Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia

KPMG’s Financial Institutions Performance Survey (FIPS) reports have provided insights into New Zealand’s financial services sector for over 30 years. Each edition presents industry commentary and analysis on the performance of New Zealand registered banks, together with a range of topical articles from industry experts, regulators and our own business leaders.

The ongoing impact of CCCFA changes

The topic that has been the most passionately discussed was the amendments to the Credit Contracts and Consumer Finance Act (CCCFA). When the changes were mooted, two things happened – commentators all agreed with the concept of promoting responsible lending and ensuring no one was harmed but simultaneously issued warnings in advance about the impact the detailed requirements within the code would have on processing times, decision making and ultimately the amount of and cost of lending that would occur.

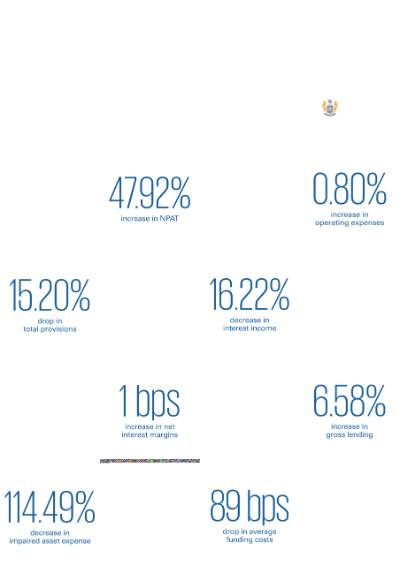

Highest profit growth on record for banking sector

KPMG’s Financial Institutions Performance Survey (FIPS) Bank review of 2021 has revealed a strong increase in net profit after tax (NPAT), showing the banking sector’s recovery from the initial shock of Covid-19 in 2020.

The results show NPAT up $1.99 billion (47.92%) from 2020 to reach $6.13 billion for the year, marking the first year that FIPS has reported a NPAT of over $6 billion.

The key driver for the increase in NPAT was a reversal in impaired asset expense of $1.69 billion (114.49%) to a $213.43 million impairment reduction in 2021.

In addition, net interest income rose by 7.07% to $765.62 million and non-interest income contributed a 5.94% ($159.08 million) increase. The net interest income increase was driven by a 1 basis point (bp) increase in the net interest margin (NIM) for the banking sector and a 6.55% increase in lending across the sector, fuelled by a strong property and mortgage market.

The increased levels of profit were further influenced by operating expenses (excluding amortisation) only increasing by a marginal $47.21 million (0.80%).

An over-heated housing market

The housing market continued to be a key topic of discussion in 2021, especially the annual house price growth rate of 27%. The housing price increases didn’t deter buyers, with annual sector lending increasing from $296 billion to $326 billion in 2021.

Navigating living with Covid-19

A prominent and recurring discussion point across survey participants was dealing with Covid-19 as a constant – and the continuous flow on effect for both banks and businesses as the balance of health and economic impacts becomes more important than ever.