On 27 March 2020, the Hong Kong Inland Revenue Department (“IRD”) published a revised version of Departmental Interpretation and Practice Notes No. 39 – Profits Tax Digital Economy, Electronic Commerce and Digital Assets (“Revised DIPN 39”) addressing various key issues concerning taxation of e-commerce transactions and digital assets.

This is an evolving area of tax law and as the government seeks to encourage the digital economy, it will be important for taxpayers in the sector to understand the basis on which they will be taxed. While the decorrelation of physical presence and ability to transact has created challenges for governments across the globe, it arguably poses particular challenges in a source-based jurisdiction, where the proximate cause of profits may be a long way from the central hub of operations. The revised DIPN provides practical guidance on the IRD’s views, but is of necessity a temporary measure pending the conclusion of global discussion on BEPS 2.0.

Overview

The Revised DIPN 39 contains material changes in relation to the previous version of July 2001. The key highlights from the Revised DIPN 39 are summarized below:

- The IRD has set out what it considers to be the key value creators of an e-commerce business, having confirmed the view that data generated and gathered in the course of an e-commerce transaction (e.g. customers’ personal data) as well as direct and indirect network effects should be understood as key value creators for e-commerce businesses.

- The IRD has also confirmed that, in the absence of any specific provisions in the Inland Revenue Ordinance (“IRO”) that deal with the taxation of e-commerce, the tax consequences of e-commerce transactions are to be determined in accordance with Section 14 of the IRO.

- In addition, the IRD has provided some practical guidance on how to determine the locality of profits in the context of e-commerce transactions. The IRD appears to take the view that the proper approach is to focus on the core operations that have effected the e-commerce transaction to earn the profits in question and the place where those operations have been carried out, rather than on what has been done electronically (i.e. location of core operations as a test of source).

- Regarding the question of whether a non-Hong Kong resident person has a PE in Hong Kong, the IRD takes the view that, in the context of e-commerce, the decisive criterion may be whether the activities of a fixed place of business (which could be a computer system or server) form an essential and significant part of the e-commerce business as a whole or whether those go beyond preparatory or auxiliary activities.

- The IRD has reiterated in this DIPN that the Authorised OECD Approach will be adopted in attributing profit from non-resident to its HK PE, where applicable. This requires a two-step analysis, namely: 1) considering the HK PE as a functionally separate entity and attributing assets and risks to the PE; and (2) applying the arm’s length principle to the transaction of the hypothetical entity (i.e. the PE).

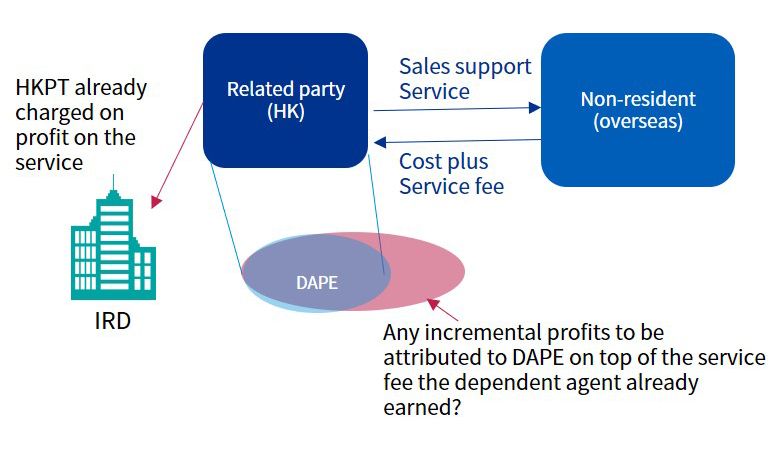

- In the case where a non-resident is considered as having a dependent agent PE (“DAPE”) in HK, an issue arises as to whether additional profits should be attributed to the DAPE assuming that the dependent agent had already earned an arm’s length service fee from the non-resident and is taxed accordingly in HK. The issue is illustrated in the below diagram as an example.

- The non-resident is engaged in e-commerce business that sells goods through an online platform directly to customers in various markets including Hong Kong.

- The non-resident engaged a related party in HK for provision of local sales support, including: merchandising of products, collection of information from its customers in HK, handling the receipt of shipments from suppliers, stocking of the goods and execution of deliveries to customers in HK.

- The non-resident creates a DAPE in HK if the related party habitually plays a principal role leading to the conclusion of contracts without material modification by the non-resident.

- The IRD has also provided some relevant comments regarding the taxation of digital assets, namely in respect of digital tokens. The IRD holds that subject to any specific exemptions provided, profits arising in or derived from Hong Kong from an Initial Coin Offering (ICO) can be charged to profits tax in accordance with the general principles in Section 14 of the IRO. Whereas, profits arising from the sale of digital assets bought for long-term investment purposes, would not be chargeable to profits tax (i.e. profits from sale of capital assets). Furthermore, the IRD confirmed that in determining if digital assets are capital assets or trading stock reference must be made to the intention at the time of its acquisition.

- It is worth mentioning as well that the previous DIPN 39 contained a statement that the taxation of e-commerce should follow a principle of neutrality and that the ordinance should be applied to e-commerce on a basis consistent with conventional business. This statement has been removed from the Revised DIPN 39.

KPMG Observation

Globalisation and digitalisation have enabled the rise of new business models, in which multinational enterprises can create value and generate profits in countries where they are not physically present. But while these developments have changed how and where profits are made, international tax rules have yet to adapt accordingly.

An update to DIPN 39 by the IRD is an undoubtedly welcome move in view of the seismic changes that have occurred in the field of electronic commerce and considering recent global developments in the context of the tax challenges arising from digitalisation of the economy. However, while it is useful in giving taxpayers some practical insights into the IRD’s approach, it perhaps struggles to reconcile a source-based approach to taxation with the realities of digital business. In our view it is far from clear that the core operations and drivers of value creation set out by the IRD are the appropriate basis for determining source, or that the locations in which profits are sourced and business is carried on need necessarily coincide in the context of e-commerce.

The IRD has committed to reviewing its approach next year once the proposals on BEPS 2.0 and the taxation of the digital economy have been finalised.

Positively, the commitment to revisiting the approach shortly appears to demonstrate that the IRD is not considering the implementation of unilateral measures as many other governments have been doing, especially in Europe, and that Hong Kong supports the view that a global consensus-based solution may be the best way to address the tax challenges arising from digitalisation of the economy and foster tax certainty. However, the current core-operations and drivers of value set out by the IRD are heavily focused on operational development and support and we note that the current discussions at the OECD are likely to point towards greater value being attributed to customer locations. While the tests of source of profit and creation of value need not be identical, we would expect the determination of the drivers of profit within the digital economy to be an area of tension and flux over the coming few years.

The Revised DIPN 39 indicates that the IRD had reshaped the profits tax principle to some extent by expanding on the previous emphasis on human presence when it comes to e-commerce. The IRD appears to be adopting a broader perspective by considering any Hong Kong based core operation’s role in a transfer pricing type value creation analysis of the entire business. As such, there is an increasing concern that the IRD may in practice directly apply TP principle to determine profit to be taxed in HK without due consideration of profits tax principle (e.g. source principle). It would be helpful for the IRD to further clarify how the source principle and TP interplay with each other.

The IRD is also silent on when and how additional PE profits should be determined in DAPE situations. There is an expectation from the business community that no additional PE profit should be resulted if the dependent agent has already received an arm’s length service fee from the related party non-resident. We understand that reference can be made to DIPN 60 on DAPE profit attribution issues, and the IRD considers that it is possible that the result from the application of PE profit attribution rule can differ from that of the arm’s length principle under an entity-to-entity context, even before the discussion of BEPS 2.0. For DAPE situations, the IRD would only accept that no additional PE profit (on top of arm’s length TP) would arise if the DAPE does not perform significant people functions on behalf of the non-resident in HK. In this regard, it is suggested that non-residents with potential DAPE arrangements in HK should take this chance to revisit their current arrangement with their dependent agent to mitigate the risk of creating PEs and potential additional taxable profits in HK.

Taxpayers operating in the digital economy space should consider seeking professional assistance to assess and review their current tax position in face of the new local and global developments on this subject.

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia