On Tuesday, 15 June our webinar on IT Outsourcing and Business Process Outsourcing took place.

During this webinar, our KPMG experts provided insights on:

- Key findings from the Benelux study on the EBA Outsourcing Guidelines;

- The latest trends in digital Outsourcing as well as methodologies for managing the full Outsourcing lifecycle;

- A client case with more information on how KPMG can help in becoming compliant with the EBA Outsourcing Guidelines.

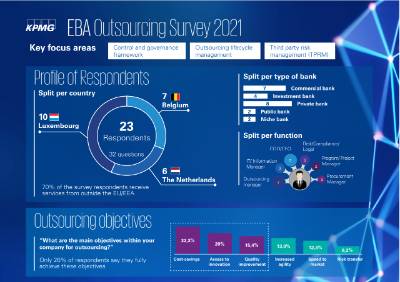

Summary of the KPMG EBA Outsourcing Guidelines Survey 2021

Key take-aways:

- The KPMG EBA Outsourcing Guidelines Survey 2021 was completed by 23 respondents across Belgium, the Netherlands and Luxembourg.

- Only 30% of the respondents feel very confident that their organization is compliant with the EBA Outsourcing Guidelines.

- Cost savings, access to innovation and quality improvement remain key objectives for Outsourcing.

- Banking institutions rely more on Outsourcing for access to new technologies and to deliver key business processes.

- Applying the EBA Outsourcing Guidelines, not just for the sake of regulatory compliance, will increase the effectiveness and added value of Outsourcing arrangements.

- An up to date Outsourcing register and a yearly review of critical and important Outsourcing arrangements provides a valuable source of information for the management body.

- Having enough expertise in-house and sufficient resources to monitor and document all Outsourcing arrangements should not be taken lightly.

- Appointing a single point of contact/Outsourcing manager who is directly reporting to the management body has a positive effect on compliance with the EBA Outsourcing Guidelines.

- Setting up regular/frequent reviews of Outsourcing arrangements on risks, responsibilities, performance and the business case is an effective way to mitigate risks and improve performance.

- A true partnership requires to explicitly manage perceptions about the services contracted, delivered and expected. Diverging perceptions and expectations could potentially derail an outsourcing relationship.

- The complexity of transferring services towards a service provider cannot be underestimated. It needs thorough preparation and a clear division of responsibilities between the financial institution and the service provider.

- Instead of outsourcing labour intensive processes, take into account the possibility to automate these processes. From the perspective of the EBA Outsourcing Guidelines, it also decreases the risk on becoming an empty shell and mitigates dependencies with third parties.

- If for some reason the review of your critical and important Outsourcing arrangements should not be finalised by 31/12/2021, you should inform the competent authority on your plan on how to complete the review or the possible exit strategy.

If you missed the webinar or would like to revisit it, we invite you to watch the recording and download the slides. If you have any further questions or comments, do not hesitate to reach out to the relevant expert listed below.

Relive the webinar

If you missed the webinar or would like to revisit it, we invite you to watch the recording and download the slides. If you have any further questions or comments, do not hesitate to reach out to the relevant expert listed below.

Contact us

Paul Olieman Director – KPMG in Belgium Technology T +32 2 708 41 37 E paulolieman@kpmg.com |

Maarten Visser Manager – KPMG in the Netherlands Digital Sourcing T +31 6 10179830 E visser.maarten@kpmg.nl |