Reinventing PPPs to make them work for health systems in Saudi Arabia

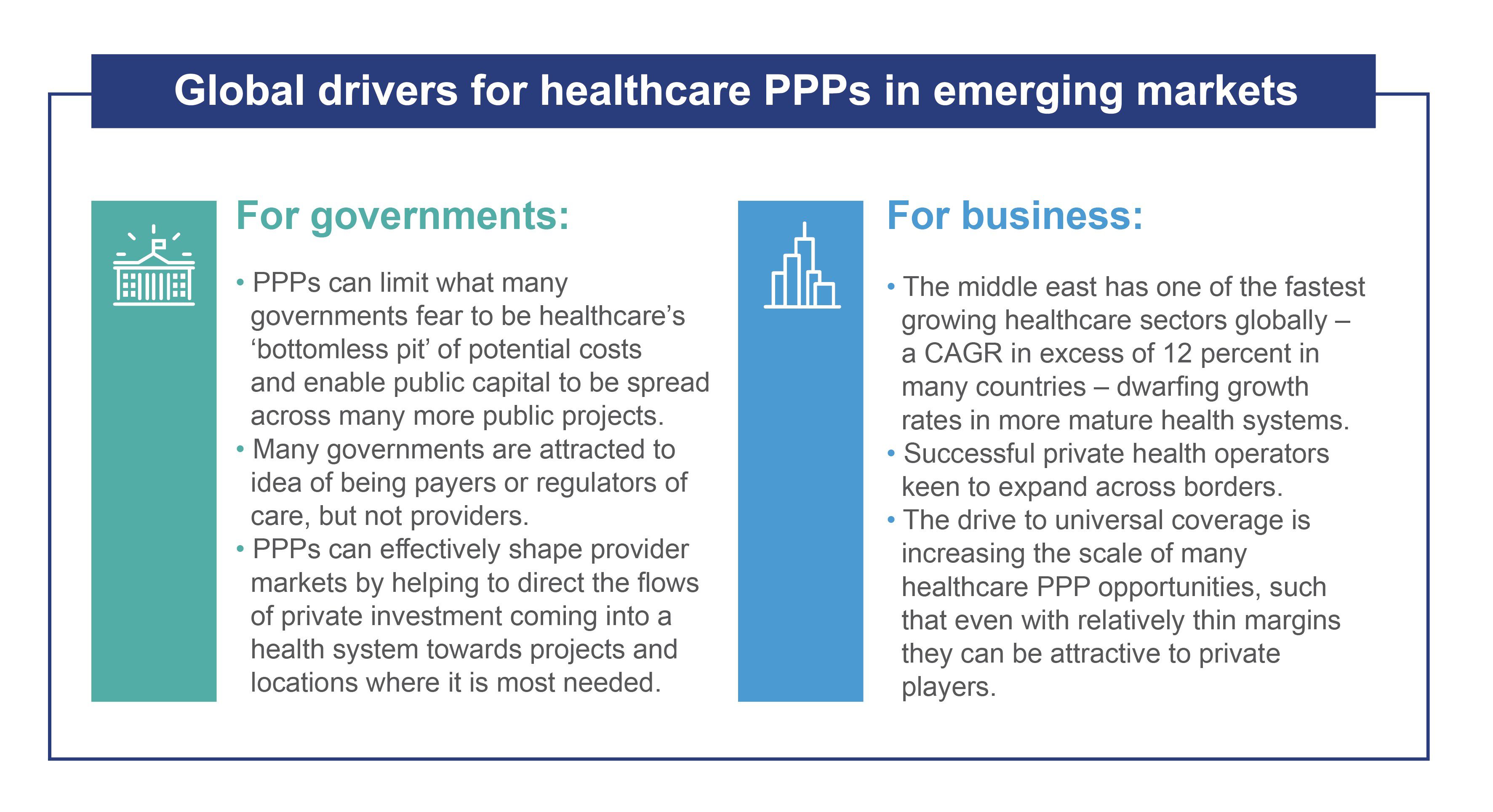

Health systems in Saudi Arabia, as well as those in the Gulf and across the Levant would appear, at least on paper, to be the ideal enabling environment for public-private partnerships (PPPs). A track record of openness to private sector input, supportive legislation and political messaging, and health sector growth many times that of Western markets should all add up to a buoyant market.

Yet as this brief shows, healthcare PPPs are having a start that is slower than expected – with just a handful of confirmed projects, and fewer still unequivocal success stories. Some commentators have even gone so far as to declare the ‘demise’ of the PPP concept in the GCC. This is a premature judgement for sure, but one that begs the question of why we see so many governments hold back from making tangible progress of PPPs having put so much emphasis on giving them permission.

Drawing on our local insights into the health systems, we find that in many cases there is good reason for this reticence to ‘take the plunge’. As a concept, healthcare PPPs have their roots in Western health systems looking to update existing elements of an ageing or outdated delivery system. Classical PPPs therefore developed primarily as an infrastructure and investment tool, yet the potential of the private sector in Saudi Arabia is not primarily in these areas but in innovation, implementation and insight to create efficient, high quality 21st century healthcare: reinvention, rather than renewal.

For this reason, we need to get back to the fundamentals of how the private sector can help to achieve their goals for the next 30 years, as part of an ecosystem that includes the full range of potential partnership models – including PPPs but many more partnership forms besides.

What matters is what we term ‘the triple win’ – finding a way to balance the interests of governments, businesses and citizens to achieve maximum social development for available state resources, achieve higher quality care at the same or lower cost for patients, and a sustainable return on investment for the private sector.

Our research shows that this shift is taking place in many other health systems that are pursuing PPPs from a similar place, and that the results can look very different from the traditional PPP hospital builds: leading to investments in clinical training, digital primary care, chronic disease management and much more. It also brings new kinds of partners into the health system, such as telecoms companies and retail chains, and results in novel partnership forms and contractual models.

In this sense, the fact that health has been overlooked as an early adopter for PPPs in the country and the region may be a blessing in disguise. The perceived complexity of healthcare has put off many governments and investors, when in fact this makes it an ideal candidate to develop this new approach, moving away from ‘me too’ infrastructure builds to more sophisticated means of extracting value from private sector human and financial capital.