People’s Republic of China – Rectification Filing Deadline if Resident Status Change

CN – Resident Status Changes: Rectification Filings

Actual days in the People’s Republic of China during 2020 may have changed significantly from the expectation at the start of the year. With the tax year having just come to an end, the time for making year-end adjustments to the amount of tax withheld during the year is fast approaching. A rectification filing might be required and the deadline for such corrections is 15 January 2021.

The 2020 tax year in the People’s Republic of China (“China”) has come to an end. Therefore, time for making year-end adjustments to the amount of tax withheld during the year is fast approaching. If an employee has a changed resident status during the year, and this has not already been reflected in the monthly withholding from the date of that change of status, a rectification filing might be required. The deadline for such corrections is 15 January 2021.

WHY THIS MATTERS

Actual days in China during 2020 may have changed significantly from the expectation at the start of the year.

Different tax calculation methods and filing obligations apply depending on whether a non-domiciled individual is resident or nonresident in the tax year concerned. In some cases, an individual’s resident status can only be determined with hindsight. Therefore, an adjustment to the withholding might be required to make sure the total tax withheld is correct.

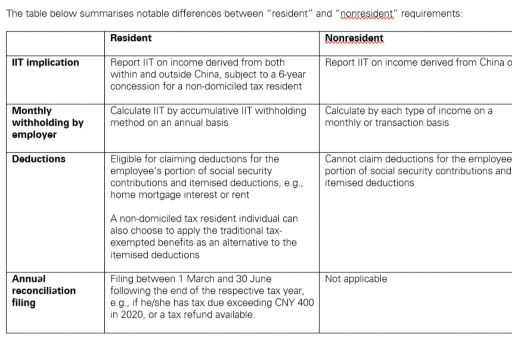

Distinction between “Resident” and “Nonresident” under Individual Income Tax (IIT)

The IIT obligation and calculation mechanisms for a resident individual and nonresident individual are different. Consequently, a change of tax residence status could result in a change in the amount of IIT payable.

Filing Obligation Due to Residence Status Change

According to prevailing PRC IIT regulations, employers shall make a pre-assessment of their employees’ tax residence status in China from the first monthly IIT filing based on his or her estimated number of days in China during a tax year.

Resident to Nonresident

If a non-domiciled employee is pre-determined to be a tax resident but later determines that he/she would not physically stay in China for 183 days or more in the tax year concerned, the employer should report and remit the tax shortfall or claim a tax refund due to the change in the employee’s residency status to the in-charge tax authority, by no later than 15 January immediately following the end of the respective tax year. No interest surcharge is imposed if the due date (15 January) is met.

Nonresident to Resident

In contrast, if the monthly tax of the employee is withheld using the nonresident method and the employee becomes a resident in the tax year concerned, the monthly IIT calculation method for nonresidents shall continue to apply. The rectification filing should be performed via the annual reconciliation filing from the following 1 March to 30 June.

KPMG NOTE

In 2020, due to the COVID-19 pandemic, China implemented travel restriction policies that have prevented the return of foreign expatriates to their place of work in China. In other cases, foreign employees may have remained in China longer than expected. As a consequence, actual days in China during 2020 may have changed significantly from the expectation at the start of the year. This change could affect the tax residence status of foreign expatriates. With expatriates returning home during the early days of the pandemic, and then having difficulty returning to China, we anticipate more resident-to-nonresident cases arising during the year.

In this regard, we suggest employers:

1. review the residency status during December by collecting the travel information of employees, identifying cases where residence status may have changed, and recalculating IIT for those employees whose resident status has been changed to nonresident;

2. consult with the in-charge tax officials or their qualified tax professional in advance regarding the practicalities of the rectification filing process and required documents, as these may vary between different tax bureaux;

3. reconsider, for the new year 2021, expatriates’ expected tax resident status based on their arrangements in light of the worldwide travel restrictions – the residence status should be determined accordingly at the beginning of the year.

VIEW ALL

The information contained in this newsletter was submitted by the KPMG International member firm in the People’s Republic of China.

SUBSCRIBE

To subscribe to GMS Flash Alert, fill out the subscription form.

© 2024 KPMG Advisory (China) Limited, a wholly foreign owned enterprise in China and KPMG Huazhen, a Sino-foreign joint venture in China, are member firms of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

KPMG International Cooperative (“KPMG International”) is a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm.

GMS Flash Alert is a Global Mobility Services publication of the KPMG LLP Washington National Tax practice. The KPMG name and logo are trademarks used under license by the independent member firms of the KPMG global organization. KPMG International Limited is a private English company limited by guarantee and does not provide services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.