Digital Banking in the Philippines

Digital innovation programs have already been part of many organizations’ agenda even before the pandemic. However, the pandemic highlighted the need for organizations to increase their investment in technology and people in order to accelerate their digital transformation journeys. Organizations today are pushing their boundaries to become operationally resilient, agile and customer-focused. In KPMG’s 2020 CEO Outlook COVID-19 Special Edition, we found that 75 percent of CEOs say the pandemic has accelerated the creation of a seamless digital customer experience, with over 1 in 5 (22 percent) of those saying progress “has sharply accelerated, putting us years in advance of where we expected to be”.1

The success of these innovation programs and digital transformation efforts define how we move forward in the new reality. The banking sector must also capitalize on these new technologies to address changing customer needs and behaviors. In the Philippines, the rise of fintech companies and new bank players paved the way for customers to experience new and exciting services, other than those of the traditional brick-and-mortar business model.

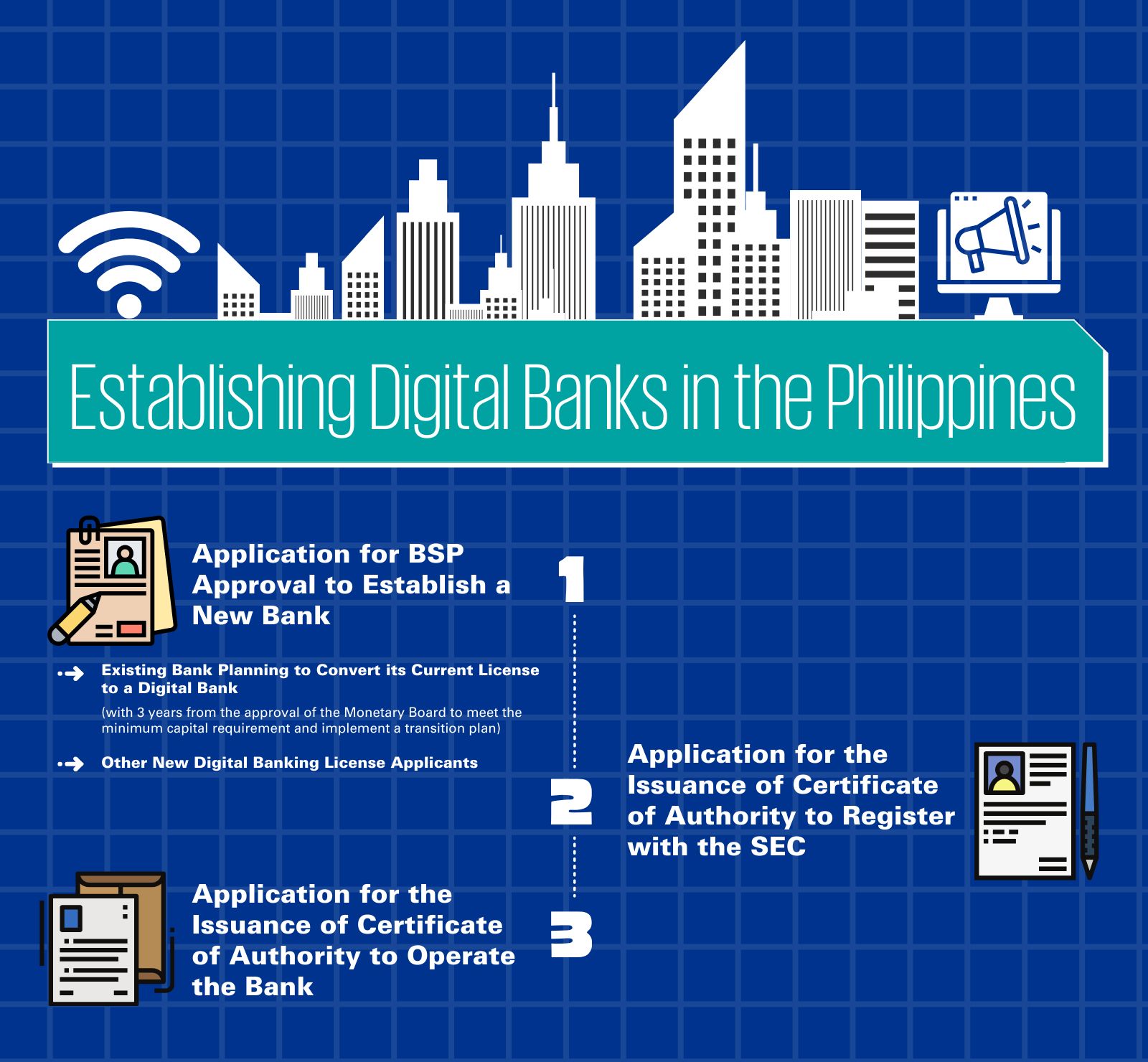

In recognition of today’s trends, the Bangko Sentral ng Pilipinas (BSP) issued Circular No. 1105 last December 2020 to add digital banks to the country’s classification of banks alongside universal, thrift, commercial, Islamic, rural and cooperative banks; and, provide guidelines for establishing a digital banks in the Philippines.

1 Source: KPMG 2020 CEO Outlook COVID-19 Special Edition

Here are some things to note:

Digital Bank

A digital bank offers financial products and services that are processed end-to-end through a digital platform and/or electronic channels with no physical branch/sub-branch or branch-lite unit offering financial products and services

Capitalization and initial expenditures

∎ Minimum capitalization shall be Php 1 billion

∎ License fee of Php 12.5 million

∎ Application fee of Php 250,000.00

Organization

∎ Sound digital governance, robust, secure and resilient technology infrastructure, and effective data management strategy and practices

∎ Subject to the prudential requirements set out by the BSP

∎ Third party expert detailed review and assessment of the supporting IT systems and infrastructure vis-à-vis the digital banking business model

∎ A principal/head office in the Philippines to serve as the main point of contact for stakeholders

Other requirements and limitations

∎ Submission of applicable requirements in offering Electronic Payments and Financial Services (MORB Sec. 701 and Appendix 141)

∎ Limits of stockholdings in a single bank (Section 122)

∎ Limits on Investment in the equities of financial allied undertakings (Section 373)

Jallain Marcel S. Manrique

Head, Technology Consulting

KPMG in the Philippines

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia