The publication on 25 March 2021 of Council Directive (EU) 2021/514 (‘DAC7’) extends the EU tax transparency rules to digital platforms and introduces an obligation for platform operators to provide information on income derived by sellers through platforms, as from 2023 onwards. The information collected will be shared with the tax authorities of the concerned Member States with the aim of addressing the lack of tax compliance and the under-declaration of income earned from commercial activities carried out with the intermediation of such digital platforms.

Both EU and non-EU platform operators are impacted, with the latter having a reporting obligation if they facilitate reportable commercial activities of EU sellers or the rental of immovable property located in the EU regardless of the place of residence of the sellers.

Examples of potentially affected platforms include: livestreaming apps that allow users to access events / performances at a fee, digital platforms facilitating peer-to-peer sale of goods or services between users (socalled collaborative / pooling economy) and platforms servicing the on-demand / access economy like car-pooling or ride-hailing apps, marketplace for freelance services, tech companies providing food delivery platforms, virtual marketplaces for all sorts of goods (sports apparel, clothing, photos, etc.), yacht chartering platforms, online travel agents, open online course providers and marketplace auction platforms, amongst others.

Sellers (or providers of services), whether individuals or of any legal form, making use of such platforms for commercial purposes will have their details and income notified to the tax authorities of the EU Member States.

Exclusions

Platforms exclusively allowing for the processing of payments, the listing or advertising of goods/services and the redirection/transfer of users elsewhere are not captured by DAC7.

While initially included in the scope, investment- and lending-based crowdfunding were excluded from DAC7.

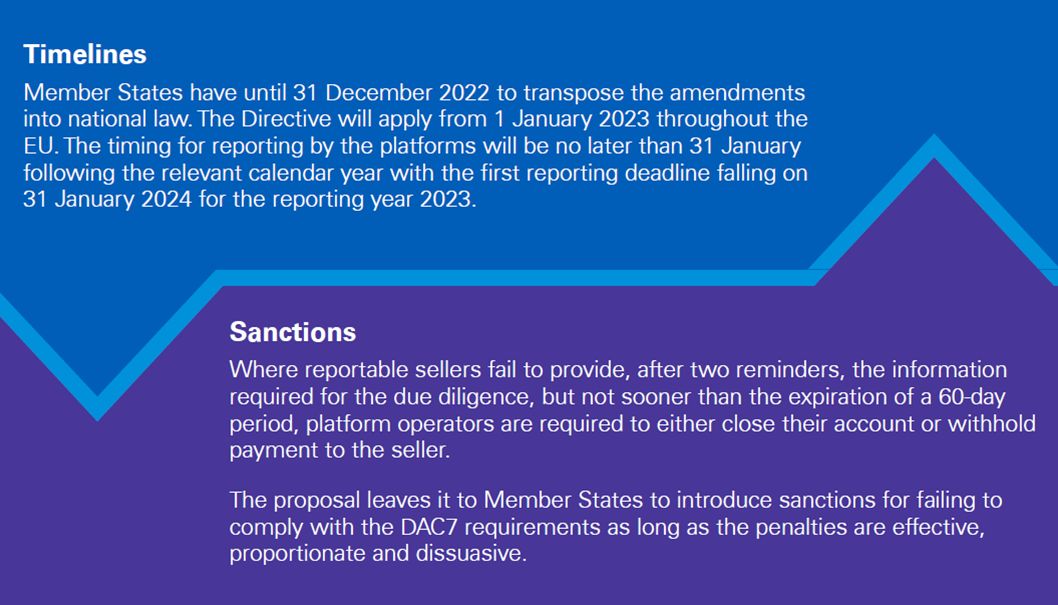

Also, platform operators are not required to report, amongst others, casual or one-time sellers of goods (with less than 30 sales not exceeding an annual consideration of EUR2,000) and rentals made by entities like hotel chains or tour operators that provide rentals at a high frequency (at least 2,000 rentals per year in respect of a Property Listing).

Exemptions from reporting also apply to non-EU platform operators from jurisdictions where adequate arrangements exist to ensure an exchange of information equivalent to the one under DAC7.

Reportable content

The reporting should cover both domestic and cross-border commercial activities.

Reportable information includes, inter alia;

- Identification details of the sellers (including the VAT and tax identification number);

- Residence of the sellers to be determined as per the Directive;

- An overview of amounts paid/payable to sellers from the reportable activities per quarter, platform fees, commissions or taxes withheld;

- The location of the rented immovable property when relevant.

Such information must be collected by the platform operators from sellers and verified in line with the due diligence procedures laid down in the Directive.

Reporting will be made with one tax authority in the jurisdiction with which the platform has nexus or, for non-EU platforms, in the jurisdiction of choice.

KPMG Commentary

Whereas certain platform operators have been already playing a role in the collection of taxes like VAT and in the provision of intelligence in some jurisdictions, DAC7 places an EU-wide obligation to share seller-level information relevant for tax compliance purposes without the platform being liable or having a role in collecting and remitting any tax. Yet, it comes at a time when the taxation of the digital economy is high on the international tax agenda.

DAC7 also follows the publication, in 2020, by the OECD of Model Rules for a global reporting framework for digital platforms with respect to sellers in the Sharing and Gig economy. While certain changes to the initial text of the DAC7 align it with the OECD regime, the scope of the activities reportable under DAC7 remains wider, for example with the inclusion of the sale of goods as a reportable activity. In this context, one would have to see whether further divergencies will be implemented both among EU and non-EU countries seeking to adopt platform reporting – the more unilateral or regional regimes that are adopted, the more complex it can get for platform operators to comply.

Although 2023 may sound far-off, platform operators should nonetheless start thinking about the possible DAC7 implications in terms of, but not exclusively:

- Assessing the extent and quality of current data in hand (possibly collated for onboarding, payment, VAT and other purposes);

- Examining the capacity, systems and processes necessary to be in place for further data collection, verification, management, testing, eventual transmission and possibly even analytics;

- Exploring the use of public interfaces for validating data and/or the possibility of outsourcing due diligence procedures;

- Reaching out to the often large number of sellers that trade through the platform and possibly educating them about their tax responsibilities;

- Reviewing the contractual relationships with the sellers;

- Evaluating any data protection implications;

- Complying with data retention rules; and

- Determining the place of registration for DAC7 purposes where this decision becomes relevant.

From the sellers’ side, although DAC7 does not affect their tax liabilities, it may mean increased scrutiny or audit activity by tax authorities on the basis of information received through platforms, potentially even in other areas such as social security payments of self-employed sellers.

From a Malta perspective, one expects DAC7 to be transposed through an amendment to the Cooperation with Other Jurisdictions on Tax Matters Regulations, S.L.123.127. It is early days to comment on the Revenue’s practical and interpretational approach towards DAC7, yet we will keep monitoring local developments to be of service to you.

Contact us

John Ellul Sullivan

Partner, Tax Services

KPMG in Malta

Lisa Zarb Mizzi

Partner, Tax Services

KPMG in Malta

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia