Australia – If Planning to Travel for Work, Consider Tax Implications

AU – Travel for Work Can Have Tax Implications

This GMS Flash Alert provides an overview of three separate documents released by the Australia Taxation Office in relation to employee travel. One draft ruling was simultaneously withdrawn. The current draft guidance suggests that for some globally-mobile employees, depending on the duration of their assignments, some of the benefits they are provided (e.g., accommodation) may be subject to Fringe Benefits Tax.

While personal travel might not be on the cards for all yet, some recent releases from the Australian Taxation Office (ATO) mean that tax costs in Australia need to be front of mind when movement resumes.1

The ATO recently released three separate documents in relation to employee travel and, simultaneously, withdrew one draft ruling.

These latest releases are a continuation of a process that started in 2017 with the ATO seeking to clarify its position in relation to the tax treatment of employer-provided transport, accommodation, and meals.

WHY THIS MATTERS

An employee’s categorisation as travelling for work, living away from home, or indefinitely relocating, will determine the Australian tax treatment of transport, accommodation, and meal benefits (including allowances).

It is important for employers of internationally-mobile employees travelling into or out of Australia to have a clear view on this categorisation and the resultant impacts to avoid any unnecessary or unexpected tax costs. This is particularly relevant for Fringe Benefits Tax (FBT) in Australia, where the liability rests with the employer and is currently 47 percent on the grossed-up value of the benefit (for example, if accommodation were subject to full FBT, then for every $100 spent on accommodation there would be roughly a corresponding $100 of FBT payable).

From a global-mobility perspective, the ATO had previously provided some guidance whereby international employees on short-term assignments to Australia for up to three months were travelling for work and, as such, not subject to FBT.2 The current draft guidance suggests that for what are similar circumstances but a longer assignment period (expressed as 90 to 120 days), some of the benefits provided (e.g., accommodation) may be subject to FBT.

ATO Documents

Recent Releases

- Final Taxation Ruling, TR 2021/1 Income tax: when are deductions allowed for employees’ transport expenses?

- Draft Taxation Ruling, TR 2021/D1 Income tax and fringe benefits tax: employees:

- accommodation and food and drink expenses;

- travel allowances; and

- living-away-from-home allowances.

- Draft Practical Compliance Guideline, PCG 2021/D1: Determining if allowances or benefits provided to an employee relate to travelling on work or living at a location – ATO compliance approach.

Draft Ruling Withdrawn

- TR 2017/D6 Income tax and fringe benefits tax: when are deductions allowed for employees’ travel expenses?

Is There a “Bright Line” Test to Establish Travelling for Work or Living Away from Home?

Given the significant impact the categorisation of an employee’s circumstances can have on the employer’s tax position, whether there exists a “bright line” test that can be used to establish if an employee is travelling for work or living away from home is a valid question and one that is asked often in practice.

The ATO’s prevailing view is that every scenario must be considered on its own merits considering the relevant “facts and circumstances.” However, the ATO has also released some Practical Compliance Guidance (PCG) (currently in draft) specifically providing a “safe harbor” test.3

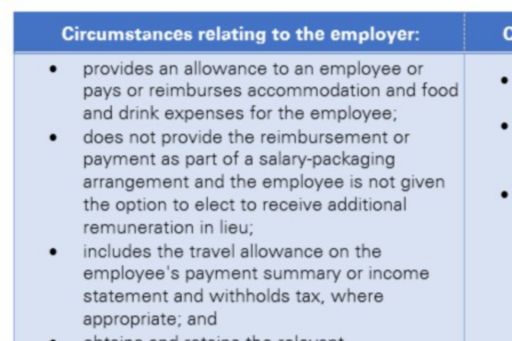

PCG 2021/D1 highlights the ATO’s compliance approach when determining if allowances or benefits provided to an employee relate to travelling for work or living at a location. The PCG incorporates a “day count” test, allowing employers a numerical basis for categorisation. It is important to note, this also increases the possibility of automation of this aspect of the FBT process (among other things).

The compliance approach sets a “safe harbour” of an aggregate period of fewer than 90 days in an FBT year for presence at a temporary work location to be treated as travelling for work. Provided that this requirement is met, PCG 2021/D1 allows an employee to have numerous short stints of travel of up to, and including, 21 continuous days.

The following table summarises the requirements for the PCG to apply:

KPMG NOTE

The PCG as a Guideline

It should be noted that the PCG only provides a guideline as to what will be accepted by the ATO as reasonable. If a scenario does not meet the criteria, the PCG does not render the relevant expenses automatically taxable, rather, it will require the employer to collate more evidence to support a “travelling for work” position. In an audit situation, the ATO will want to see evidence of how the employer has come to this conclusion, despite the PCG, and why.

Concluding Thoughts

The introduction of the PCG and the safe harbour it offers will provide a set of rules that can be applied to data and help an organisation assess retrospectively which trips might not require further consideration to classify.

Similarly, the PCG provides an opportunity for employers to plan employee travel within these limits if it wishes to do so and other practical business realities allow it to do so.

Organisations may need support in navigating the relevant legislation, cases, and ATO guidance in considering all relevant facts and circumstances and helping employers classify their travelling employees correctly.

FOOTNOTES

1 For related coverage, see GMS Flash Alert 2020-487, 9 December 2020.

2 For prior coverage, see GMS Flash Alert 2020-113, 25 March 2020.

3 Draft Practical Compliance Guideline, PCG 2021/D1.

PEOPLE SERVICES IN AUSTRALIA

Dan Hodgson

Perth, Western Australia

Partner – People Services

Tel. +61 8 9278 2053

Direct Tel. +61 8 9278 2053

Mobile: +61 416 017 131

Mardi Heinrich

Melbourne, Victoria

Partner – Deals, Tax & Legal People Services

Tel. +61 3 9838 4348

Direct Tel. +61 3 9838 4348

Mobile: +61 410 602 993

Ablean Saoud

Sydney, New South Wales

Partner – Deals, Tax & Legal People Services

Tel. +61 2 9335 8550

Direct Tel. +61 2 9335 8550

Mobile: +61 421 052 596

Hayley Lock

Brisbane, Queensland

Partner – People Services

Tel. +61 7 3434 9176

Direct Tel. +61 7 3434 9176

Mobile: +61 477 764 638

Jackie Shelton

Sydney, New South Wales

Partner – Deals, Tax & Legal

Tel. +61 2 9335 8511

Direct Tel. +61 2 9335 8511

Mobile: +61 477 764 638

The information contained in this newsletter was submitted by the KPMG International member firm in Australia.

VIEW ALL

SUBSCRIBE

To subscribe to GMS Flash Alert, fill out the subscription form.

KPMG Australia acknowledges the Traditional Custodians of the land on which we operate, live and gather as employees, and recognise their continuing connection to land, water and community. We pay respect to Elders past, present and emerging.

©2024 KPMG, an Australian partnership and a member firm of the KPMG global organisation of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved. The KPMG name and logo are trademarks used under license by the independent member firms of the KPMG global organisation.

Liability limited by a scheme approved under Professional Standards Legislation.

For more detail about the structure of the KPMG global organisation please visit https://kpmg.com/governance.

GMS Flash Alert is a Global Mobility Services publication of the KPMG LLP Washington National Tax practice. The KPMG name and logo are trademarks used under license by the independent member firms of the KPMG global organization. KPMG International Limited is a private English company limited by guarantee and does not provide services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.