14 May 2020 (Updated 25 July 2022)

Some contracts may be loss-making from the outset or become loss-making during their life cycle.

There may be various drivers for a loss-making contract, including external factors and a company’s own strategy.

Our new seven-step guide sets out a logical approach to accounting for loss-making contracts under IFRS® Accounting Standards.

Companies previously applying the ‘incremental cost’ approach will need to recognise bigger and potentially more provisions for onerous contracts. This follows recent amendments to IAS 37 Provisions, Contingent Liabilities and Contingent Assets, which clarify the types of costs a company includes as the ‘costs of fulfilling a contract’ when assessing whether a contract is onerous.

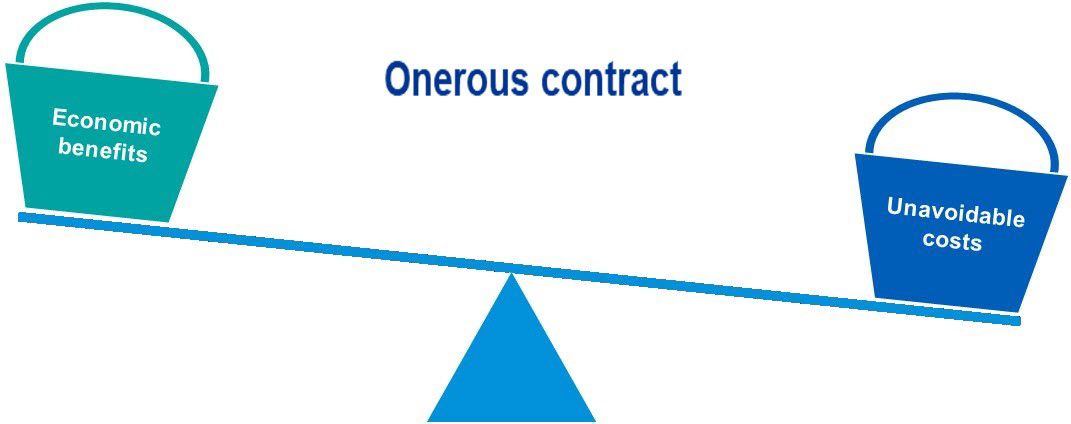

What’s the issue? – Determining if a contract is onerous

Following the withdrawal of IAS 11 Construction Contracts, companies apply the requirements in IAS 37 when determining whether a contract is onerous. These requirements specify that a contract is ‘onerous’ when the unavoidable costs of meeting the contractual obligations – i.e. the lower of the costs of fulfilling the contract and the costs of terminating it – outweigh the economic benefits.

While IAS 11 specified which costs were included as a cost of fulfilling a contract, IAS 37 did not, which led to diversity in practice. The International Accounting Standards Board’s amendments address this issue by clarifying those costs that comprise the costs of fulfilling a contract.

What is included in the costs to fulfil a contract?

The amendments clarify that the ‘costs of fulfilling a contract’ comprise both:

- the incremental costs – e.g. direct labour and materials; and

- an allocation of other direct costs – e.g. an allocation of the depreciation charge for an item of property, plant and equipment used in fulfilling the contract.

This clarification is unlikely to affect companies that already apply the ‘full cost’ approach, but those that apply the ‘incremental cost’ approach will need to recognise bigger and potentially more provisions.

Effective date and transition

The amendments apply for annual reporting periods beginning on or after 1 January 2022 to contracts existing at the date when the amendments are first applied. At the date of initial application, the cumulative effect of applying the amendments is recognised as an opening balance adjustment to retained earnings or other component of equity, as appropriate. The comparatives are not restated.

To find out more about the amendments, speak to your usual KPMG contact.

Read our seven-step guide

Our seven-step guide (PDF 454KB) sets out a logical approach to accounting for loss-making contracts under IFRS Accounting Standards.

© 2024 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.