Introduction of the VAT e-commerce package is to bring major changes likely to impact the operations of entities managing electronic interfaces (EI), including marketplaces, platforms, portals, or similar means. As of 1 July 2021, the role of electronic interfaces in terms of reporting, record-keeping and VAT duties is to change radically.

The purpose behind the changes

Sales made to consumers within the EU, both as part of the trading between Member States and in terms of import from third countries, are, to a large extent, effectuated via online marketplaces. The EU has been long struggling with effective collection of VAT on such transactions, especially in the case of sellers from outside the EU. In fact, the main challenge posed by sales via electronic interfaces is related to relatively high administrative burden and costs of settling tax on such transactions borne by companies and fiscal administration.

Marketplace as a VAT payer

To tackle this issue, the EU VAT e-commerce package was armed with a raft of provisions imposing a requirement to collect VAT on taxpayers facilitating certain categories of supplies via electronic interfaces. The main goal is to shift the burden of performing duties stipulated by VAT provisions from a relatively wide group of companies (i.e. the so-called underlying suppliers) to a much smaller group of electronic interface operators.

To achieve it, a new Article 14a was added to the EU VAT Directive, providing that where a taxable person facilitates, through the use of an electronic interface such as a marketplace, platform, portal, or similar means,

- distance sales of goods imported from third territories or third countries in consignments of an intrinsic value not exceeding EUR 150,

- the supply of goods within the Community by a taxable person not established within the Community to a non-taxable person,

that taxable person shall be deemed to have received and supplied those goods himself.

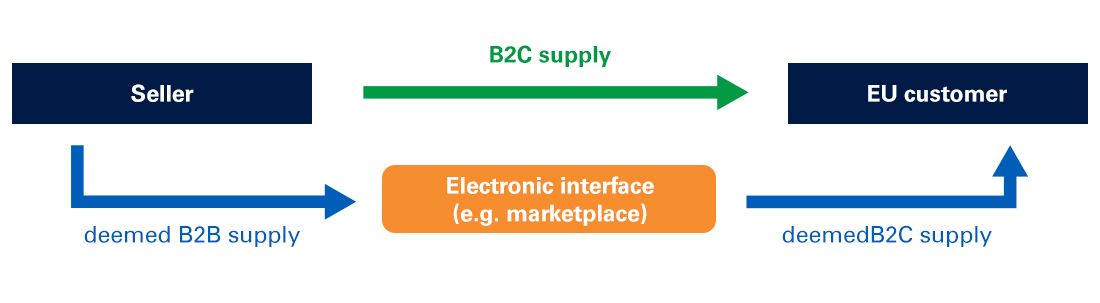

The above provisions creates fiction that a taxable person facilitating the supplies made by underlying suppliers through the use of an electronic interface is in fact:

- deemed to have received (purchased) those goods himself (an assumption is made that a B2B supply of goods takes place between the underlying supplier and the electronic interface) and

- deemed to have supplied those goods (an assumption is made that a B2C supply of goods takes place between the electronic interface and the end buyer, i.e. the consumer, who actually purchases the goods).

As a result, the underlying supply will have no VAT effects (it will remain VAT transparent), while VAT effects will be brought by the two deemed supplies, where the dispatch or transport of the goods will be always assigned to the deemed supply made by the electronic interfaces to the end buyer. For sales of imported goods, the first supply (between the underlying supplier and the electronic interface, B2B) will be taxed in the third country (i.e. the country of dispatch), while in the case of supply of goods within the Community, the amended regulations will provide for exemption with the right of deduction (in Poland 0 % VAT rate).

Consequently, the second B2C supply, i.e. the one taking place between the electronic interface and the consumer, will be in fact subject to real taxation. This means that the electronic interface operator will be treated as a VAT payer performing supplies of goods to the consumer, with all the consequences it gives rise to, especially in terms of settling, declaring, and documenting such a transaction. Importantly, the electronic interface will be able to apply the VAT-OSS and VAT-IOSS procedures on the same terms as other taxpayers.

It should be kept in mind, however, that the provisions brought about by the VAT e-commerce package will relate solely to electronic interfaces that facilitate the specific types of supplies. As noted in the explanatory notes to the draft bill implementing the provisions of VAT e-commerce package into the Polish legislation, an “electronic interface” shall mean any device or software allowing to establish contact between the user who is the seller and the user who makes the purchase. The provisions of the amended VAT Act (Article 7a(1)) will intentionally list only examples of possible types of electronic interfaces in order to also cover the types thereof that may appear in the future.

In turn, details on what should be understood as “facilitating” are provided by Article 5b of the Council Implementing Regulation (EU) 2019/2026 of 21 November 2019 amending Implementing Regulation (EU) No 282/2011 as well as by the European Commission's Explanatory Notes.

In practice, doubts may arise whether in a specific case we are dealing with an operator managing an "electronic interface" within the meaning of the above-mentioned regulations and whether the electronic interface is used to facilitate sales.

In theory, each case should be assessed on an individual basis, considering the type of business activity carried out by the entity, the purpose of the implemented provisions, and individual actions encompassed by services provided to sellers.

In a situation where we deal with the electronic interface obligated to collect VAT, further considerations should include the operators’ responsibility for VAT collection (within the scope of information on transactions obtained from the sellers) and how the marketplace’s position may be secured in this regard.

The record-keeping obligations

Importantly, pursuant to the VAT e-commerce package provisions, selected operators of electronic interfaces, used to provide services and supply goods to consumers within the EU, shall keep electronic records of these transactions, made available electronically on request to the competent tax authorities.

Authors:

Izabela Jędra, Assistant Manager, Indirect Tax Services, KPMG in Poland

Kamil Chmielewski, Supervisor, Indirect Tax Services, KPMG in Poland

Frontiers in tax. Polish edition | June 2021

This issue of the Magazine explores the key VAT-related changes, including introduction of a new type of e-invoice, commonly referred to as structured invoice, the SLIM VAT package, the VAT e-Commerce package, along with the latest developments related to the sugar tax.

In this issue:

- Introduction – Tomasz Bełdyga

- Structured invoice: a new VAT invoicing scheme – Łukasz Daniek

- VAT-slimming in practice – Tomasz Piotrowski

- The next edition of the SLIM VAT package – Natalia Kłoś, Patryk Roratowski

- The VAT E-Commerce Package: VAT Changes for B2C Trade– Izabela Jędra, Kamil Chmielewski

- VAT E-Commerce Package: Marketplaces and the new roles they are about to assume – Izabela Jędra, Kamil Chmielewski

- A draft Decree on amending the extended SAF_T file (JPK_VAT) – Izabela Jędra, Kamil Chmielewski

- Reverse charge on VAT: a landmark ruling of CJEU – Marek Bielawski

- Sugar tax – Zbigniew Sobecki, Rafał Roczniak

| Please login or register to download the PDF file |

|---|