‘Banking’ on net zero emissions by 2050 'Banking' on net zero emissions by 2050

The net zero ambition

Major banks and investors are pledging to make their portfolios net zero by 2050; 43 banks from 23 countries recently launched the ‘UN-convened Net Zero Banking Alliance’ and many others have made similar commitments outside of this. Those that haven’t are under increasing pressure from investors to follow suit and commit to aligning their lending and investment portfolios with net zero emissions by 2050.

Making headline announcements is important to show ambition, but stakeholders are increasingly demanding interim, science-based targets to complement these longer-term ambitions. Setting a science-based target supports alignment of lending and investment activities with the Paris Agreement and helps banks in defining their trajectory to net zero with interim targets.

How science-based targets and net zero targets interact

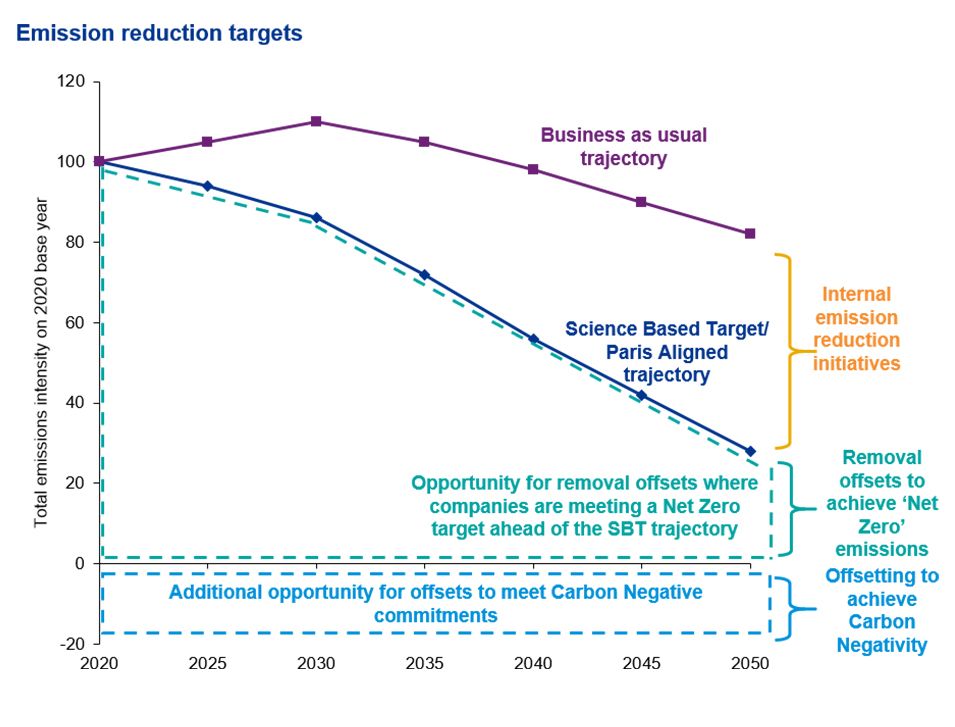

Science-based targets provide companies with a clearly defined path to reduce emissions in line with the Paris Agreement goals – limiting global warming to well-below 2°C above pre-industrial levels and pursuing efforts to limit warming to 1.5°C.

Net zero targets imply a company will achieve a balance between the amount of greenhouse gas emissions produced and the amount removed from the atmosphere by a set date.

The key difference between the two types of targets is that science-based targets do not allow carbon offsetting to achieve targets. In order to achieve net zero, banks must develop a carbon offsetting strategy which is in line with evolving market expectations – focussing on permanent carbon removal not reduction.

Targets require measurement

Turning high-level commitments into actionable insights and strategy development requires a granular understanding of a bank’s portfolio.

Measuring a bank’s climate impact is easier said than done and requires new data points to be collected (or proxied) and methodologies to be developed. Such as:

- Counterparty level data including scope 1 and 2 emissions (and where material, scope 3), production profile and financial data;

- Paris-aligned climate scenarios, enriching those publicly available through organisations such as Network for Greening the Financial System and the Bank of England;

- Sector-level transition pathways, including the future energy mix as well as sector specific considerations e.g. timing of transition to Electric Vehicles, ideally on a regional or country basis reflecting the differing rates of transition in different locations.

Using these data points and climate modelling infrastructures, banks can calculate their current financed emissions (for example via absolute emissions or emissions intensity) and portfolio temperature alignment, in order to understand the level of alignment to a net zero trajectory at a sector level.

Several initiatives and methodologies have begun to emerge to support banks. In September 2020, 2DII launched PACTA for banks, to provide banks with a climate scenario analysis toolkit for select sectors in corporate lending portfolios. In the same month, SBT set out guidance for financial institutions setting science-based targets. Then PCAF, a global partnership of financial institutions, launched a standard methodology for measuring financed emissions in November 2020. However, there is no single methodology or solution to guide banks through financed emissions measurement and temperature alignment. Moreover, there is no solution that provides a granular and readily comparable scenario for banks to use to calculate financed emissions.

Measurement enables action

Understanding and measuring the temperature alignment of a portfolio is just the first step in enabling a bank to meet its net zero target. Banks need to take action to align their portfolio’s emissions to their targets. Developing a strategy and taking actions that drives change both internally and supports clients through the transition is key for any bank to align to net zero. Banks will need to:

- Incorporate emissions metrics and targets into their risk appetite;

- Develop lending policies and strategies that are aligned to metrics and targets (reflecting not just carbon risk, but broader climate-related, ESG and Enterprise Risks as well);

- Identify opportunities to green their portfolios through new growth sectors;

- Support existing clients’ transition to the low carbon economy.

Competition for green finance will get tougher

As banks strive to green their portfolios, competition for green products will grow and attracting customers with the right credentials to enable a bank to stay aligned to net zero will get tougher.

There are already warnings of a ‘green bubble’ in the asset management industry, which could quickly be replicated in corporate lending as competition for green lending options continues to grow.

Banks may have to offer ‘green’ loans with preferential and competitive financing terms to attract customers from ‘green’ industries. Without proper governance, and a clear strategy of how different risks will be balanced, demand for green loans may result in financing of companies with bad fundamentals that otherwise would have been declined.

Furthermore, pricing for those in ‘brown’ industries may be offered at higher rates to try and reduce lending in these sectors and avoid the negative impact on net zero alignment metrics. This may result in ‘brown’ lending being forced into the shadow banking industry, where financing is less easily influenced by policy makers and investors. For some, this may reduce their longer-term ability to transition at all, proving binary for their longevity.