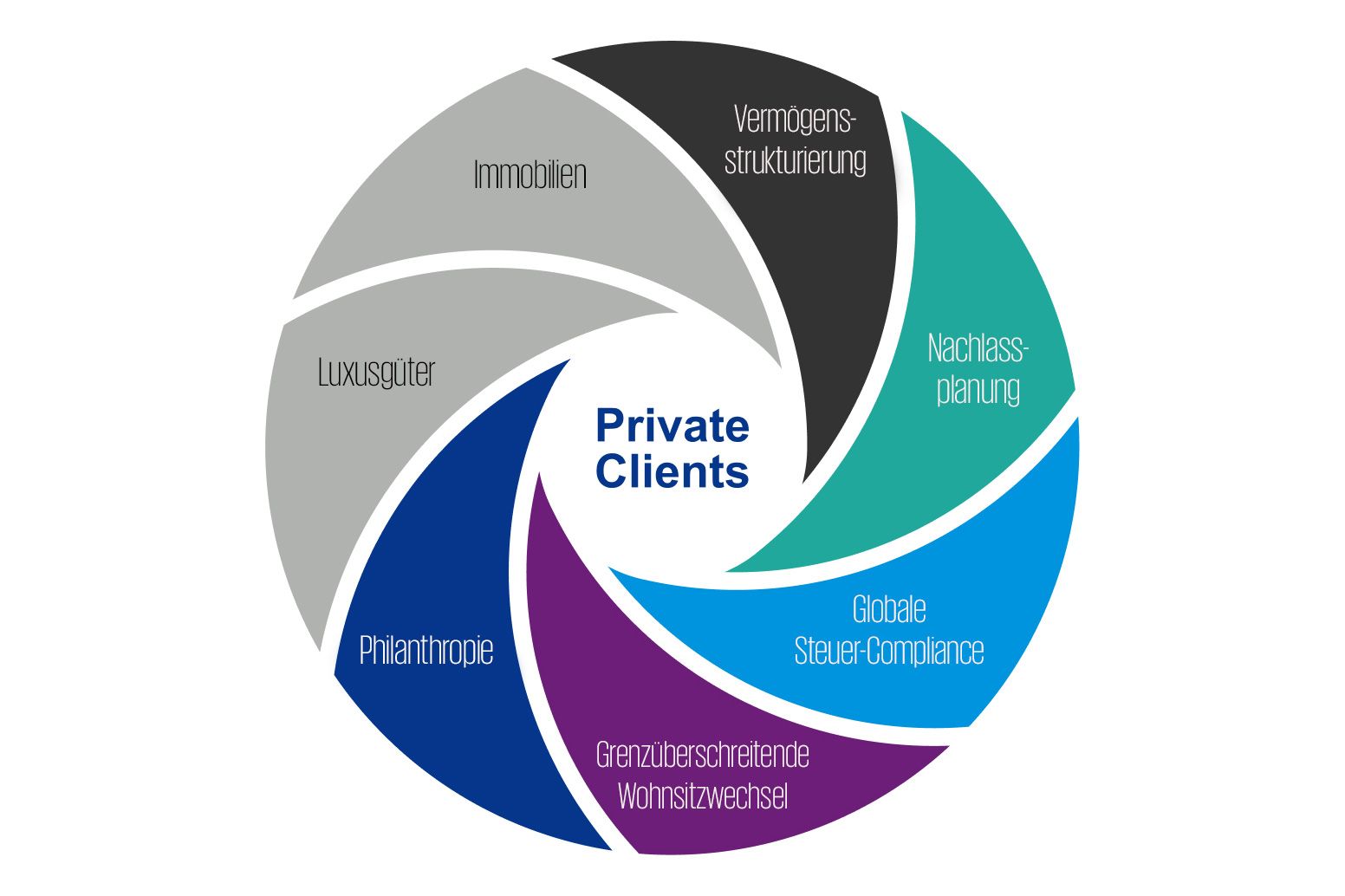

Ihr Vermögen ist einer Vielzahl von Risiken ausgesetzt, die komplex und nicht immer offensichtlich sind. Wenn Sie in mehreren Staaten leben oder geschäftlich tätig sind, gilt es dem Schutz des Vermögens besondere Aufmerksamkeit zu schenken. Aus solchen Risiken können sich schwerwiegende finanzielle Folgen ergeben, welche sich auf Sie, Ihre Familien und Ihre Unternehmen negativ auswirken können.

Das Private Clients Team von KPMG besteht in der Schweiz aus rund 40 Steuerberatern, Anwälten und Finanzexperten, die Sie unterstützen diese Risiken zu identifizieren, zu reduzieren und zu überwachen. Um dies ganzheitlich und auf Ihre Situation zugeschnitten zu tun, können wir nicht nur KPMG-Privatkundenberater in 154 Ländern beiziehen, sondern arbeiten mit einer Vielzahl von Partnern international und lokal zusammen.

So kontaktieren Sie uns

- KPMG Standorte finden kpmg.findOfficeLocations

- kpmg.emailUs

- Social Media @ KPMG kpmg.socialMedia

Unsere Expertise

Als Privatkunde profitieren Sie von KPMG’s multidisziplinärer Expertise in den Bereichen Steuern, Recht, Cyber und Unternehmensberatung. Wir stellen Ihnen unser Wissen und die Erfahrung aus der Zusammenarbeit mit global tätigen Unternehmen zur Verfügung.

Wo immer und wann immer Sie das globale Netzwerk eines Big Four-Unternehmens benötigen, verschaffen wir Ihnen schnellen Zugang zu hochkarätigen Spezialisten, die Sie bei jeglichen Herausforderungen unterstützen.

Unsere Lösungen sind erprobt und werden massgeschneidert, damit sie nicht nur die Bedürfnisse von Privatkunden abdecken, sondern auch deren Unternehmen Rechnung tragen. Deshalb zählen wir zu den von uns betreuten Kunden nicht nur vermögende Privatpersonen, sondern auch Unternehmer und Führungskräfte. Schützen Sie Ihr Vermögen heute und für die nächsten Generationen.

Ihre Ansprechpartner

Für weitere Informationen und Fragen stehen wir Ihnen gerne zur Verfügung.

Erfahren Sie mehr

Family Office & Private Client

KPMG's Team aus Steuerexperten kann Sie in allen Bereichen der Familien- und persönlichen Besteuerung unterstützen.

Family Offices & Private Clients Newsletter

Steuerliche und rechtliche Entwicklungen betreffend Privatpersonen und Family Offices.

KPMG Law

Im heutigen sich rasch wandelnden rechtlichen Umfeld bieten wir mehr als nur zuverlässigen Rat.

Philanthropie: Eine neue Welle?

Erahren Sie mehr über die Trends, welche Philanthropisten in der Zukunft begegnen werden.