Transforming the tax function through technology Transforming the tax function through tech

Introduction —before we begin

An Australian journalist described the world as being “in amoment between technology and techno-panic”. This is the idea that we are both excited about and fearful of what the future may hold for us in a world where technological developments are on the precipice of a revolution, one that is increasingly being referred to as the fourth industrial revolution. The onset of this revolution has left many tax and finance managers feeling anxious about being left behind and uncertain of where to start. Indeed, the term ‘disruption’, which is so commonly bandied about to describe the effect of this revolution, evokes images more associated with fear than with education and opportunity. The goal for this publication is to provide tax and finance leaders with a foundation for transforming their departments and increased confidence in embracing technology and the benefits it can bring for managing and evolving the modern tax function.

This publication is founded on a core belief that to transform an in-house tax function with technology, tax departments need to ‘walk before they run’. To transform an organization that is rooted in traditionally manual tasks into a highly technologically enabled tax function requires a journey over a period of time. It is not a process that happens without thoughtful planning, nor can it happen overnight simply by investing in the latest technology solutions in the market. It is vital to remember that the use of technology in a tax function needs to serve a purpose beyond merely the use of trendy new gadgets or following the lead of others. Rather, meaningful technology-enablement is about making strategic changes that benefit the function and the organization in terms of time and cost savings, efficiency gains, and helping to move the tax function up the value chain within the organization, so that the tax department becomes a true enabler of value inside the organization and beyond.

It is important to recognize that technology is but one, albeit integral, component to tax function transformation. As the below diagram highlights,2 the operating model of a tax function comprises six key components, with the seventh component, performance management, as a measurement and performance tool to monitor the value contributed to the organization. Technology and the related components of data and information that feed into technology solutions are increasingly important as we move into the third decade of the 21st century. However, technology also needs people with skills to operate and maintain it, an organizational model to support it, and it needs to enable or facilitate processes, governance and risk. In short, technology may be at the epicenter of any transformation strategy, but it must work in unison with the other components in order to be truly effective.

It is vital to remember that the use of technology in a tax function needs to serve a purpose beyond merely the use of trendy new gadgets or following the lead of others.

Themes — Helping to understand the problem

Of course, every organization is different and the problems you may be trying to solve through technology will have elements that are specific to your organization. However, there are many recurring themes that KPMG professionals hear when speaking with tax leaders around the world. Consider the following examples:

- “The people on our team spend a lot of time doing manually oriented tasks to support our tax compliance process — how do we reduce that?”

- “Our organization has trouble obtaining the data we need to prepare our tax filings; the data often comes in from many different sources. Is there a better way?”

- “We need to spend a lot of time each month checking, adjusting and/or reconciling data to ensure the accuracy of our tax returns. Even then, we are often concerned it may not be correct.”

- “As a tax leader, I struggle to have visibility over the activities or transactions being carried out by the business, or in knowing how tax can best support our business goals. Is there a way to help me with this?“

- “I’ve heard the tax authorities in my jurisdiction are investing heavily in technology so that they can carry out data and analytics testing. I don’t know what they may find with my organization.”

- “Our department seems to spend much of its time trying to get the information from the business, in managing tax problems for transactions that have already happened; how do we get the time to be able to prevent problems from arising in the first place?”

- “The budget in my organization will not be sufficient to allow me to hire new people, or to invest in technology to help me fix some of our existing problems.”

These themes highlight the problems most organizations encounter, and suggest why many turn to technology solutions to help address inefficiencies in current systems and/or processes, to ensure greater accuracy or insights, or to mitigate potential risks. Knowing the problem you are trying to solve by technology is a critical first step in the journey. To use an analogy, if a person wants to avoid unnecessary spending, they may prefer to write a shopping list before entering the store. The same is true with technology. Knowing what your problem is before you embark on your journey helps you map the right path to get there.

A critical framework

To help you start with your journey of discovery, let us share what we see as a critical framework for achieving a technology enabled tax function.

Technology helps

Most tax technology solutions in the market today can be broadly placed into one of four categories:

- compliance

- insights

- process management

- accessories, components or infrastructure, which enable or facilitate 1, 2 or 3.

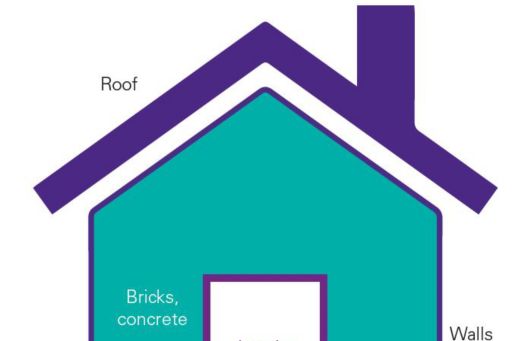

Let’s look at each of these in turn. First, however, let‘s use the analogy of a house to explore each of these areas, and the role they play in building a technology enabled tax function.

Compliance related solutions

Compliance related solutions refer to those solutions that help you to prepare and/or file tax returns more efficiently and accurately and/or in a more automated way. They may also help you perform similar automation functions for invoicing purposes. These solutions can help either with specific taxes or with the full range of tax returns from VAT filings (including invoicing), to corporate income tax filings, even to stamp duty. Most tax professionals would readily accept that efficient and accurate management of compliance activities is at the core of their responsibilities; thus, compliance solutions are among the most common seen in use by tax departments today.4 To return to the house analogy, we might think of the compliance related solutions as the walls and roof of a house; they are both integral and critical to the overall structure. Most tax professionals would readily accept that to get their compliance handled both efficiently and accurately is at the core of their responsibilities.

Insight related solutions

Insight related solutions refers to the broad category of technology solutions that give you greater insights into the accuracy of your tax related data, helping you to identify potential tax risks up front and/or enabling you to identify errors or inconsistencies in your tax filings. Examples may include software solutions that allow you to carry out sophisticated data analytics to identify potential errors in your tax reporting, analyze the margins on transactions for transfer pricing purposes, identify permanent establishment risks or help calculate tax liabilities of expatriates employed by your organization around the world. In terms of the house analogy, insight related solutions may be viewed like the interior design of a house. The interior features make the house more visually appealing, and also more functional.

Process management solutions

Process management solutions are those that help to manage either a specific process or an end-to-end process, by making the right information available to the right person at the right time. More specifically, these solutions may help to manage workflow within your tax function, or possibly within your organization. They are not solutions that ‘do’ anything in the sense that they are focused more on facilitating and optimizing the process, rather than changing the outputs of the process. As such, they may not provide insights into your tax data, and they may not prepare the tax returns you need. Rather, they help to manage these processes by helping your organization operate more efficiently. Examples include workflow solutions, which help to track the tax return preparation and approvals processes, and solutions that store your tax working papers in one place so that they are accessible to your tax team. When we think of these solutions in terms of building a house, we might consider these types of solutions the concrete that holds the bricks together.

Accessories, components or infrastructure

When we speak of accessories, components or infrastructure, we are referring to those hardware or software solutions that are typically built into your tax technology software, or that enable or facilitate the automation of compliance or the delivery of insight related solutions. Examples include solutions that manage the data extraction process, help to deliver visualizations of your data, or those that allow you to store data, such as cloud computing or data warehouses. Accessories, components or infrastructure may not be the most exciting aspects of tax technology, but they will often be the building blocks that can make the difference betwee a successful deployment and one that may not succeed. We might think of these as the foundations of the house. A house needs to be built on a solid foundation, with well-constructed walls, held together with concrete and designed in a way that is both aesthetically pleasing and functional.

A tax technology strategy needs to combine all of these elements in harmony. Investment in one component to the exclusion of another may not achieve the intended results. However, you may not be able to invest in every area at once.

Most change will be incremental

For most organizations, the incorporation of technology solutions into your tax function will be achieved incrementally, not radically. Rather than try to lead the way in rapid technology investment, most tax functions will strive to invest gradually, focusing on becoming more efficient and cost effective, and seeking to deliver more value to their organizations, each year surpassing the last.

Again, while the early adopters may be striving more ambitiously and experimenting and investing in research and development early on, for most organizations, change will be achieved through a series of steps.

Consider that when electronic payments were first launched through the internet, consumers often expressed concern about the security of their data. While those concerns may still be evident to some extent, advances in digital security have reduced those concerns, and most consumers engage now in electronic payments on a regular basis. In other words, what may have seemed risky or difficult 2 to 3 years ago is now a routine task.

The challenge for the tax function will be to do things each day or each month slightly differently from the day or month before. Over time, your department and your organization will adapt. Change does not happen automatically, nor does it happen without facing some challenges along the way.

Technology goals need to be realistic

It is critically important to be realistic about what will be achieved in the early days with tax technology. Sometimes, tax leaders associate automation of the tax compliance process with the idea that, each month, they will be able to press a single button on a computer and produce a perfect tax return, fully correct and complete. Unfortunately, that is the work of science fiction. Moreover, if it were true, then the role of the tax manager would likely become redundant very quickly. But there are many benefits to be gained already through early incarnations of automation, long before total automation is a reality.

Why do we say that total tax automation is more aspirational than real, at least in the period leading up to 2020?

While we may all wish for perfection in tax automation, it’s important to recognize why limitations exist. For example, perfection in tax automation would require an organization to have perfect data in its ERP system, and for that data to be collected and stored in a way that is deliberately set up for the tax function; it would require the data to be complete, with no manual reconciliations or adjustments needed. This is simply unrealistic right now in most organizations, especially multinational entities operating across multiple jurisdictions. The reality is more like the following:

- Many organizations maintain data in multiple systems — this will often require some form of reconciliation because those systems may not always ‘speak’ to each other.

- The data that is maintained in ERP systems often contains errors or anomalies or is incomplete, because in many cases much of the data is still entered manually. In the future, this may change with advances in optical character recognition (OCR) technology, but this is still a few years away for most organizations.

- Most ERP systems are not built with the tax function in mind, so we cannot expect the reporting data to be perfectly suited for the tax function’s needs.

- Compliance with tax legislation in many jurisdictions requires adjustments to be made that fall outside transactions that are recorded in an ERP system. A great example of this is deemed sales transactions whereby output VAT may be payable for goods or services which are given away for no sales revenue (essentially ‘free’). Similarly, an organization may make some exempt sales for VAT purposes, or incur nondeductible entertainment expenses, and frequently these adjustments happen through manual intervention. There are many circumstances requiring changes to happen ‘outside of the system’, and these require real people to manage the effort.

There is an increasingly important field of expertise emerging around data integrity, especially for the tax function. This is the idea that while we may strive to use Big Data, ultimately its utility very much depends upon having trust in the data being used in preparing the tax returns — that is, that the data is accurate, correct and complete. It is the adage that any investment in technology is limited by the fact that the outputs of data will only be as good as the input. Or, as the saying goes, “garbage in will equal garbage out.”

In our experience, one possible outcome when first starting to invest in tax technology is to discover that the solution being deployed does not work effectively because the underlying data lacks integrity. This may result in the immediate project being diverted to fix the problems with data integrity — for example, by including additional data points recorded through an ERP system to allow better testing and analysis, or by correcting errors in the data — referred to as ‘data cleansing’. While this may seem frustrating at the time, it is important to recognize that this can happen, but that the end result of this temporary diversion in resources is a longer lasting and higher quality series of outcomes. In other words, recognize that you may need to take one short-term step backwards in order to take two longer-term steps forward.

As a concrete example of this, KPMG China tax professionals recently carried out an analysis of a client’s ERP data. One of the client’s objectives was to identify and reconcile the receipt of special VAT invoices as recorded in the Golden Tax System, which is China‘s system for taxpayers to record all transactional tax data, with potentially available input VAT credits reflected in their ERP system. However, while the team was able to carry out the reconciliation process with reasonable accuracy, through this process they identified a simple change needed in the client’s data entry into their ERP system, which would enable near real-time reconciliations to occur. The primary outcome was a simple process change that would better align the client’s data needs for the future, with consequential efficiency benefits.

The moral of this story is that the adoption of technology as part of a tax function transformation process may not necessarily yield the immediate results you expect, nor should you expect it to automate your tax function fully at the outset. There will be learnings along the way, and the journey you are embarking upon should be seen as a permanent feature in your organization, not as a ‘set and forget’ short-term project.

1 ‘How to ensure Australia thrives when the robots come,’ Peter Hartcher, Sydney Morning Herald, 30 September 2017, smh.com.au/comment/how-to-ensure-australiathrives-when-the-robots-come-20170929-gyrgr9.html

2 ‘Designing an Indirect Tax Function which is Fit for the Future,’ KPMG International, 26 September 2016, https://home.kpmg.com/xx/en/home/insights/2016/09/designing-an-indirect-tax-function-that-is-fit-for-the-future.html

3 KPMG International’s 2017 Global Tax Department Benchmarking Study Data

4 KPMG International’s 2017/2018 Global Tax Department Benchmarking Study Data