Limited progress on cost take out measures has caused European banks to lose ground to their North American and Asian peers of late.

The market cap of the top five European banks is only ~ €274bn versus ~€815bn for North American and ~ €802bn for ASPAC banks. In terms of profitability, European banks also lag and are expected to generate an average ROTE of 6.7 percent, compared to 12.2 percent North American and 9.9 percent for ASPAC banks for 2021E. Consequently, we continue to see low market valuations for many European lenders with many being substantially impacted by the pandemic. The biggest impact, however, has come from a spike in loan loss provisions and an ensuing reduction in post-tax profits.

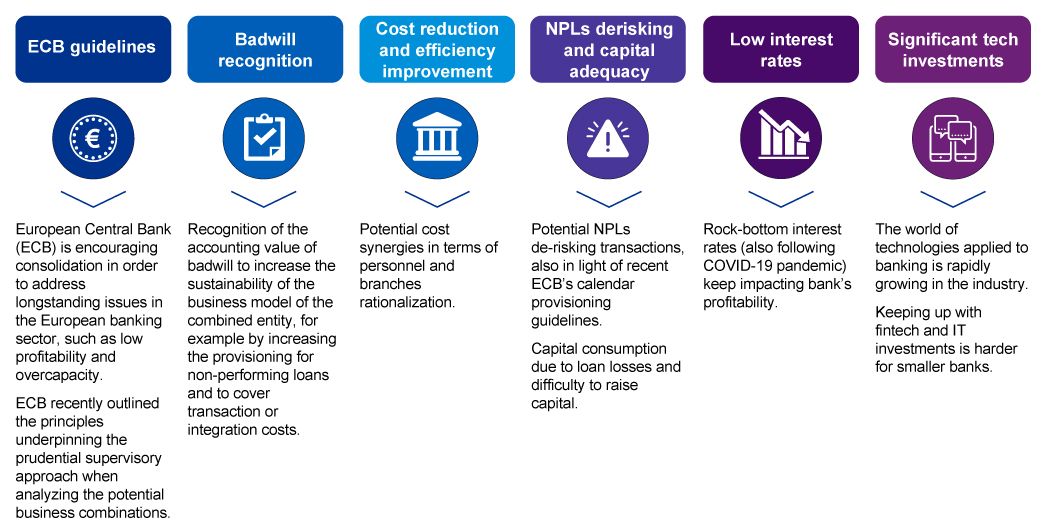

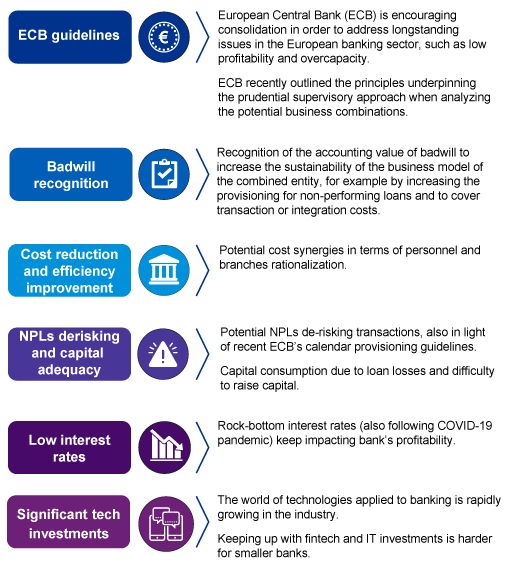

Within this context, domestic scale becomes a critical lever for reducing the number of bank branches and improving profitability. Domestic deals will continue to take precedence while in-market transactions will also be more viable. We see this with a few larger-scale deals going through this year, notably Intesa Sanpaolo acquired UBI Banca, the third largest bank in Italy, and CaixaBank merging with Bankia in Spain. Banco BPM is evaluating potential consolidation activities within the domestic space, while rumors persist about a potential merger between UBS and Credit Suisse. However, cross-border transactions may still take time to pick up pace — hindered by difficulties finding necessary synergies and structural impediments.

Looking at broader trends, the ECB has revived the M&A debate after publishing a draft guide to banking sector consolidation in July 2020. The comments are a potential framework to address longstanding issues in the European banking sector (namely profitability and overcapacity). The ECB has outlined expectations on three important areas in relation to sector consolidation: the setting of capital requirements and guidance, the treatment of badwill and the use of internal models by new entities.

Key drivers for European banking consolidation

European Bank M&A has reduced (US$ bn) over 2009-2020

Globally, few big-ticket deals kept the M&A market bubbling in 2019 and 2020 especially in core banking, with adjacent or aligned sectors such as payments, specialty finance and software companies servicing financial institutions, supported by underlying growth drivers, low cost funding and strategic motivation. Despite a formidable list of challenges faced by the European banks — the value and volume of mergers and acquisitions involving European banks fell to its lowest level since the global financial crisis. The drive to consolidate (from a supervisory perspective) is a logical conclusion to remedy some issues that the ECB has seen over a long period in the Eurozone banking market.

Scale alone may not drive profitability

Compared to selected institutions, we observe that European banks are not only smaller based on asset size than US and Chinese banks, they are also less profitable. Chinese banks and large US institutions are expected to generate a return on tangible equity above industry average of 7.9 percent for 2021E, while European institutions are still at a much lower level. Thus, the scope of needed consolidation for European banks is much higher.

Moreover, within the region, large banks (assets > €1,500 bn) are generating lower returns compared to many mid-sized banks. Thus, it appears that ‘scale’ as an M&A driver alone may not revive European bank profitability. Factors such as margin considerations, NPLs, business model fit, scope for meaningful cost cuts and potential value creation may take priority.

Source: KPMG analysis, Bloomberg, Capital IQ

Significant badwill could trigger further European consolidation

The ECB has allowed banks to recognize an accounting gain known as negative goodwill, or badwill, where the target is trading below 1x P/TBV and P/CET1 (acquiring bank below tangible book value, or at a lower price than the sum of its assets minus liabilities).

While most European banks are valued below accounting book value, M&A is probably going to involve some form of negative goodwill. The regulator highlighted an expectation that badwill will be used to increase the sustainability of the combined entity's business model (i.e. used in impairments and coverage at the time of the integration) and not put towards shareholder remuneration.

This appears to be a positive step for M&A activity as it recognizes the value of badwill as capital. Computation criteria remains unclear, however, especially for large deals. We expect this to accelerate consolidation among banks, particularly mid-sized banks. Some players may pursue a ‘wait and watch’ strategy until mid-2021 when institutions are able to evaluate NPLs resulting from COVID-19. Moreover, we expect badwill to act as a catalyst for domestic mergers rather than near-term cross-border transactions.

| Rank | Bank | Country | Exchange rate | Currency | Market cap (Euros bn) | Implied Badwill (Euros bn) | P/E'21 | P/TBV Last | ROTE'21 |

|---|---|---|---|---|---|---|---|---|---|

| 1 | HSBC | UK | 1.14 | GBP | 91.8 | 92.0 | 12.7x | 0.6x | 5.3% |

| 2 | BNP Paribas | France | — | EUR | 54.8 | 44.0 | 9.2x | 0.6x | 6.5% |

| 3 | UBS | Switzerland | 0.90 | CHF | 46.9 | 3.4 | 10.8x | 1.1x | 9.1% |

| 4 | Santander | Spain | — | EUR | 42.7 | 57.4 | 9.8x | 0.6x | 6.0% |

| 5 | Intesa Sanpaolo | Italy | — | EUR | 37.8 | 13.6 | 10.5x | 0.9x | 8.3% |

| 6 | ING | Netherlands | — | EUR | 32.8 | 20.9 | 9.8x | 06.x | 6.2% |

| 7 | Nordea | Finland | — | EUR | 29.7 | 1.0 | 10.9x | 1.1x | 9.7% |

| 8 | Llyods Banking Grou | UK | 1.14 | GBP | 29.4 | 17.4 | 11.0x | 0.7x | 6.5% |

| 9 | Credit Agricole | France | — | EUR | 28.5 | 29.3 | 10.4x | 0.7x | 7.1% |

| 10 | Barclays | UK | 1.14 | GBP | 27.0 | 33.5 | 9.7x | 0.5x | 5.5% |

| 11 | Credit Suisse | Switzerland | 0.90 | CHF | 26.5 | 13.5 | 8.6x | 0.7x | 7.8% |

| 12 | BBVA | Spain | — | EUR | 26.4 | 22.3 | 10.9x | 0.6x | 5.7% |

| 13 | KBC | Ireland | — | EUR | 24.9 | (6.0) | 14.4x | 1.4x | 9.8% |

| 14 | DNB | Norway | 0.10 | NOK | 24.0 | (3.9) | 12.8x | 1.2x | 9.0% |

| 15 | NatWest | UK | 1.14 | GBP | 21.7 | 22.3 | 17.1x | 0.6x | 4.1% |

| 16 | UniCredit | Italy | — | EUR | 20.3 | 35.5 | 11.0x | 0.4x | 3.8% |

| 17 | SEB | Sweden | 0.90 | SEK | 20.2 | (4.7) | 10.9x | 1.4x | 12.5% |

| 18 | Deutsche Bank | Germany | — | EUR | 19.6 | 36.3 | 23.7x | 0.4x | 1.8%x |

| 19 | Handelsbanken | Sweden | 0.09 | SEK | 17.2 | (1.4) | 10.8x | 1.2x | 10.4% |

| 20 | Standard Chartered | UK | 1.14 | GBP | 16.3 | 32.7 | 10.1x | 0.4x | 4.8% |

| 21 | Société Générale | France | — | EUR | 14.8 | 48.7 | 10.8x | 0.3x | 2.5% |

| 22 | CaixaBank | Spain | — | EUR | 13.2 | 11.9 | 12.0x | 0.6x | 5.3% |

| Average | 11.7x | 0.8x | 6.7% | ||||||

*Market cap for top 5 banks is €274bn and €421bn for top 10 banks

What to expect in the year ahead?

Challenges remain in 2021. The recessionary environment will weigh on bank loan demand while ever-increasing pressure on margins, default rates and NPL ratios may generate a sharp increase in non-performing loans which could severely impact some EU countries. M&A has been the obvious option for several years for the European banking industry. But with the ECB’s more relaxed tone, we expect in-market M&A to benefit from significant badwill being used to absorb upfront restructuring costs and additional provisions. Also, expect to see more consolidation among banks, mainly in over-banked markets like Spain, Italy and Germany.

Deal activity will be driven not only by scale issues but also by synergies, geographical and product diversification, strategic business fit and potential value creation. We see large deals already happening, but these M&A transactions may lead to even larger complications if external challenges like digitalization are not prioritized following the pandemic. For banks to benefit from consolidation, they must invest in relevant technological areas.

Cross-border transactions will take time, with the need to deliver credible synergies, accommodate regulatory constraints and navigate accounting headwinds.

Continue reading