overview of the key content included in the ASRS Standards, we have prepared an executive summary. This summary may be useful for Directors or other individuals who require only a broad understanding of the requirements for the Exposure Draft.

- IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-related Disclosures