The Corporate Sustainability Reporting Directive (CSRD) adopted by the EU Parliament in November 2022 profoundly changes the scope and nature of corporate sustainability reporting.

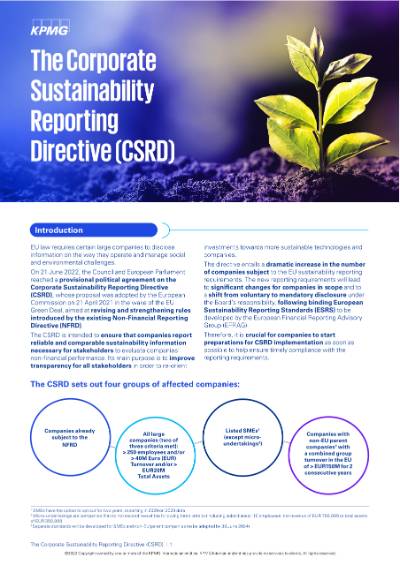

The CSRD significantly expands existing rules on non-financial reporting. All companies listed on an EU-regulated market (with the exception of micro-enterprises) are covered by the new reporting obligation. In addition, all non-capital market oriented companies are covered by the CSRD if they fulfil two of the following three criteria (EU thresholds, subject to transposition into national law):

- Balance sheet total > 25 million euros

- Net sales > 50 million euros

- Number of employees > 250

It is estimated that this would affect about 50,000 companies in the EU, 15,000 of them in Germany alone.

The new CSR Directive follows a double materiality perspective. This means that companies must record the effect of sustainability aspects on the economic situation of the company. And they must clarify the impact of operations on sustainability aspects. The CSRD requires reporting to include information on:

- Sustainability goals,

- the role of the executive board and the supervisory board

- the company's most significant adverse impacts, and

- intangible resources not yet accounted for.

In addition, with the new CSRD there is no longer the possibility to publish non-financial information in a separate non-financial report. In future, sustainability information is to be disclosed exclusively in the management report.

Goran Mazar

Partner, EMA & German Head of ESG and Automotive

KPMG AG Wirtschaftsprüfungsgesellschaft

Learn more in our brochure (in German only)

Sustainability reporting: We help you with implementation

Our experts support you across all levels of ESG reporting to make the transition to sustainability as smooth and beneficial as possible. We help you to embed the requirements of the Corporate Sustainability Reporting Directive (CSRD) in your organisation while taking advantage of ESG-related opportunities.

Our modular project approach can be tailored to your individual needs. Our experts have extensive experience in sustainability consulting and the auditing of sustainability reports. We develop pragmatic and helpful solutions and services to help you cope with the extensive requirements of sustainability reporting.

In our brochure "Get ready for the next wave of ESG reporting" you can find out in detail how KPMG can support you in the transition to CSRD-compliant sustainability reporting.