From insights to opportunities to impact – KPMG’s Global Strategy Group provides new perspectives on how to design and implement strategies that embed the agility, customer-centricity, resilience, and operational excellence needed to thrive in dynamic markets.

Our environment is characterized by fast-changing market conditions and disruptive forces coupled with the accelerated development of new technology. A robust, sustainable and adaptive business strategy needs to incorporate the constantly developing understanding of the power play between innovation, creating, and preserving value.

We help you in navigating challenging financial objectives with the core elements of a sustainable business model and the aspiration of operational excellence.

The Global Strategy Group is KPMG’s strategy consulting arm, seamlessly connected with KPMG’s Audit, Tax/Legal, Deal Advisory and Management Consulting teams – grown from 150 years of history and expertise across all sectors and geographies proven by world class credentials and united by the integrity and credibility of the company’s DNA.

Our solutions: navigating the present, shaping the future

Our complete service offering helps clients define, challenge and achieve their strategies and growth ambitions.

We offer strong specialist assistance in- and outside of deals, from the definition of a company’s growth ambition (organic vs. inorganic) through to evaluation and execution of a transaction and/or strategic transformation.

Transact

Pre- and post-deal strategy consulting for your mergers & acquisitions (M&A) and divestment transactions.

Commercial due diligence

examines a target company’s market and competitive position to challenge its business plan and identify commercial risks as well as potential upsides.

Advanced business planning

supports the development of well-articulated business plans geared towards investors to underline the value and strategic position of a business.

Synergy assessment

quantifies the financial upside of combining two businesses. We provide concrete, tangible value potential and growth opportunities based on proprietary data, benchmarks, and experience from past deals.

Separation due diligence

assesses the operational and financial implications (risks/upsides) of a carve-out – from a seller’s or buyer’s point of view. Examines whether the separation concept is solid in a transaction context and ensures business continuity after closing the deal.

Separation assistance

supports sellers in carve-out situations, by identifying the key entanglements with the group (“separation hotspots”), designing solutions to disentangle them (“standalone target operating model”), and articulating the financial implications of your separation (“standalone cost adjustments”). Our seamlessly integrated cross-functional team – covering functional, tax, legal and regulatory subject matter expertise – also supports the operational planning and implementation of carve-outs from signing to post closing.

Integration assistance

end-to-end support from pre-closing due diligence and strategic planning, through integration blueprint, master planning and Day 1-readiness all the way to post-closing implementation support protecting the value of your deal while limiting the impact on your business-as-usual operations.

Inorganic growth strategy & target search

helps articulate the role of M&A, JVs, and partnerships in the context of your corporate strategy and supports the development of target search criteria and long / short lists of specific acquisition targets.

Value creation

KPMG’s proprietary way of identifying and quantifying value for client transformations, turnarounds and transactions. Bringing together data, insights, and execution capabilities that enable us to prioritize and deliver value quickly and confidently.

Transform

Supporting commercial and operational strategy projects as your transformation partner of choice.

Strategy stress test

independent assessment of your strategy, providing an outside-in view of whether strategic choices are clearly articulated and coherent across all the relevant dimensions of the business and operating model – based on KPMG’s proprietary 9 Levers of Value strategy framework.

Growth strategy

helps identify opportunities for growth, both organic (such as market entry, pricing, etc.) and inorganic (such as M&A, partnerships, JVs), and articulates corresponding strategies for reaching the ambition.

Commercial strategy

assistance to optimize the commercialization of products and services, considering industry-specific characteristics, launch excellence, life cycle management, pricing, customer centricity and other levers.

Operations strategy

transforms a client’s operating model across all functions, from front-to-back office, considering new business models and technologies as well as performance improvement levers.

Corporate strategy

supports the analyses of the “as-is” state, setting an ambition, identifying opportunities for sustainable growth, and formulating a strategy with relevant implementation plans to reach the ambition.

Corporate transformation

assists in optimizing group structures, efficiencies of corporate functions and throughout the value chain, business unit setup and access to (growth) capital.

Value creation

KPMG’s proprietary way of identifying and quantifying value for client transformations, turnarounds and transactions. Bringing together data, insights and execution capabilities that enable us to prioritize and deliver value quickly and confidently.

ESG due diligence

reviews the key risks and upsides of a target company from an environmental (“E”), social (“S”), and governance (“G”) perspective to build a multi-layered picture of the transaction.

ESG strategy

helps corporates to identify material sustainability areas and articulate the ambition for each of these areas (i.e. Where do we stand today? Where do we want to go? How can we get there?).

Decarbonization strategy

supports clients to find a path to decarbonize, from assessing the “as-is” (current carbon footprint of scope 1,2,3 emissions), articulating a science-based target and a pathway to reach the target over time.

Circular economy strategy

helps clients understand and unlock the value of circular economy-based approaches, as a key lever for decarbonization and resource efficiency.

Our approach: focused on value creation, protection and delivery from innovation to results

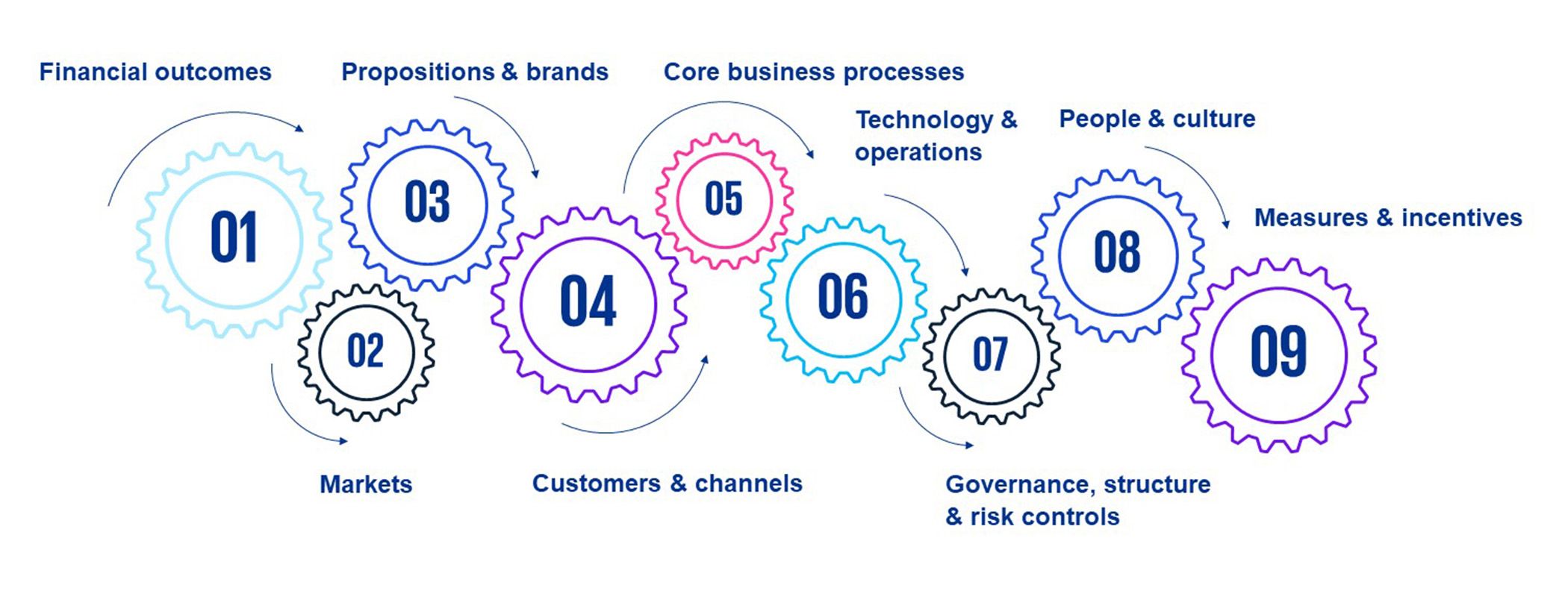

The Global Strategy Group’s proprietary 9 Levers of Value strategy framework represents key elements of a client’s financial, business and operating model that need to be considered when designing and implementing a strategy – be it at the corporate or business unit level.

Whether the client is active on an international or national level, large or small, private, public or not-for-profit, the 9 Levers of Value is a versatile and pragmatic framework to approach strategic challenges.

> Click on the image for more information

Our most recent publications

Our sector expertise

Our solutions are complemented by our sector expertise.

KPMG’s global sector teams have the true local presence, capabilities, and connectivity to help clients in their respective sectors to tackle challenges today and anticipate those of the future.

In Switzerland, the Global Strategy Group team has built dedicated capabilities for these sectors:

Life Sciences

As one of the world’s leading life science hubs, Switzerland boasts one of the highest densities of life science firms in the world.

Due to the importance of this sector to the Swiss economy and the specific challenges faced by the sector, the Global Strategy Group in Switzerland has a dedicated group of life science professionals (i. a. with advanced degrees such as PhDs in molecular sciences and trained doctors) who support start-ups and large multinational life sciences companies in their business decisions.

Consumer & Retail

A global pandemic, significant changes in consumer behavior, supply chain disruptions and competition from new players are just some challenges affecting the consumer and retail sector. Businesses continually review how they operate, broaden the scope of their responsibility and develop new strategies for preserving consumer loyalty.

We assist industry leaders in navigating these disruptions and create tailored solutions serving the purpose of retail companies in the consumer’s daily life.

Luxury

It is more important than ever to understand the luxury market as a whole, including brand, economic systems, and human factors.

We see the luxury industry challenged by technology and sustainability developments from the outside, while talent shift challenges the corporates from the inside. Brands need to reassess their stand in the market and the ways they deliver their promise to customers.

With our strong industry knowledge, we support luxury and fashion brands in building profitable and sustainable businesses.

Industrial Manufacturing

The industrial manufacturing sector in Switzerland is facing multiple key challenges – such as increasing pressure to decarbonize, to (re-)localize supply chains and a general pressure on prices and margins.

We have worked with many leading industrial companies in tackling some of these challenges and finding ways to grow revenue and profit in spite of the challenging circumstances.

> More about our services in industrial manufacturing

> More about our services in automotive

Telecom, Media & Technology (TMT)

The TMT sector has been booming, driven by the unabated continuation of digital adoption by consumers and businesses alike.

We have been supporting leading clients in traditional TMT sub-sectors such as sports rights and marketing as well as in newer and strongly emerging sub-sectors such as cybersecurity services, for example – most frequently with a focus around how to unluck even further growth potential through commercial market and white spot analysis.

> More about our services in technology

> More about our services in media

> More about our services in telecommunication

Key contact persons

We will gladly remain at your disposal to answer further questions you may have.