On 17 January 2020, the Ministry of Finance and State Taxation Administration jointly issued the “Announcement on Individual Income Tax Policy in relation to Overseas Income” (Ministry of Finance and State Taxation Administration Announcement 3 of 2020, hereinafter referred to as "Annoucement 3"). This announcement applies from the 2019 tax year.

Announcement 3 sets out the relevant policies regarding income earned overseas by China tax residents. The key contents include:

- Classification of overseas income

- Calculation of taxable income

- Foreign tax credit (“FTC”) claim

- Administrative requirements

Main contents and our analysis

1. Classification of overseas income

Announcement 3 confirms that the following categories of income are considered as overseas income:

| Income categories | Basis of income sourcing |

|---|---|

| (1) Income from provision of labour services outside China (including employment income and independent personal service income); | The overseas location where the labour or employment activities are carried out. |

| (2) Authors’ remuneration paid and borne by enterprises and other organisations outside China; | The overseas location of the enterprise or organisation which pays and bears the remuneration. |

| (3) Royalties received from the grant of concessions outside China; | The overseas location where the concessions are utilised. |

| (4) Income from business operations and productions outside China; | The overseas location where business operation or production is carried out. |

| (5) Interest and dividend income obtained from enterprises, other organisations and non-resident individuals outside China; | The overseas location where the interest and/or dividend paying parties are based. |

| (6) Income from lease of overseas properties; | The overseas location where the leased property is used. |

| (7) Capital gains from the transfer of real estate, transfer of equity stocks, stock options, or other financial assets (hereinafter referred to as financial assets) of overseas enterprises or other organisations, or from the transfer of other assets outside China; | Real estate: the overseas location where the asset is located; Financial assets: the overseas location where the invested enterprise or other organisation is based. It is worth noting that if more than 50% of the fair value of the assets of the invested enterprise or other organisation comes directly or indirectly from real estate located in China at any time during the three years (36 consecutive months) prior to the transfer, the gains from the transfer of the assets would be deemed as China sourced. |

| (8) Incidental income obtained from enterprises, other organisations and non-resident individuals outside China; | The overseas location where the incidental income paying parties are based. |

| (9) Separate rules may apply if otherwise determined by the Ministry of Finance or the State Taxation Administration. | N/A |

2. Calculation of taxable income

In accordance with the Individual Income Tax (“IIT”) Law and Implementation Rules, resident individuals shall determine their China and overseas sourced taxable income based on the following methods:

- Domestic and foreign income subject to consolidated tax calculation

Comprehensive income1

Annual comprehensive income = comprehensive income within China + comprehensive income from overseas

Income from business operations

Annual operating income = income from domestic operations + income from overseas operations

Losses from business operations in a particular overseas jurisdiction cannot be offset against income from operations in China or other overseas locations. However, the losses may be used to offset business operating income at the same location in future tax years, based on the relevant tax law in China. - Domestic and foreign income subject to separate tax calculation

Income from interests, dividends, property lease, property transfer and incidental income cannot be consolidated with China sourced income and shall be subject to tax calculation separately.

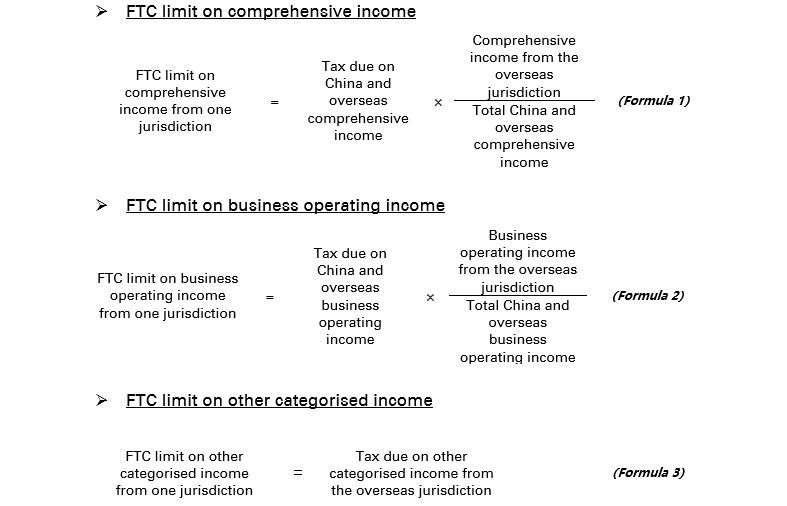

3. Method for calculating credit against foreign taxes

Announcement 3 makes it clear that where resident taxpayers receive overseas income during a tax year, FTC will be granted where foreign income tax has been paid in the overseas location in accordance with the tax law in that jurisdiction, subject to limits. The formula is as follows:

Tax / refund due for the tax year = total tax liability for the tax year – overseas tax liability allowable as credit (not exceeding the tax credit limit)

The amount of overseas tax exceeding the tax credit limit can be utilised in the following five tax years.

FTC limits

In the above formula, the FTC limit is calculated in accordance with (a) the country (region) where income is earned by resident individuals and (b) the category of income, as follows:

The total allowable FTC on income from a particular jurisdiction is the sum of the FTC limits of the various income categories, i.e. the FTC limit on income from a jurisdiction = Formula 1 + Formula 2 + Formula 3

Overseas income not allowable for FTC

At the same time, the announcement further clarifies that FTC is not allowable in the following circumstances, and shall be excluded from the FTC claims:

- Overseas tax paid or collected by mistake;

- Tax which should not be levied in the overseas jurisdiction under the Double Tax Treaty between China and the foreign country (or under the Double Tax Arrangement between Mainland China and Hong Kong and Macao);

- Late payment interest and/or penalties imposed by overseas tax authorities for underpayment or late payment of overseas income tax;

- Overseas income tax which is due for refund or compensation from the overseas tax authorities;

- Overseas income which is tax-exempt under the China IIT Law and Implementation Rules.

Application of concession clause of tax treaties

Concession clauses of a Double Tax Treaty allow FTC to be granted in cases where foreign tax is deemed to be levied even though no foreign tax is due under tax exemption rules of the overseas jurisdiction. Announcement 3 provides that where tax residents receive overseas income which has been subject to tax exemption or reduction in the overseas jurisdiction, the amount of tax exempt or reduced shall be allowed as FTC according to the relevant Double Tax Treaty provisions, and to be included in the FTC claim.

4. Administrative requirements

Overseas income reporting and FTC claims

| Reporting timeline | From 1 March to 30 June following the tax year in which income is received;

|

|---|---|

| Reporting tax bureau | Report to the local in-charge tax bureau where the taxpayer’s employer is based.

|

| Documentation requirements | The following should be provided when filing for FTC claims (unless other rules apply):

|

| Time limits |

|

Tax withholding and reporting requirements for outbound assignees

For tax residents who have been assigned overseas by their employers, remuneration for employment or labour services should be subject to the following withholding rules:

| Income paying or bearing party | Withholding and reporting requirements |

|---|---|

| Sending entity or other China based entity | Tax withholding should be applied by the sending or other entity in China |

| Overseas receiving entity (where taxpayer is assigned to a Chinese overseas entity) | Tax withholding can be operated by the overseas Chinese entity, and tax reporting obligation can be delegated to the sending entity in China. Where no withholding has been applied, the sending entity should report relevant information to the local tax bureau by 28 February following the tax year. The reportable information includes: assignee name, ID number, job title, country (region) or assignment, overseas entity name and address, assignment period, overseas and China sourced income and tax payment details etc. |

| Overseas receiving entity (where taxpayer is assigned to a non-Chinese overseas entity) | The sending entity should report relevant information to the local tax bureau by 28 February following the tax year. The reportable information includes: assignee name, ID number, job title, country (region) or assignment, overseas entity name and address, assignment period, overseas and China sourced income and tax payment details etc. |

Other administrative requirements

Legal obligations

Where taxpayers and withholding agents fail to fulfill the tax reporting and payment obligations as stipulated in Announcement 3, the relevant rules under the Tax Collection and Administration Law of the People's Republic of China and the IIT Law and Implementation Rules will apply. The failures will also be incorporated into the personal tax credit rating system.

Foreign currency conversion

Where the overseas income or overseas tax payment is denoted in a currency other than RMB, in accordance with Article 32 of the Implementation Rules, the taxable income shall be converted into RMB according to the median exchange rate on the last day of the month prior to the month of tax reporting or withholding. While performing the Annual Reconciliation filing, currency conversion calculation should not be repeated where income denominated in foreign currency has already been subject to (monthly/ quarterly/periodic) income reporting during the respective tax year; where additional overseas income is reportable on the Annual Reconciliation, the median exchange rate on the last day of the previous tax year shall apply.

KPMG Observation

Announcement 3 further improves the IIT policy on overseas income received by resident taxpayers, and it clarifies relevant rules on FTC claims and administrative procedures. It complements the recent IIT reform and resolves transitional issues. The following should be noted:

- Clarifying FTC claims on overseas income

The announcement clarifies five situations in which the FTC would not be allowed, including (1) tax paid/collected by mistake; (2) tax refund or compensation; (3) interest and penalties; (4) overseas tax not due under a Double Tax Treaty; and (5) tax-exempt income under China tax law. At the same time, the concession clauses of Double Tax Treaties allow FTC to be claimed on certain income subject to tax exemption or deduction in overseas jurisdictions. The provisions have filled the gaps in the IIT Law regarding FTCs, and provides solutions on a practical level. - Refining overseas income reporting and administrative procedures

The announcement has refined certain details including reporting timeline. The reporting timeline has been set to 1 March – 30 June, which is in line with that of the Annual Reconciliation, which avoids duplication of tax filing and therefore simplifies the reporting process. The announcement also states that where the tax year of the jurisdiction is inconsistent with the calendar year, the corresponding tax year for China tax purposes would be the calendar year in which the last day of the overseas jurisdiction tax year falls, which provides clarity to taxpayers. - Adjusting overseas assignee withholding and reporting mechanism

Withholding and reporting rules for China outbound assignees have also been clarified under this announcement. For domestic organisations which pays or bears the remuneration costs, there will be tax withholding obligations. Where the overseas assignees’ remuneration is paid or borne by an overseas Chinese entity, and that withholding has not been applied, the China domestic entity will be required to report overseas assignee information to the local tax bureau by 28 February following the tax year. As such, businesses are advised to establish internal processes to effectively collect and report relevant outbound assignee information, as well as fulfill withholding obligations, to mitigate any potential risk of non-compliance. - Overseas income received by non-resident individuals

Announcement 3 clarifies the relevant rules for resident taxpayers, but has not provided guidance in respect of non-residents. Under the new IIT Law, non-resident taxpayers are not subject to tax on their overseas income for six years starting from 2019, and so far such income has not been within the scope of taxation. We expect that the tax authorities will publish relevant guidance in due course.

KPMG will continue to closely follow the relevant tax policies on overseas income and proactively discuss policy developments and share our practical experiences with the tax authorities. We welcome organisations and taxpayers to contact us for the latest information on individual taxation.

If you have any questions in the above practices, you are welcome to consult KPMG.

1 According to Article 2 of the IIT Law, comprehensive income consists of employment income, income from independent labour services, authors’ remuneration and royalties.

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia