Credit risk assesment - What the expectations of the Hungarian corporate sector?

Credit risk assesment - What the expectations of the...

What are the expectations of the Hungarian corporate sector?

The economic effects of the coronavirus and the stimulus measures designed to counteract it are forcing credit institutions to make a number of changes in measuring credit risk for both corporate and retail customers. Due to the payment moratorium, data on customers' solvency are limited until the end of the year, and credit institutions need to process loan applications of less than HUF 300 million from participants in the Central Bank’s Funding for Growth Program extremely quickly, in just 10 working days. However, the Central Bank's assessment of the impact of the coronavirus on the corporate sector may also help measuring credit risk in the altered circumstances.

In order to understand and monitor the economic situation due to the coronavirus, the MNB conducted a survey within the corporate sector between 26 March and 2 April, in which nearly 5,000 companies participated, 98% of which were SME’s. The questionnaire focused mainly on changes in demand and pricing, the slowdown in economic activity, as well as employment, the liquidity situation and investment plans, while wo-thirds of respondents were operating in the service sector. Half of the answers to the questionnaire came from the Central Hungary region, but significant feedback was also received from the rest of the country.

The main findings of the survey

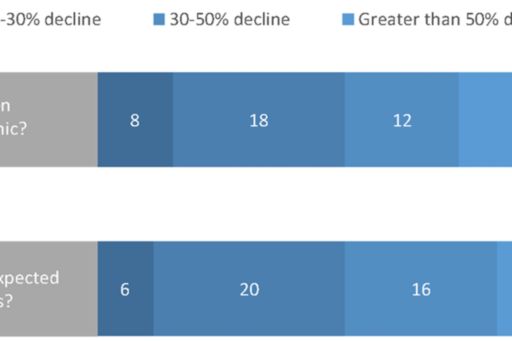

Based on the results of the survey, companies expect a significant drop in the net income in short-term, which they mostly do not plan to offset by price increases. Nearly half of the respondents experienced a decline in sales of over 30 percent and expect a further decline in the next 1-3 months. At the same time, according to research, companies trust a relatively rapid recovery, with 50% of respondents saying it will take less than 6 months to reach pre-crisis levels, while 25% say sales will return within a year.

A critical issue for business continuity is that 41% of respondents could not replace the 1-month outage of the supplier providing the material / service needed for production, and only 23% could solve the production / service differently. This is made even more severe by the fact that 63% of the respondents experienced supplier disruptions, mostly related to transportation difficulties from the countries most affected by the epidemic: a quarter of the disruptions came from countries with more than 100,000 cases and a quarter from countries with cases between 50,000 and 100,000.

The change in the number of employees can show the current situation of the given enterprise, but also the mid-term outlook of the management. 55% of the respondents do not plan to lay off workers in the short term, but 44% of the respondents see the pre-crisis number of employees as sustainable only for 2 months without improvements in the economic situation. It is an interesting finding that 40% of respondents would like to take out a loan to finance temporary wages, during which they would typically need to finance 3 months’ wage costs.

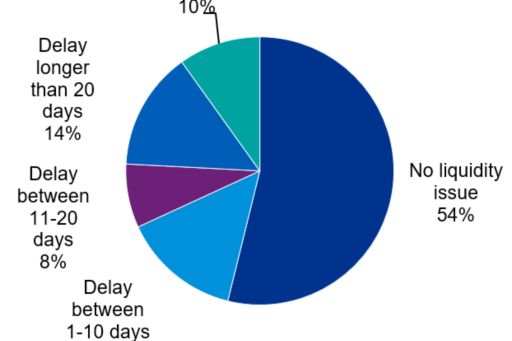

It may also be relevant for credit risk that a large proportion of respondents have not had a payment problem so far, but a third of respondents have been at least 11 days late on a payment. According to the research, the responding companies found paying public charges/taxes and wages the biggest difficulties and the supplier accounts come only in the third place. Especially in the most affected sectors, it is important to note that only about 40% of companies can maintain their solvency for more than a month without income.

Due to the epidemic, nearly one-third of respondents are forced to postpone their planned investments, but despite the crisis, nearly 20% of respondents would take out investment loans, half of them for the full amount planned before the crisis. The companies participating in the research primarily consider favourable interest rates and, secondly, fast administration, to be the most important factors in the current situation, which shows changing customer needs and accelerating expectations.

Sector specificities

The Covid-19 crisis affected various sectors differently. In some areas, operations have come to a complete halt, some players have limited operations, and there are companies where the production / service process continues uninterrupted. The production / service process has to be stopped for at least 1 month by almost all enterprises engaged in entertainment, leisure activities, accommodation services, and a significant part of catering establishments also stop for more than 1 month, however, so do 41% of manufacturing companies also have to halt for a month. The analysis of downtime is also critical from a credit risk perspective, because firms make virtually no revenue during this period, but fixed costs remain relevant.

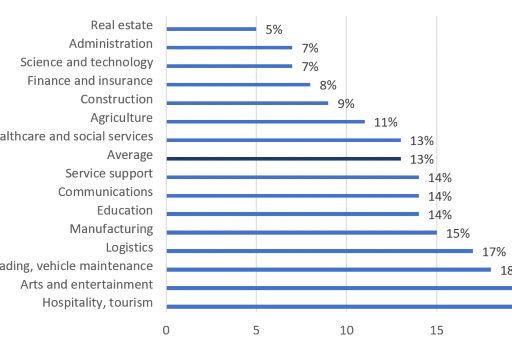

These results are also well illustrated by the fact that there is a significant difference in solvency by sector, while only 9% of respondents in the construction industry had a payment delay of more than 20 days, while 20% operating in trade and 23% operating in catering and accommodation services were delaying a payment over 20 days.

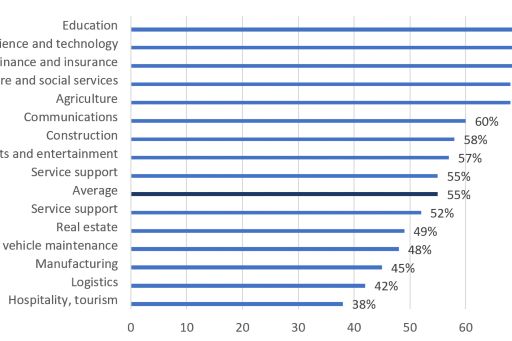

There are also significant differences between companies in terms of companies’ expectations about the employment situation. According to the research, for example, 53% of the enterprises operating in the catering industry, 25% of those operating in the manufacturing industry, but only 14% of those operating in the agricultural sector will not be able to meet their wage payment obligations. As a result, the difference is also significant in terms of the planned number of employees, while 71% and 68% of companies engaged in financial insurance or agriculture respectively plan to maintain their current number of employees, 45% in manufacturing and only 38% in hospitality plan to do so.

The Central Bank's research examined a wide range of issues, which shows a significant difference between sectors. An important aspect in the analysis of credit risk, especially due to the limited payment data available due to the payment moratorium, is the examination the effects of the Covid-19 crisis in the national economy and the expected economic situation of the given company/sector. Of course, in addition to assessing the risk to businesses, it is also very important for individual customers to analyse their workplace, but at least the relevant sector. Altogether it is an important task for credit institutions to pay special attention not only to past data, but also to the debtor's future prospects, including the assessment of the labour market sector, when developing credit rating, scoring models.

The current extreme uncertainty makes it more difficult to effectively assess credit risk and monitor loans with previously used methodologies, but maintaining a lending activity with the help of a well-thought-out, thorough analysis of risks is key is crucial from perspectives of both the individual business and the national economy.

© 2024 KPMG Hungária Kft./ KPMG Tanácsadó Kft. / KPMG Legal Tóásó Ügyvédi Iroda / KPMG Global Services Hungary Kft., a magyar jog alapján bejegyzett korlátolt felelősségű társaság, és egyben a KPMG International Limited („KPMG International”) angol „private company limited by guarantee” társasághoz kapcsolódó független tagtársaságokból álló KPMG globális szervezet tagtársasága. Minden jog fenntartva.

A KPMG globális szervezeti struktúrával kapcsolatos további részletekért kérjük látogassa meg a https://kpmg.com/governance oldalt.