The Maltese Patent Box

The Maltese Patent Box

Malta has introduced patent box rules creating incentives for taxpayers involved in the development and use of intangible assets.

Following the issue of LN 208 of 2019 on 13th August 2019 Malta introduced patent box deduction rules, which allow taxpayers actively involved in the development and exploitation of IP to opt for the application of special rules on calculating deductions (“Patent Box Deduction”).

Benefits of Patent Box Rules

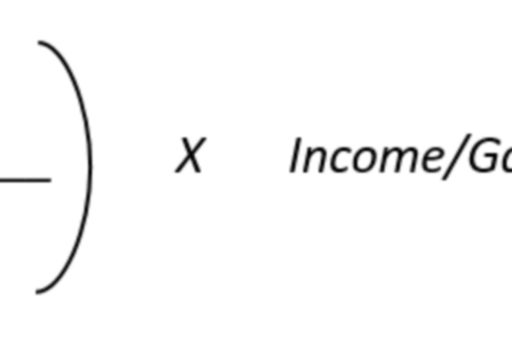

The Maltese Patent Box Deduction allows taxpayers that exploit qualifying IP to deduct their expenses related to such IP in terms of more favourable conditions than provided by the general deduction formula. The Patent Box Deduction is calculated based on the following formula:

Where:

- Total IP Expenditure includes all expenditure directly incurred in the acquisition, creation, development, improvement or protection of the qualifying IP; and

- Qualifying IP Expenditure is equivalent to Total IP Expenditures excluding certain types of expenses, particularly acquisition cost of IP and costs paid to related parties for the development of qualifying IP.

The above deduction may be applied against income/gains from qualifying IP derived on or after 1st January 2019.

Qualifying Intellectual Property

Only income/expenses from IP which meets definition of “qualifying IP” is eligible for the Patent Box Deduction. Qualifying IP includes the following categories of intangibles, provided that in any case the qualifying IP is granted legal protection in at least one jurisdiction:

- patents, including patents pending issuance/extension;

- non-patent IP protected by legislation (including those related to plant and genetic materials and plant/crop protection products);

- orphan drug designations, utility models and software protected by copyright;

- intellectual property assets that are non-obvious, useful, novel and that have features similar to those of patents. Only those holders who are regarded as “small entities” (i.e. entities with group turnover of up to EUR 50 million and gross IP revenue of up to EUR 7.5 million) are eligible to use such IP for the purpose of the Patent Box Deduction.

- it is important to note that marketing-related IP assets including brands, trademarks and tradenames are not considered as “qualifying IP”, and thus falls outside the scope of the new rules. Moreover, companies which are involved purely in holding and marketing IP without active development will have to setup R&D activities in order to be eligible to benefit from the new Patent Box Rules.

The Patent Box Deduction rules target taxpayers that are involved in the active exploitation of IP. The eligible beneficiary should satisfy the following conditions:

- be able to demonstrate that all important functions in relation to creation, development, improvement or protection of the qualifying IP are carried out by such beneficiary, solely or in cooperation under the terms of a cost sharing agreement, either directly or:

- through a permanent establishment situated in a jurisdiction other than that of the beneficiary (provided that income of such permanent establishment is subject to tax in the jurisdiction of residence of the beneficiary); or

- through other enterprises (and employees of other enterprises) provided that such functions are performed under the specific directions of the entity claiming the benefit.

- legally own “qualifying IP” or hold an exclusive license in respect of such IP. If the IP is developed under a cost sharing agreement, the entity must own a share in the ownership of the qualifying IP or be the holder of an exclusive license;

- the entity must be specifically empowered to receive income from qualifying IP; and

- have a sufficient level of substance in the jurisdictions where activities in respect of the qualifying IP are being carried out.

Key takeaway

The new Patent Box Deduction rules are based on the nexus approach as developed by the OECD, which requires a direct link between the benefits derived from favourable taxation and actual R&D activities. Only taxpayers engaged in the development of IP (either themselves or through independent subcontractors) may benefit from the Patent Box Deduction. The Patent Box Deduction rules exclude the application of the new deduction formula by taxpayers whose functions do not go beyond pure holding, deriving passive royalty income without contributing (directly or indirectly) to the development of the IP.

© 2024 KPMG, a Maltese civil partnership and a member firm of the KPMG global organisation of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. All rights reserved.

For more detail about the structure of the KPMG global organization please visit https://kpmg.com/governance.