| Area |

Key disclosure and presentation considerations |

Reference |

| Basis of preparation |

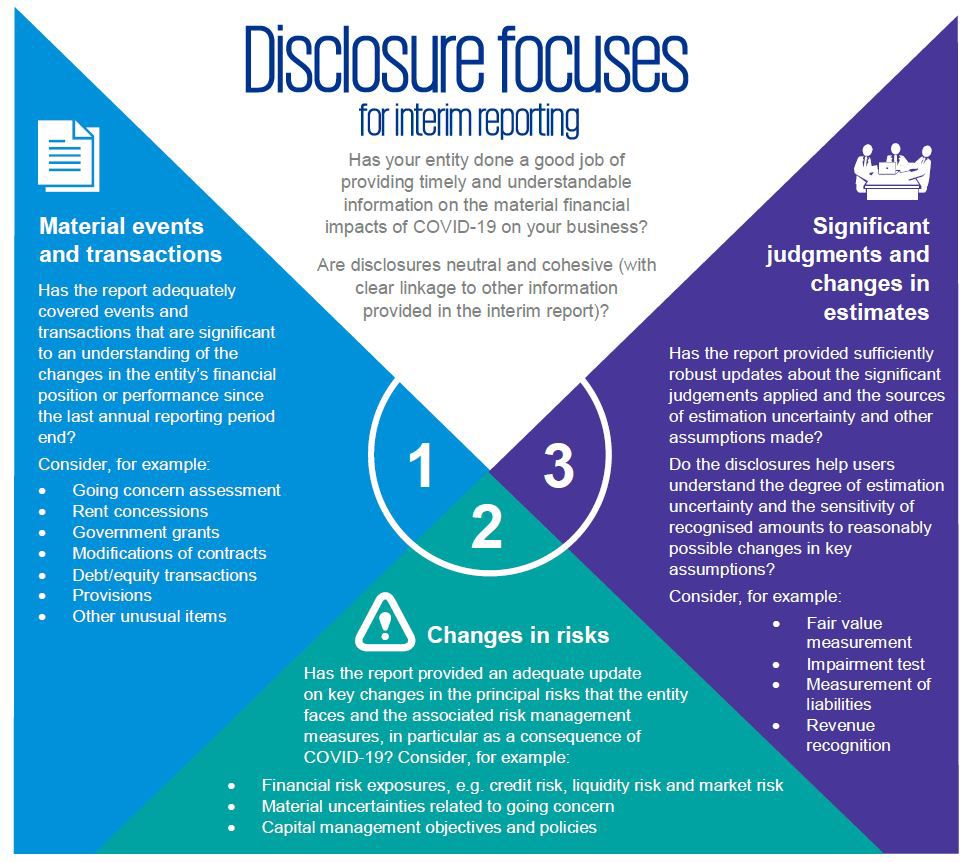

Material events and transactions

- Narrative descriptions of the appropriateness of the going concern assumption after taking into account the uncertainties about the impact of COVID-19, the extent and duration of various government health measures, and the impact on the economy and fluctuating asset prices during the interim period, as well as the entity’s current and expected profitability, debt repayment schedules and potential sources of replacement financing.

Changes in risks

- Disclosure of the material uncertainty relating to going concern that are as specific to the entity as possible, so as to enable the users of financial statements to understand how and when the uncertainty might crystallize and its impact on the resources, operational capacity, liquidity and solvency of the entity.

Significant judgments and changes in estimates

- The significant judgement involved in the management’s conclusion that there is not a material uncertainty relating to the entity’s ability to continue as a going concern.

|

I/HKAS 34.15; I/HKAS 1.4, 25-26, 122 |

| Financial instruments |

Material events and transactions

- Recognition of a loss from the impairment of financial assets and the reversal of such an impairment loss.

- Loan default or breach of a loan agreement that has not been remedied on or before the end of the reporting period and any resulting change in the presentation as current or non-current liabilities in the statement of financial position.

- Issues, repurchases and repayments of debt and equity securities.

- Nature and amount of items affecting financial instruments that are unusual because of their nature, size or incidence, e.g. modifications of existing contractual arrangements, sale of financial assets measured at amortised cost that are managed in a held-to-collect business model.

Changes in risks ✥ Expanded disclosures of qualitative and quantitative information about liquidity risk arising from financial instruments, with added focus on the entity’s response to the impact of COVID-19. For example:

- an explanation of how an entity is adjusting the way they manage liquidity risk to respond to the current difficult economic conditions, including the use of alternative sources of funding and availability of the banking facilities (whether they are committed or not);

- what are the entity’s liabilities and what are the cash and investments available to meet those obligations;

- any material adverse clauses in the entity’s borrowings and facilities available – e.g. those linked to changes in credit-worthiness or other financial metrics;

- any defaults and breaches relating to the borrowings recognised during and at the end of the reporting period; and

- impact of COVID-19 on factoring and reverse factoring arrangements, where relevant.

✥ Information about an entity’s credit risk management practices and how they have been changed in response to COVID-19 and how COVID-19 impacts on the recognition and measurement of expected credit losses (ECLs) – e.g. by extending payment terms for trade receivables or revisiting the debt collection processes. Significant judgments and changes in estimates ✥ Nature and amount of changes in estimates, e.g. changes in estimation techniques, assumptions and information used to measure ECLs – in particular, how it has:

- dealt with the challenge of measuring ECLs using a provision matrix that relies heavily on historical information which may not fully reflect the impact of the current economic shocks;

- updated customer segmentation so that trade receivables are grouped based on shared credit risk characteristics for the purpose of measuring ECLs;

- calculated any overlays and adjustments to the ECL model;

- reflected the impact of any credit insurances;

- incorporated the provision of government support that might aid recovery of balances; and

- incorporated the forward-looking information into measuring ECLs.

|

I/HKAS 34.15, 15B(b) & (i), 15C,16A(c) & (e), I/HKFRS 7.20(a)(vi) & I/HKAS 1.69 I/HKAS 34.15 & 15C, I/HKFRS 7.18-19, 33-34, 35B and 39(c)

I/HKAS 34.15C, 16A(d), I/HKFRS 7.31, 35F-G, I/HKAS 1.122 & 125

|

| Hedge accounting |

Changes in risks

- Information about an entity’s hedge accounting application, in particular how it is applied to manage each category of risk according to the risk management strategy and how the hedging activities may affect the amount, timing and uncertainty of its future cash flows and its financial effect.

- Other sources of hedge ineffectiveness emerging in a hedging relationship by risk category and explanations for the resulting hedge ineffectiveness.

- Forecast transactions that were subject to hedge accounting but are no longer expected to occur and the related reclassifications from the cash flow hedge reserve to profit or loss.

- Reclassifications of irrecoverable losses from the cash flow hedge reserve to profit or loss.

|

I/HKAS 34.15C I/HKFRS 7.21A, 22A, 23E-F, and 24C(b) |

| Fair value measurement for each class of financial assets and financial liabilities |

Material events and transactions

- Changes in the business or economic circumstances that affect the fair value of the entity’s financial assets and financial liabilities, whether those assets or liabilities are recognized at fair value or amortised cost.

- The amounts of any transfers between Level 1 and Level 2 and of any transfers into or out of Level 3 of the fair value hierarchy for recurring fair value measurements (in particular, the number of fair value measurements classified as Level 3 may have increased).

- The reasons for any transfers between levels of the fair value hierarchy, as well as the entity’s policy for determining when transfers between levels are deemed to have occurred (e.g. occurred at the date of the event or change in circumstances that caused the transfer, deemed to have occurred at the beginning of the reporting period, or at the end of the reporting period).

- The existence of an inseparable third-party credit enhancement issued with a liability measured at fair value and whether it is reflected in the fair value measurement.

Significant judgments and changes in estimates

- A narrative description of the sensitivity for recurring Level 3 fair value measurements in response to changes in unobservable inputs (such as certain risk-adjusted discount rates).

- Quantitative sensitivity information if changing one or more of the unobservable inputs to reflect reasonably possible alternative assumptions would change fair value significantly, together with disclosure of the key assumptions and judgements made by management.

- The impact of increased economic uncertainty on forecasts, the assumptions the entity has made about the future, other unobservable inputs and the valuation techniques used in the recurring Level 2 and Level 3 fair value measurements, in particular when a valuation report contained a significant valuation uncertainty clause. If there is a change in the valuation technique, the change and the reason for making it shall also be disclosed.

|

I/HKAS 34.15B(h) & (k); I/HKFRS 13.93(c) & (e)(iv), 95 and 98

I/HKAS 34.16A(j) I/HKFRS 13.93(h) & (d), I/HKAS 1.125

|

| Fair value measurement of non-financial assets and non-financial liabilities |

Significant judgments and changes in estimates

- Nature and amount of changes in estimates, e.g. changes in estimation techniques, assumptions, key inputs and information used to measure non-financial assets and liabilities carried at fair value, e.g. investment property and cash-settled share-based payment transactions.

|

I/HKAS 34.15C & 16A(c), I/HKAS 1.125 |

| Other non-financial assets, including goodwill |

Material events and transactions

- Any material impairment loss recognised on property, plant and equipment, intangible assets, assets arising from contracts with customers, or other assets, and the reversal of such an impairment loss (except for goodwill), including an explanation of significant events during interim period which led to the loss or reversal and/or an update to any related information included in the last annual financial statements.

Significant judgments and changes in estimates

- Changes in estimates and judgement used in the impairment test – e.g. information about any ‘out-of-cycle’ impairment tests or changes in approach (e.g. change from a single cash flow projection approach to a multiple, probability-weighted, cash flow approach) and inputs used in estimating recoverable amounts.

- Sensitivity of estimates to reasonably possible changes to key assumptions when testing a cash-generating unit containing goodwill (or intangible assets with indefinite useful lives) for impairment.

- The impact of the increased economic uncertainty on forecasting cash flows, the assumptions the entity has made about the future, the inputs or metrics used for the purpose of determining fair value less costs of disposal in impairment testing, in particular when a valuation report contained a significant valuation uncertainty clause.

- Changes in estimates for determining the residual value and the useful life of the tangible and intangible assets as at interim reporting date when the usage or retention strategy for these assets has changed.

|

I/HKAS 34.15B(b) & 15C

I/HKAS 34.15C & 16A(d) I/HKAS 16.51& I/HKAS 38.104, I/HKAS 36.134(e)-(f), I/HKAS 1.122 & 125

|

| Inventory and contract costs |

Material events and transactions

- The amounts of write-down of inventories to net realizable value and the reversal of such a write-down, including the significant events and transactions occurred during interim period causing such results.

Significant judgments and changes in estimates

- Changes in estimates for the amortisation period for contract costs relating to contracts with customers.

|

I/HKAS 34.15B (a),15C & 16A(d), I/HKAS 1.125 |

| Revenue |

Significant judgments and changes in estimates

- The judgement involved in applying the principles of revenue recognition, e.g. the enforceability of contract terms (in particular how COVID-19 is considered in the legal interpretation of clauses, such as “force majeure” or similar clauses), collectability issue for new contracts.

- The nature and amount of changes in estimates of amounts reported in prior financial year, e.g. changes in the timeframe for a performance obligation to be satisfied and any adjustments to the variable consideration.

|

I/HKAS 34.15C & 16A(c)-(d), I/HKAS 1.122 &125, I/HKFRS 15.123-126 |

| Government grants and other assistance |

Material events and transactions

- Nature, extent and amount of government grants recognised in the interim financial report and an indication of other forms of government assistance from which the entity has directly benefited, e.g. various relief measures introduced to support borrowers affected by COVID-19, which could be in the form of payment holidays on existing loans.

- Unfulfilled conditions and other contingencies attaching to government assistance that has been recognised, e.g. the conditions attached to the wage subsidies granted to the employers.

|

I/HKAS 34.15C, 16A(c) & I/HKAS 20.39(b)-(c) |

| Leases |

Material events and transactions

- The fact that the entity as a lessee has applied the practical expedient in the recent IFRS 16 amendment (and the equivalent HKFRS 16 amendment) to all qualifying COVID-19-related rent concessions or, if not applied to all such rent concessions, information about the nature of the contracts with similar characteristics and in similar circumstances to which it has applied the practical expedient.

- The amount recognised in profit or loss for the reporting period to reflect changes in lease payments that arise from rent concessions to which the practical expedient has been applied.

- Nature of rent concessions (e.g. one-off rent reductions, rent waivers or deferrals of lease payments) received during the period, regardless of whether the company applies the practical expedient relating to COVID-19.

|

I/HKAS 34.15C, 16A(c) & I/HKFRS 16.59, 60A |

| Provisions and obligations |

Material events and transactions

- The nature and the amount of the provision recognised in the financial statements and the expected timing of any resulting outflows of economic benefits, e.g. restructuring provisions, provision for employees’ termination benefits.

Significant judgments and changes in estimates

- An indication of the uncertainties about the amount or timing of those outflows and, where necessary, the major assumptions made concerning the future events that may affect the amount required to settle an obligation.

|

I/HKAS 34.15C, 16A(c) & I/HKAS 37.85, I/HKAS 1.125 |

| Non-current assets held for sale |

Material events and transactions

- The description of any non-current assets (or disposal group) which satisfied the held-for-sale criteria during the period and hence are presented as current in the statement of financial position.

- The facts and circumstances of the sale or the expected sale, and the expected manner and timing of that disposal.

- Recognition of an impairment loss for any write-down of the non-current assets (or disposal group) to fair value less costs to sell.

- The reportable segment in which the non-current asset (or disposal group) is presented.

|

I/HKAS 34.15C, 16A(c) & I/HKFRS 5.20 & 41 |

| Capital management objectives and policies |

Changes in risks

- Changes in an entity’s objectives, policies and processes for managing capital in response to COVID-19 – e.g. whether the entity has become subject to externally imposed capital requirements, the nature of those requirements and how those requirements have been incorporated into the management of capital.

- Summary quantitative data about the changes in managing capital, e.g. any change in the components within the capital structure.

|

I/HKAS 34.15C, I/HKAS 1.134-135 |

| Non-adjusting subsequent events |

Material events and transactions

- The nature of the event and an estimate of its financial effect, or a statement that such an estimate cannot be made.

- Information relating to the non-current assets (or disposal group) which satisfy held-for-sale criteria after the reporting period but before the authorization of the interim financial report for issue.

|

I/HKAS 34.15C & 16A(h), I/HKAS 10.21-22, I/HKFRS 5.12 |