At a time of seismic geopolitical shifts, advancing technology, ongoing globalization, and new business demands, tax functions are being called on to strengthen their performance and contribute more value. Now more than ever, tax leaders should ensure their tax departments are built for the future — by evolving the function and by restructuring operations so they can better support their organizations and help deliver lasting results.

In a reimagined tax function, the strategy for tax aligns with and helps further the business’s broader goals. To support this, the tax operating model is configured to standardize, streamline and automate routine work; and the right mix of sourcing options (e.g. co-sourcing, managed services) is in place to help ensure compliance is well managed while allowing tax teams to refocus their efforts on more strategic areas.

Together with strategy, operations and sourcing, a focus on performance is critical for a reimagined tax function’s success. As global companies rethink their approach to tax, their tax functions should constantly monitor and manage how well they are doing in their efforts to support the business and add as much value as possible.

Based on the experience of KPMG tax transformation professionals, we believe that driving peak performance requires putting priority on four key areas:

- Managing talent

- Managing stakeholders

- Adopting a value-based approach to performance

- Setting key performance indicators (KPIs) to measure success

In this article, we examine each of these priorities in turn, highlighting ways you can help boost your tax function’s performance and demonstrate the overall value your tax team is adding to your organization.

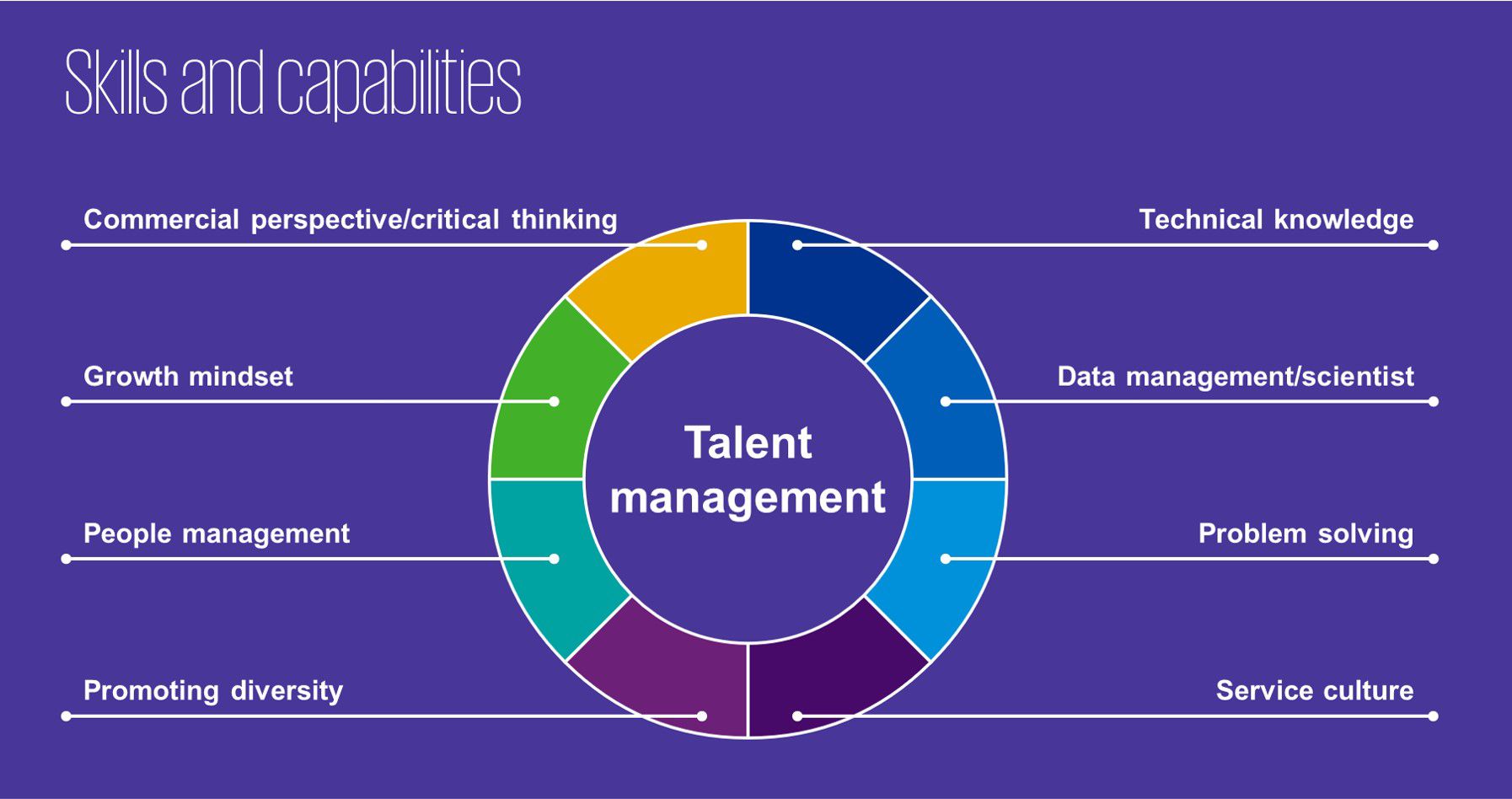

Managing talent

With the currently tight global market for skilled professionals and increasing mobility opportunities arising from the trend toward remote working, attracting talent and continuously motivating them to perform better has never been more important.

To help achieve the best results, you need a strategy in place specific for your company. Even if you have a formal HR team supporting you, the tax function should take a hands-on approach to its strategy for managing talent.

- Shower them with recognition: In addition to opening opportunities for employees, you can further motivate them by giving them high, broadly communicated praise when they succeed. Tax functions should seek to instill a culture that prizes communication and service excellence. Success should be recognized openly and frequently, and this recognition should go beyond the results to tell the larger story about how those outcomes were achieved.

- Treat your employees as individuals – Top-end talent do not want to be seen as a member of a larger class. Your tax talent strategy should deliver an experience that assures each employee they are being perceived and treated as unique.

- Provide new opportunities – Today’s younger professionals want to grow, learn and feel like they’re gaining new skills and moving forward. Satisfying these ambitions means having clear career development paths based on the tax function’s sourcing strategy, as well as making training and mentorship programs available to keep your talent’s continuous improvement on track.

In terms of skills and accountabilities, everyone is an accountant in the digital age. Tax functions are looking for so-called “convergence skills” — varied skills with intersecting trajectories that combine to enable a high-performing, future-ready tax team. These skills include not only core tax technical skills, but also capabilities in business acumen, critical thinking, tax technology, data and analytics. Expertise in people management is also key, among other things, to help craft individualized career plans to develop the mix of skills that meets your tax function’s current and future needs.

As competition for talent escalates, the most successful organizations will likely be those that recognize and accommodate the aspirations of younger generations to work in an environment that suits their values and expectations. Bear in mind also that talent tends to move in packs, so if you succeed in creating an environment that draws some younger talent, you’ll likely find it increasingly easy to attract more talent from within that demographic.

Finally, the tax function’s talent strategy should seek to promote as much diversity as possible — not just of identity, but also of background, skills and mindset. Embracing a wide variety of distinct working styles, ideas and perspectives can help create an innovative, productive environment that’s better positioned to create value.

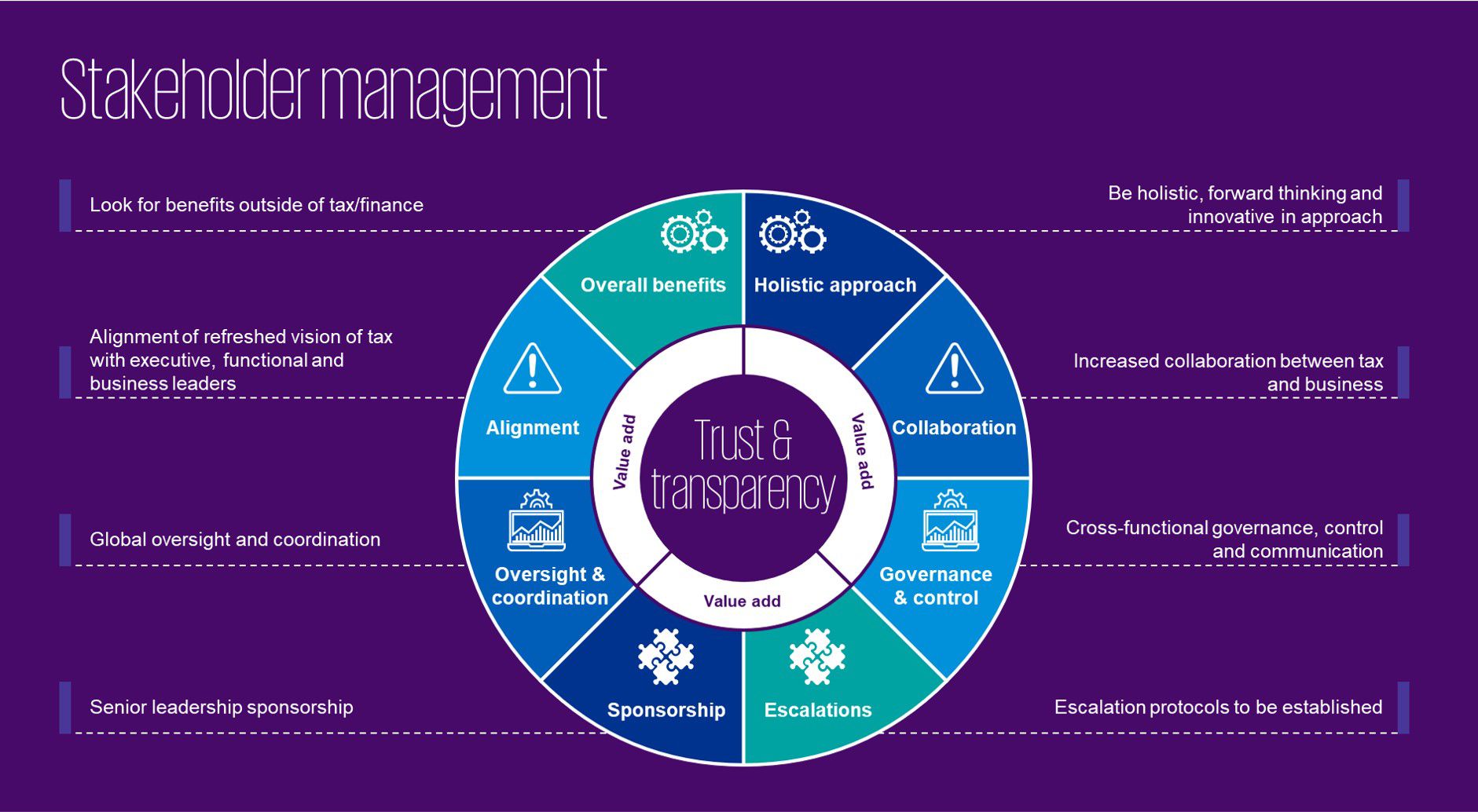

Managing stakeholders

The past decade has seen increasing interest in the inner workings of tax functions, as governments and societies demand more tax responsibility on the part of global companies and as senior management and other internal players seek assurance that reputational risk related to tax is being well managed.

As a result, tax leaders need to inspire confidence through stakeholder relations that highlight trust and transparency in the function’s strategy and processes. Tax leaders can do this by understanding the composition and objectives of their various stakeholder groups and then developing effective strategies for engaging with them.

Forward thinking is a must in this regard. Tax leaders need to be adept at understanding what changes are needed and explaining what benefits a change would deliver — with special attention to benefits to the organization beyond the tax function. These communications are critical for building a business case for transformative change in the tax function and gaining support from internal sponsors.

A leading practice is for tax leaders to regularly deliver a summary of current tax trends that highlights any tax function changes or opportunities they may bring. This summary should explain the reasons behind any gaps, the challenges expected on implementation, and how they would be addressed. The summary should also include a set of KPIs for measuring progress.

Tax leaders would also do well to communicate their work to improve tax governance and controls, supported by technology. This reporting helps stakeholders know that everything has been filed on time and work is on track. It also shows that the tax function has the systems and the controls needed to sustain good compliance going forward. These communications can also serve to give the business visibility over tax attributes, management of tax audits and cash management.

Finally, given the high volumes of email most professionals receive daily, having a proper escalation and communication protocol is key for enhancing communication with stakeholders.

Structuring these communications so they meet everyone’s needs is key. Stakeholders rely on the tax function to inspire confidence and gain support from customers and regulators. The tax function relies on stakeholders for the sponsorship they need to help its transformation. i Your communication strategy should ensure that the right communication protocols are in place for stakeholders and the tax function alike.

Adopting a value-based approach to performance

A third priority for improving tax function performance involves measuring and communicating the value the function brings to the business. This value extends beyond effective, everyday tax compliance and reporting to focus on those more strategic activities that bolster the tax function’s reputation as a business partner. We believe the more value the function can show it produces, the more the business will look to involve tax in planning and decision making.

Tax functions can add significant value in four key ways:

- Cost containment: Like other functions, today’s tax functions are under intense pressure to reduce costs. Tax leaders should focus on how their teams do their work, and how they can enhance efficiencies and manage costs within their teams to help ensure they drive as much value for the business as possible.

- Proactivity and opportunity: By taking a proactive approach to new tax laws and business initiatives, tax leaders can find opportunities to manage tax more efficiently and help reduce the amount of tax the business pays. This involves maximizing the use of tax deductions and incentives in all locations, as well as effective tax rate management to help ensure the business is paying — but not overpaying — the right amount of tax in any one jurisdiction.

- Time efficiency: Once a tax function starts to analyze all the different aspects of its operation, they can identify new ways to improve their processes. For example, significant time gains can be achieved by improving uniformity across jurisdictions, since it is quicker for people to understand and review information when it is presented in consistent formats. Efficiencies like these can free up considerable time for tax and finance team members, which they can then devote to higher-value work. Tax teams can also find ways to speed up the time spent on tax work within other parts of the business, who will welcome the lighter burden.

- Technology: With the right investments in technology, tax teams can free up the significant amount of time they spend retrieving data housed in multiple systems across the company, verifying it and reformatting it for compliance. Many international companies we work with are investing in systems designed in cooperation with finance, IT and other functions to satisfy a variety of data needs, including those of the tax function. By building standardized, automated tax data processes and controls into company-wide, end-to-end data management frameworks, tax teams can get the right tax data in the right format when they need it. Again, the substantial time saved can then be spent on more profitable work.

Setting KPIs to help measure success

KPIs are critically important to help improve value-driven performance and the behavior of teams. Measurement drives performance, and clear, commonly understood performance measures can help the tax function demonstrate its worth and quantify the value it brings.

In particular, KPIs can be set to gauge performance in the three key areas of reducing costs, contributing value and improving quality.

Where cost reduction is concerned, KPIs can be set to create goals that promote success in reducing the direct costs of regulatory compliance (e.g. labor, service providers, training). They can also encourage the tax team to contribute more savings with targets for decreasing costs for data management and retention, easing time spent by other departments on tax work and cutting manual compliance efforts by leveraging technology and automation.

KPIs concerning value creation can compel greater focus on the tax function’s contribution to improving cash flow, meeting corporate strategic objectives and enhancing the use of resources. For example, these KPIs could measure taxes saved through planning ideas, reduction in effective tax rate and reduction in cash taxes paid. Other KPIs could be introduced for the tax function’s contributions to broader objectives, such as improving quality of life and job satisfaction (as shown by measuring reduced turnover) or better sourcing of data management (as shown by reduction in data collection times).

A third set of KPIs can aim for improvements in the quality of the tax function’s contribution through upgraded controls, enhanced tax governance and visibility, and higher-quality deliverables — all of which can lead to both better compliance and better insights for planning. KPIs here can target quality improvements in terms of changes in audit assessments, the number of tax years open and the extent of financial statement adjustment needed to prepare the tax provision.

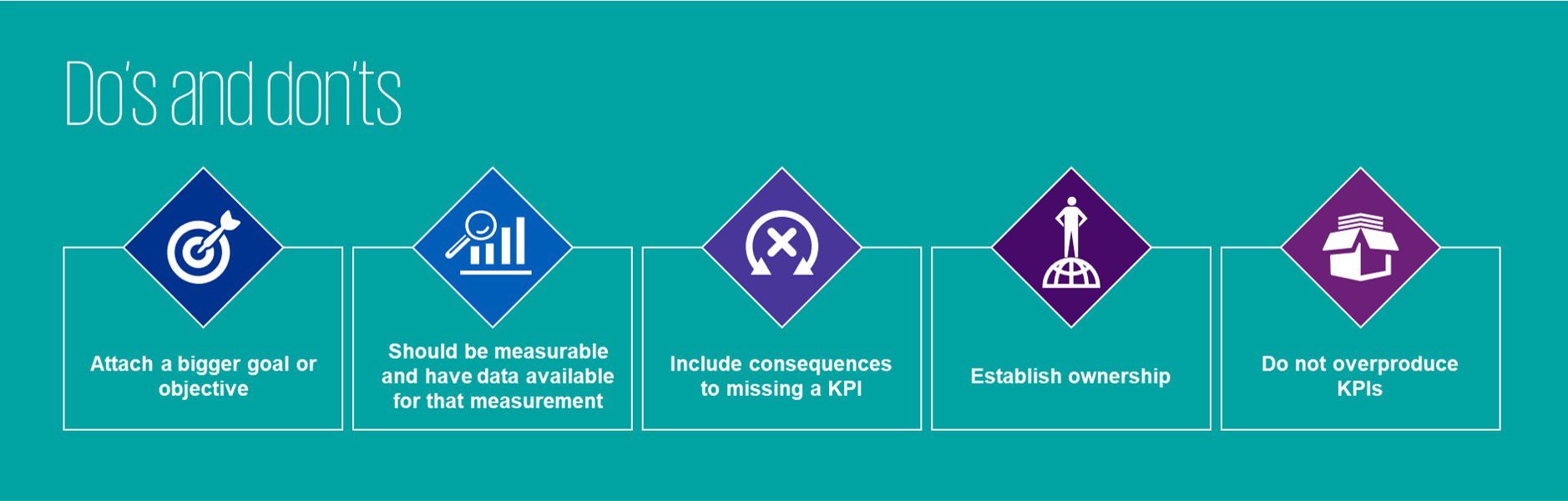

Some dos and don’ts to keep in mind when setting KPIs for the tax function are as follows:

Attach a bigger goal or objective. Doing this can help draw the line between the company’s broader strategy goals and the tax function’s work to support them. For example, if the organization’s objective is to prioritize cash tax management, KPIs can be as follows:

- Forecasts produced by X date each month for Tier 1 entities

- Accuracy to be within X percent tolerance

- Forecasts produced by X date for Tier 2 entities

Ensure the KPI is measurable, and data is available for that measurement. It’s important to avoid setting goals that have no objective data points for measuring their achievement. For example, “effective communications to the Board and wider stakeholders” is not a measurable KPI in itself. KPIs that could make this measurable could include:

- Producing quarterly Finance Committee reports

- Presenting tax reports at X number of Finance Committee meetings

- Seeking feedback from the Finance Leadership Team

Include consequences for missing a KPI: In order for KPIs to help drive real changes in behavior, appropriate consequences should be established for missing a KPI. It’s important to specify the impact of a missed KPI so that individuals and teams are compelled to support it. What reactive items will they need to adopt to meet the KPI in the future? Each KPI should come with a defined action plan to address any missed KPIs and help remediate the impact.

Establish ownership. In most cases, the tax function should specify which role within the organization owns each KPI and the related actions. Many tax KPIs are not owned by the tax function but by finance, so clarifying roles and responsibilities is important.

Do not overproduce KPIs: It’s better to start with fewer KPIs and refine them, with an eye to gradually introducing additional ones. An organization’s set of KPIs tends to have a maturity curve that builds over time from basic controls to more sophisticated measures of quality. For example, a basic KPI could be to “file timely compliance”. The next year, this could be supplemented with a new KPI based on the number of iterations per return. Finally, a mature, quality-based KPI could be to increase the number of tax adjustments that don’t require reworking.

We believe the success of future tax functions will increasingly depend on the strength of their strategies for enhancing performance — among individual members, the tax team, and the systems and processes enabling tax compliance work across the organization. By emphasizing performance and putting priority on measurement and improvement, organizations can help ensure their tax compliance is well in hand and that their tax talent are primed to deliver enduring value.

Throughout this article, “we”, “KPMG”, “us” and “our” refers to the global organization or to one or more of the member firms of KPMG International Limited (“KPMG International”), each of which is a separate legal entity.