Measuring the CSM Measuring the CSM

Key development

The revised IFRS 17 was published in mid-2020 with amendments in eight key areas of the standard including a deferred effective date of 1 January 2023.

IFRS 17 – Level of aggregation

International Accounting Standards Board meeting, February 2020

Allocating the CSM under the general measurement model to investment services

International Accounting Standards Board meetings, February 2020, May, March and January 2019

International Accounting Standards Board meeting, January 2020

IFRS 17 – Business combinations – contracts acquired in their settlement period

International Accounting Standards Board meeting, January 2020

Exposure draft of amendments to IFRS 17

International Accounting Standards Board, June 2019

Allocating the CSM under the general measurement model to reflect investment services

May, March and January 2019, and June 2018 International Accounting Standards Board meetings

September 2018 TRG meeting

Accounting for insurance risk consequent to an incurred claim

September 2018 TRG meeting

How to identify coverage units for CSM allocation (for contracts with no investment components)

May and February 2018 TRG meetings

How to identify coverage units for CSM allocation (for contracts with investment components)

June 2018 International Accounting Standards Board meeting and May 2018 TRG meeting

Level of aggregation

International Accounting Standards Board meeting, February 2020

What’s the issue?

IFRS 17 Insurance Contracts requires an entity to recognise and measure groups of insurance contracts. Groups are determined by:

- identifying portfolios of insurance contracts;

- dividing a portfolio into a minimum of three groups –

- those that are onerous at initial recognition,

- those that at initial recognition have no significant possibility of becoming onerous subsequently, and

- the remaining contracts in the portfolio; and

- dividing these into groups of contracts not issued more than one year apart (annual cohorts).

Applying the annual cohort requirement is costly when there is sharing of risks between different generations of policyholders. This is because the cash flows of one contract affect or are affected by contracts with other policyholders and also share in the same pool of underlying items as those other contracts (such as mutualised contracts). This is particularly complex if the entity has discretion over how it shares the returns from the underlying items between itself and the policyholders as a whole, or if the contracts are in the scope of the variable fee approach (VFA).

The loss of information about the effect of annual cohorts on the CSM would be limited when:

- the effect of financial guarantees over returns on underlying items in a contract is shared with other policyholders across generations and the entity’s remaining share is small; and

- a contract includes only small amounts of ‘fixed cash flows’ and the effect of changes in these is not shared with other policyholders, which means that the amount of fixed cash flows borne by the entity is small.

Although the Board did not ask a question on the annual cohort requirement in the exposure draft, the Board agreed to consider the feedback they received from respondents on applying the annual cohort requirement to insurance contracts with intergenerational sharing of risks between policyholders.

What did the Board decide?

The Board has confirmed that the annual cohort requirement in IFRS 17 will remain unchanged. The Board acknowledged that there may be limited circumstances when the cost of dividing portfolios into annual cohorts may outweigh the benefits. However, the complexity of developing criteria for an exemption could result in interpretation issues and inconsistent application, resulting in disrupting the implementation of IFRS 17 and reducing the benefits of its ongoing application.

What’s the impact?

The Board has now re-confirmed that the annual cohort requirements in IFRS 17 will not change. Entities now need to start focusing on how they will implement these requirements, especially those issuing mutualised contracts.

The Board has demonstrated that the purpose and benefits of annual cohorts contribute to providing fundamental information about trends in an insurer’s profits from insurance contracts over time, including, by:

- preventing onerous insurance contracts from being offset against profitable ones; and

- ensuring that profits associated with insurance contracts are fully recognised in profit or loss over the coverage period of those contracts.

For some contracts the requirement will be complex and costly to implement and require the exercise of judgement. However, the information provided by annual cohorts is critical to users of financial statements, especially given the current low interest rate environment impacting insurers.

Entities will need to consider how to allocate changes in the amount of the entity’s share of the fair value of the underlying items across annual cohorts that share in the same pool of underlying items. This will require significant judgement and entities should consider approaches that will generate useful information to users.

IFRS 17 permits entities to group contracts at a higher level than the annual cohort level if the same accounting outcome can be reached as if annual cohorts were applied. Before entities consider identifying such scenarios, they should evaluate the operational complexity of proving this outcome, not only at inception but on an on-going basis in all scenarios. For many contracts an entity is exposed to the impact of guarantees, experience gains and losses or other results through its variable fee.

Allocating the CSM under the general measurement model to investment services

February 2020, May, March and January 2019 International Accounting Standards Board meetings

What's the issue?

Recognition of the contractual service margin (CSM) in profit or loss under the general measurement model is currently determined by allocating the balance to coverage units, which are based on:

- the quantity of benefits provided under the contracts; and

- the contracts’ expected duration.

Under IFRS 17 Insurance Contracts, for insurance contracts that are not contracts with direct participation features, the quantity of benefits and contract duration relate only to insurance coverage and do not take into account any investment services.

The exposure draft (ED) included proposed amendments to allocate the CSM based on coverage units that are determined by considering both insurance coverage and any investment-return service, if certain criteria were met to identify an investment-return service. Feedback included concerns on the scope and operational complexity of the proposed amendment.

What did the Board decide?

At its meeting in February 2020, the Board confirmed:

- that entities will be required to identify coverage units for insurance contracts without direct participation features considering the quantity of benefits and expected period of investment-return service, if any, in addition to insurance coverage;

- the criteria for an investment-return service in paragraph 119B of the ED, replacing references to ‘positive investment return’ with ‘investment return’;

- the disclosure requirements as proposed in the ED; and

- the addition of an ‘insurance contract services’ definition in Appendix A.

The Board also confirmed an amendment to require an entity to include, as cash flows within the boundary of an insurance contract, costs related to investment activities to the extent the entity performs such activities to enhance benefits from insurance coverage for the policyholder – even if there is no investment-return service.

What’s the impact?

Entities would need to assess their insurance contracts to determine whether there is an investment-return service according to the confirmed proposals, which may affect the coverage period and determination of coverage units.

This means that, where relevant, entities would need to assess the relative weighting of insurance coverage and any investment-return services, and their pattern of delivery, to determine how the CSM is recognised in profit or loss on a systematic and rational basis for insurance contracts accounted for under the general measurement model. Entities may want to consider leveraging their approach for insurance contracts with direct participation features and for contracts that provide more than one type of insurance coverage when making this determination.

This assessment is important because it could affect:

- the timing of profit recognition;

- whether and to what degree related investment costs are included in the fulfilment cash flows; and

- whether insurance contracts qualify for the premium allocation approach, according to the amended definition of coverage period.

The inclusion of investment costs in the fulfilment cash flows may have wide-ranging impacts on entities’ systems and processes, profit recognition and financial statement presentation. More specifically, the addition of costs related to investment activities to the extent that the entity is performing the activities to enhance benefits for the policyholder will require entities to assess, and apply judgement, to determine whether certain investment costs are directly attributable to the fulfilment of the insurance contract. This concept of enhancing insurance benefits refers to a circumstance when an entity’s investment activities increase the value of the benefit to the policyholder. Additionally, entities will need to consider the inclusion of investment costs in the fulfilment cash flows when determining the discount rate to be applied, to make it consistent with the assumptions for cash flows.

The Board confirmed that the difference between an investment-return service and a contract where investment activities are used to enhance the benefit to the policyholder is that, without an investment component, the policyholder does not have a right to benefit from investment returns absent an insured event – an important distinction between the two.

When an investment component exists, it may be clear if an investment-return service is being provided. There will be circumstances when no investment-return service is provided but an investment component exists. For example, an entity does not provide an investment-return service if it provides only investment custody services regarding the investment component of an insurance contract. In many other cases, entities will need to use judgement – exercised consistently – in making this assessment.

Entities will be required to disclose quantitative information about the expected CSM release, rather than providing solely qualitative information. This requirement will help users of financial statements understand the profit recognition pattern for different products and enable them to compare those products across entities. It should be noted that this amount is unlikely to be the actual profit arising in future years as effects like the time value of money or experience gains or losses are excluded from the expected CSM release disclosure.

1 The Board discussed whether the term 'investment activities' will lead to interpretation issues and the staff agreed to consider the wording in the drafting of the revised version of IFRS 17.

Interim Reporting

January 2020 International Accounting Standards Board meeting

What’s the issue?

IAS®34 Interim Financial Reporting states that the frequency of an entity’s reporting should not affect the measurement of its annual results. However, IFRS 17 Insurance Contracts requires that an entity does not change the treatment of accounting estimates made in previous interim financial statements when applying IFRS 17 in subsequent interim financial statements or in the annual reporting period.

IFRS 17 generally requires changes in estimates of fulfilment cash flows related to future periods to adjust the contractual service margin (CSM), whereas experience adjustments – i.e. differences between expected and actual cash flows for the current and past period – are recognised in profit or loss immediately. This approach can result in different CSM and revenue for annual financial statements depending on the frequency of an entity’s reporting.

This issue creates particular complexities for groups that issue consolidated IAS 34 interim reports but whose subsidiaries are not required to do so (or prepare interim reports other than those addressed by IAS 34 or with a different frequency), and vice versa.

The Board did not propose amending IFRS 17 in this regard in the exposure draft but nevertheless received feedback on this aspect of IFRS 17, specifically that the issue would result in some entities:

- maintaining two sets of accounting estimates; and

- changing existing accounting practices for interim financial statements from a year-to-date basis to a period-to-period basis.

What did the Board decide in January 2020?

The Board tentatively decided to amend the requirements relating to interim financial statements in IFRS 17 to require an entity to:

- make an accounting policy choice whether to change the treatment of accounting estimates made in previous interim financial statements when applying IFRS 17 in subsequent interim financial statements and in the annual reporting period; and

- apply its choice of accounting policy to all insurance contracts issued and reinsurance contracts held.

What’s the impact and what should preparers be doing now?

The choice for entities is whether to:

- adopt a year-to-date approach in presenting their annual financial statements, ignoring results presented in any IAS 34 interim reporting during the year; or

- apply the current IFRS 17 requirement.

The differences that arise between these approaches are likely to be unpredictable (since they arise from changes in estimates) and so entities are likely to consider this accounting policy choice from an operational perspective, while also considering the approach adopted by their peers. During periods in which there are significant changes in estimates, an entity that selects an accounting policy that differs from its peer group is likely to find itself explaining different drivers of its results arising from the timing of how changes in estimates are reflected in its results.

In addition, the basis for accretion of interest will differ. For example, consider an entity that issues half-year reports in compliance with IAS 34. It forms a new group of contracts that will be originated through the year – it will accrete interest on the CSM in the first half of the year using the weighted average discount rate for that period, and in the second half using the average for the whole year. This may result in a difference in the CSM compared to an entity that does not issue interim reports and therefore would accrete interest on the CSM for all contracts in the group using the weighted average discount rate for the whole year.

The operational implications are also likely to be complex. Whichever accounting policy election is made, IFRS 17 will require estimates and assumptions to be updated at interim reporting dates.

Some insurers may already have started to build systems and processes to comply with the current requirement in IFRS 17 – many others will need to consider the pros and cons of the accounting policy election now open to them.

Some issues for preparers to consider |

|

|

|

|

|

|

|

|

|

|

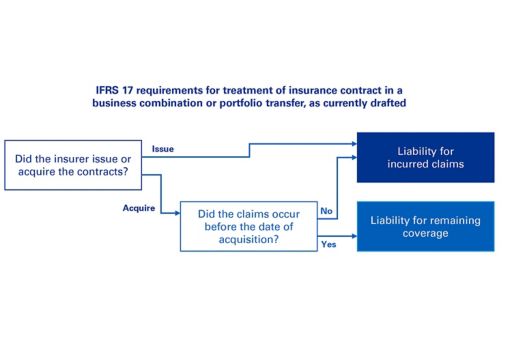

IFRS®17 – Business combinations – contracts acquired in their settlement period

January 2020 International Accounting Standards Board meeting

What’s the requirement?

Under IFRS 17 Insurance Contracts, an entity is required to assess whether a contract meets the definition of an insurance contract based on facts and circumstances at:

- inception, if the entity issued the contract; or

- the date the contract is acquired, if the entity acquired the contract either in a business combination within the scope of IFRS 3 Business Combinations, or a transfer of insurance contracts that do not form a business.

This differs from current accounting practice under which, as an exception to IFRS 3, insurance contracts acquired in a business combination or transfer are classified on the basis of contractual terms and other factors at their inception.

In principle, the insurance contracts originally issued by an entity (the acquiree) do not change when acquired by another entity (the acquirer). Following the introduction of IFRS 17, the exemption that permitted the acquirer to classify these contracts on the basis of the contractual terms and other factors at their inception can no longer be applied in accounting for business combinations or transfers. Once IFRS 17 is effective, acquirers will need to classify insurance contracts acquired as at the date of the business combination or transfer. This has the accounting consequence that where contracts are acquired with claims in their settlement period, such contracts are generally classified as if the insured event were the ultimate determination of the cost of the claims.

The assumed obligation would be classified as a liability for remaining coverage as shown below.

Click to enlarge diagram (JPG 42.3 KB)

{kind=link}

As a result, insurance contracts with claims in their settlement period may be treated differently depending on whether they were originated by the entity or were assumed in a business combination or transfer during their settlement period.

This may lead to system changes and related costs for contracts acquired during their settlement period, and some stakeholders believe that it will result in less useful information compared to current practice by insurers.

The Board did not propose amending IFRS 17’s guidance on its application to business combinations and insurance contracts acquired in the transfer of a business that do not form a business combination. However, as a result of comments received from outreach and comment letters it has discussed this topic during its redeliberations.

What did the Board decide in January 2020?

The Board confirmed its intention to retain unchanged the guidance in IFRS 17 for insurance contracts acquired in their settlement period. The Board argued that exempting insurance contracts acquired in a business combination from the general requirements would create complexity for users of financial statements and reduce comparability with other transactions. The Board noted that it believes it is important to align business combination accounting with other industries.

What’s the impact and what should preparers be doing?

Insurers have previously been able to apply a special exemption from the IFRS 3 accounting which applies to insurance contracts. This exemption will no longer be available under IFRS 17, which will impact the accounting for business combinations and portfolio transfers.

Under this revised approach, differences may arise between the identification of the service provided – and associated recognition and release of contractual service margin (CSM) – for the same contract between the acquiring entity and the acquiree entity in a business combination or transfer. For example, the acquirer would measure a contract acquired in its settlement period at fair value and recognise a CSM equal to the difference between the fair value and the present value of the fulfilment cash flows, and will recognise the entire fair value as revenue over the estimated settlement period. Determining the fair value and the resulting CSM requires the use of judgement. The acquiree would continue not to recognise a CSM or revenue for insurance contracts in their settlement period.

For insurers who issue short-term contracts – and therefore plan to account for the insurance contracts they issue under the premium allocation approach (PAA) – the removal of the exemption in IFRS 3 may add an additional layer of complexity and cost in accounting for insurance contracts acquired in business combinations and portfolio transfers. Contracts acquired which are expected to have a longer claims settlement period may not be eligible for the PAA in the acquirer’s financial statements – the acquiring entity may need to develop systems and processes to measure contracts using the general model and accommodate a CSM.

Accounting for business combinations and portfolio transfers under IFRS 17 will be challenging. Compared to current requirements, which permit an acquiring insurer to continue to use the classification in accordance with IFRS 4 Insurance Contracts at inception, certain exemptions have been removed and multiple reassessments may have to take place on acquisition, such as:

- the classification of contracts using the contractual terms and other factors as at that date;

- the determination of the measurement model; and

- the potential need for separation and combination of contracts.

On transition to IFRS 17, a number of simplifications can be applied, but these may not go as far as some hoped. In particular, the Board has tentatively confirmed that – on transition – an insurer need not recognise a CSM for settlement of claims incurred before an insurance contract was acquired. But this only applies if the contract was acquired before transition and the entity does not have the information to apply the IFRS 17 requirement retrospectively (see article).

Insurers should look at their business combinations that will have occurred before the transition date – especially businesses acquired in 2020 or 2021 – to see whether this applies. In addition, the process for the accounting analysis of business combinations and transfers after the effective date will change and become substantially more complex.

Exposure draft of amendments to IFRS 17

International Accounting Standards Board, June 2019

With the Board having published its exposure draft of the amendments to IFRS 17, you can find our latest insight and analysis at home.Kpmg/ifrs17amendments.

Allocating the CSM under the general measurement model to reflect investment services

May, March and January 2019, and June 2018 International Accounting Standards Board meetings

What's the issue?

Recognition of the CSM in profit or loss under the general measurement model is currently determined by allocating the balance to coverage units, which are determined by assessing:

- the quantity of benefits provided under the contracts; and

- the contracts’ expected duration.

Under IFRS 17, for insurance contracts that are not direct participating contracts, the quantity of benefits and contract duration relate only to insurance coverage and do not take into account any investment-related services.

At their June 2018 meeting, the Board proposed to clarify the definition of the coverage period for insurance contracts with direct participation features, emphasising that the coverage period for such contracts includes periods in which the insurer provides investment-related services.

What did the Board decide in January 2019?

The Board tentatively decided that the CSM under the general measurement model should be allocated based on coverage units that are determined by considering both insurance coverage and any investment return service, a new concept introduced for the purpose of this amendment.

The Board decided not to develop a prescriptive approach to determine when and to what extent investment return services are provided. The existence of an investment component is necessary for an investment return service to be considered in the CSM release, but is not sufficient on its own to demonstrate that an investment return service exists. Judgement – applied consistently – would be needed to identify an investment return service.

What did the Board decide in March 2019?

The Board tentatively decided to amend the disclosure requirements in IFRS 17, by requiring insurers to provide:

- quantitative disclosures, in appropriate time bands, of the expected recognition in profit or loss of the CSM remaining at the reporting date – currently IFRS 17 also allows only qualitative disclosures; and

- specific disclosures about their approach to assessing the relative weighting of the benefits provided by insurance coverage and investment-related services or investment return services.

What did the Board decide in May 2019?

The Board has tentatively decided that an investment return service can exist in an insurance contract only if:

- there is an investment component, or the policyholder has a right to withdraw an amount; and

- the investment component, or amount that the policyholder has a right to withdraw, is expected to include a positive investment return generated by the insurer’s investment activity.

Consistent with its decision in January, the Board agreed that satisfying the above criteria is necessary, but not sufficient on its own, to demonstrate that an investment return service exists – further analysis would still be needed to identify an investment return service.

Some Board members observed that, for these purposes, a ‘positive investment return’ does not necessarily equate to a return greater than zero. In a jurisdiction with a negative interest rate environment, a ‘positive investment return’ could be less than zero as long as the return is still higher than the benchmark yield.

What’s the impact?

Insurers would need to assess their insurance contracts to determine whether there is an investment return service according to the revised proposals, which may affect the coverage period and determination of coverage units.

This means that, where relevant, insurers would need to assess the relative weighting of insurance coverage and any investment return service and their pattern of delivery, on a systematic and rational basis, to determine how the CSM is recognised in profit or loss for insurance contracts accounted for under the general measurement model.

This decision is important because it would affect:

- the timing of profit recognition;

- whether related investment administration costs are included in the fulfilment cash flows; and potentially

- whether insurance contracts qualify for the premium allocation approach.

The inclusion of investment-related administrative costs in the fulfilment cash flows would have wide-ranging impacts on insurers’ systems and processes, profit recognition and financial statement presentation.

When an investment component exists, it may sometimes be clear whether an investment return service is being provided. For example, an insurer does not provide an investment return service if it provides only investment custody services regarding the investment component of an insurance contract. In many other cases, insurers would need to use judgement – exercised consistently – in making this assessment.

Insurers should start evaluating the implications of these proposed changes now. Given the impact on profit recognition it would also be advisable for insurers to update financial impact assessments for these proposals, noting that a number of them are inter-related and are influenced by other judgements. When designing their new processes, insurers should allow scope for adjustment and fine-tuning as the proposals are exposed for comment and eventually finalised.

Insurers will be required to disclose quantitative information about the expected CSM release, rather than provide solely qualitative information. This requirement will help users of financial statements understand the profit recognition pattern for different products and be able to compare those products across entities.

| Example: Investment return service in an insurance contract with no investment component |

|---|

Insurer X issues a deferred annuity contract to a policyholder, who pays the premiums up-front. Under the contract:

If the policyholder dies after conversion, but before the first annuity payment, then the policyholder receives nothing. In this situation, there is no investment component because a scenario exists in which the amount is not repaid. However, during the accumulation phase it is possible to conclude that an investment return service is being provided if the amount the policyholder can withdraw includes an investment return that is generated by the insurer’s investment activity and is expected to be positive. |

Applying the annual cohorts requirement to contracts that share in the return of a specified pool of underlying items

September 2018 TRG meeting

What's the issue?

Some insurance contracts share in the return of a specified pool of underlying items, with some of the return contractually passed from one group of policyholders to another – e.g. because of guarantees and proportionate sharing in the returns of the pool.

The basis for conclusions to IFRS 17 explains that, for contracts that fully share risks, the groups of contracts considered together will give the same results as a single combined risk-sharing portfolio.

It adds that IFRS 17 does not specify the methodology to be used to arrive at the reported amounts, and in some cases it is not necessary to restrict groups to annual cohorts to achieve the same accounting outcome.

The question that arises is: when would measuring the CSM at a higher level than an annual cohort level (e.g. portfolio level) achieve the same accounting outcome as measuring it at an annual cohort level?

What did the TRG discuss?

TRG members observed that when contracts share in 100 percent of the returns of a pool of underlying items that includes the insurance contracts themselves, the insurer would not be affected by the expected cash flows of each individual contract issued; and for groups of such contracts, the CSM would be zero. Accordingly, measuring the CSM at a level higher than the annual cohort would achieve the same outcome as applying the annual cohorts requirement.

TRG members observed that where the effects of risk sharing between policyholders comprise less than 100 percent of the returns, the expected cash flows could affect the insurer, resulting in a CSM being recognised for each group. In these cases, insurers would need to determine whether measuring the contracts at a higher level than the annual cohort would still result in the same outcome as applying the annual cohorts requirement.

What's the impact?

Insurers may be able to measure contracts with a risk-sharing mechanism at a higher level than the annual cohort only if they can achieve the same accounting outcome. They would need to assess whether these contracts share risks to an extent that would allow them to achieve that outcome.

Insurers would also be expected to perform an analysis to confirm that the different measurement levels would not impact the measurement outcome.

Accounting for insurance risk consequent to an incurred claim

September 2018 TRG meeting

What's the issue?

There are certain situations where an incurred claim creates an insurance risk for an insurer that would not exist if no claim were made.

A common example is a disability contract that provides coverage for a policyholder becoming disabled during a specified period. If a claim is made, then the insurer is required to make regular payments to the policyholder until they either recover, reach a specified age or die. In this scenario, the amount of the claim is uncertain and subject to insurance risk.

A question that arises is whether an insurer should record such an obligation as:

- a liability for incurred claims – i.e. the insured event in the example above is the policyholder becoming disabled; or

- liability for remaining coverage – i.e. the insured event is the policyholder becoming and remaining disabled.

What did the TRG discuss?

TRG members observed that different interpretations of what the insured event is for these types of contracts are possible when applying IFRS 17. Therefore, the obligation may be treated as a liability for incurred claims or a liability for remaining coverage.

TRG members observed that determining the appropriate accounting policy requires the exercise of judgement, based on the specific facts and circumstances, considering which interpretation provides the most useful information about the nature of the services provided. These accounting policies should be applied consistently to similar transactions and over time.

What's the impact?

Whether expected regular payments are classified as a liability for incurred claims or as a liability for remaining coverage has no impact on the cash flows that are included in the insurance contract measurement. However, it directly impacts the determination and allocation of the CSM to profit or loss as shown below.

| Accounting for payments to the policyholder | Effect on profit recognition | Effect on recognition of changes in estimates of future cash flows | Complexity of the approach |

| Liability for incurred claims | Shorter recognition period | Changes are recognised immediately, which can lead to volatility in profit or loss | Less complex |

| Liability for remaining coverage | Longer recognition period |

Volatility related to changes is partly absorbed by the CSM | More complex |

In some cases, the classification may also impact the accounting model applicable to the insurance contracts – e.g. whether a group of contracts qualifies for the premium allocation approach.

It will be crucial for insurers to make transparent disclosures as required by IFRS 17, including those about significant judgements, to allow financial statement users to understand and compare the performance of insurers.

How to identify coverage units for CSM allocation (for contracts with no investment components)

May and February 2018 TRG meetings

What’s the issue?

The CSM of a group of insurance contracts is recognised in profit or loss based on identifying the coverage units in the group. These are determined by considering, for each contract, the quantity of benefits provided and its expected coverage duration.

Due to the variety and complexity of insurance products, determining the quantity of benefits provided under each contract in a group of insurance contracts is an area of judgement.

The question that arises is what factors should be considered in determining the coverage units in a group of contracts, considering both the contracts’ expected duration and quantity of benefits.

What did the TRG discuss?

The objective of the release of the CSM is to reflect services provided in each period. Since IFRS 17 does not specify how to determine the coverage units in a group, TRG members agreed that an insurer needs to apply judgement to determine a systematic and rational method for estimating the services provided for each group of contracts.

TRG members observed that coverage units should reflect:

- expectations of lapses and cancellations of contracts, as well as the likelihood of an insured event occurring to the extent that they it would affect the expected duration of contracts in the group; and

- different levels of service across the periods being covered – because the benefits of being able to make a claim are affected by the amount that a policyholder can claim.

Depending on the facts and circumstances, methods that may achieve the objective include:

- a straight-line allocation over the passage of time, reflecting the number of contracts in a group;

- using the maximum contractual cover in each period;

- using the amount that the insurer expects the policyholder to be able to validly claim in each period if an insured event occurs;

- methods based on expected cash flows; and

- methods based on premiums.

It was noted that methods based on premiums would not be appropriate if the premiums:

- are receivable in periods different from those in which services are provided;

- reflect different probabilities of claims for the same type of insured event in different periods (rather than different levels of service of standing ready to meet the claims); or

- reflect different levels of profitability in contracts.

TRG members also appeared to agree that methods that result in no CSM allocation to periods in which the insurer stands ready to meet valid claims would not meet the objective.

What’s the impact?

Many groups of insurance contracts will contain contracts with similar risks and levels of cover provided.

For groups like these, a method primarily based on the passage of time that reflects the number of contracts in the group may be a reasonable proxy for services provided in each period.

For other, more complex groups of insurance contracts (e.g. groups that contain contracts with different or multiple risks, or contracts with different levels of cover provided over different periods), other methods would need to be developed to achieve the objective of the CSM release.

Identifying a practical and systematic approach for determining the quantity of benefits provided by these contracts using information available to the insurer may ease the operational challenges of this new requirement.

How to identify coverage units for CSM allocation (for contracts with investment components)

June 2018 International Accounting Standards Board meeting and May 2018 TRG meeting

What's the issue?

A variety of insurance contracts provide investment-related services. A key question is whether their coverage period and coverage units should be determined with reference to insurance coverage only, or with reference to insurance coverage and the investment-related services. Answering this question is necessary for determining the CSM recognised in profit or loss in each period.

What did the TRG discuss in May 2018?

IFRS 17 identifies direct participating contracts as contracts that provide both insurance services and investment-related services. Based on this, TRG members agreed that, for direct participating contracts, determining the quantity of benefits provided and the expected coverage duration – and hence, the CSM recognised in profit or loss in each period – should reflect both insurance and investment-related services provided under the contract.

For contracts with investment-related services that are not direct participating contracts, the staff and some TRG members believed that, based on the wording of IFRS 17, the coverage period and coverage units are determined by reference to insurance services only. However, most TRG members disagreed that such contracts should be treated as providing only insurance services.

What did the Board discuss in June 2018?

The Board decided to amend the definition of the coverage period for direct participating contracts in the next cycle of annual improvements to IFRS. The amendment would clarify that the coverage period for these contracts includes periods in which the entity provides coverage for insured events or investment-related services.

At a future meeting, the Board will receive a more comprehensive list of items that have been identified as raising practical, interpretative and other implementation challenges.

Update, January 2019: The International Accounting Standards Board has proposed amendments to IFRS 17 that affect how the CSM would be allocated under the general measurement model to investment services.

What's the impact?

The proposed amendment for direct participating contracts appears consistent with the way these contracts are identified and accounted for (i.e. applying the variable fee approach), and reflects the contracts’ characteristics. Given the wide range of these contracts, assessing the pattern of service provision reflecting both insurance and investment-related services will require judgement.

However, at the May TRG meeting some TRG members observed that if investment-related services provided are reflected in CSM allocation only for direct participating contracts, then this could result in what they believe are economically similar contracts having significantly different recognition patterns, depending on whether they qualify as direct participating contracts or not. This is because they consider that insurance contracts that are not direct participating contracts may still provide significant investment-related services.

Although the June Board meeting has provided additional clarity, some uncertainty still remains over whether the Board will hold a substantive discussion about contracts with investment-related services that are not direct participating contracts. Many preparers will want to continue to progress the overall design of their IFRS 17 systems and processes, but will need to be mindful to build in flexibility to accommodate the continuation of this discussion. We recommend that you stay tuned for further developments in this area.

About this page

This topic page is part of our Insurance – Transition to IFRS 17 series, which covers the discussions of the International Accounting Standards Board and its Transition Resource Group (TRG) regarding the new insurance contracts standard.

You can also find more insight and analysis on the new insurance contracts standard at IFRS – Insurance.