Australian major banks have reported strong financials for the first half of 2023, driven by continued growth of the loan portfolio and improving net interest margins.

While the headline results for the period are positive for the four major banks in Australia, there are early signs of stress in the loan portfolio as a result of the soft economic outlook.

With interest rates elevated, our major banks are seeing a margin benefit, but this is being eroded by a combination of loan pricing competition, funding cost increases and a continued rise in bank costs.

KPMG Major Banks insights

Credit quality remains strong but increasing arrears and provisions signal potential stress ahead.

Credit quality remains sound, with household and business savings buffers and high employment continuing to insulate the Majors’ loan books from any significant stress. However, given the expectation for economic softening, banks should continue to focus on leading credit indicators and early warning signals to identify customers at increasing risk of default.

Where banks have invested in analytics and data capabilities, they may be more aware of the extent of customers’ financial difficulty than the customers themselves. Proactive management and support for customers will be beneficial for the bank and the customer.

We expect that arrears and impairments will start to accelerate over the second half of the year with mortgage arrears following the lead of unsecured products.

Paul Lichtenstein

Partner, Credit Risk Management

KPMG Australia

Bank costs continue to rise, despite heavy investment in digital capabilities.

While cost to income ratios have trended down, actual costs continue to rise caused by higher levels of inflation; higher numbers of staff (and the increasing cost of those staff); and the ongoing cost of risk/regulatory, technology and growth investment.

Banks that make considered strategic decisions to actively reduce costs within their control and minimise ongoing business impost will be best positioned to maintain margins in a retracting economy.

Ben Kilpatrick

Partner, Customer Advisory

KPMG Australia

What will drive success or failure for the Majors?

Banks must now master how to effectively serve and support their customers through a challenging economic environment, whilst continuing to invest in digital transformation to tackle structural cost issues.

These issues are not separate, but fundamentally intertwined. Understanding this and responding to them together is a key way to extract value.

We expect to see divergence in the fortunes of Australian banks as the economy is further challenged. Those who have been courageous in their efforts to tackle these challenges and continue to invest, will have the advantage. The defining factor of success will be how well the banks can tackle these challenges in combination with a long-term, growth mindset versus tactically and focused only on today.

Theo Efthymiou

Partner, Financial Services

KPMG Australia

Results summary

Income

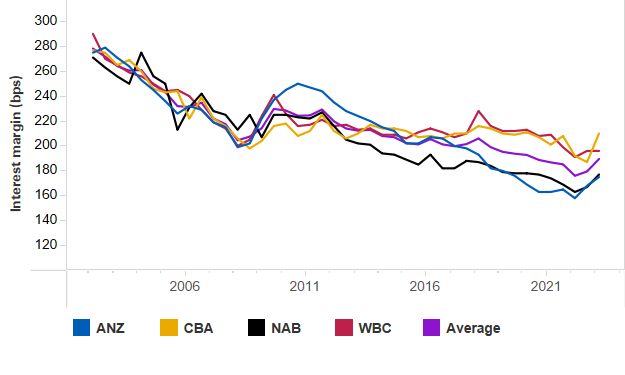

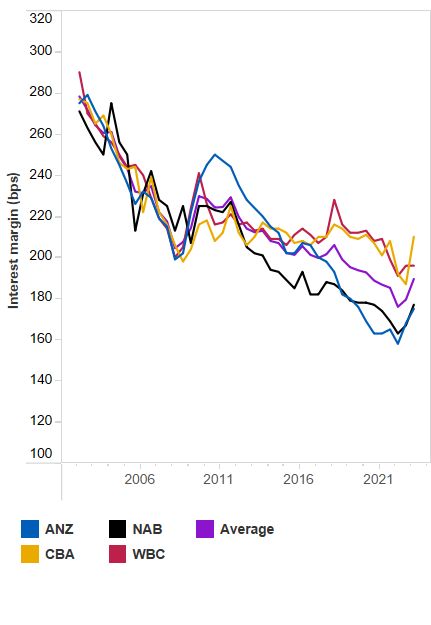

Net interest margins across the four Major Banks continued to increase in 1H23 by an average of 14 basis points compared with 1H22. There was also an increase of 10 basis points compared to 2H22. This is a result of significantly improved interest earned on the loan portfolio on the back of the RBA’s sustained rate increases during the last 12 months. While net interest income has increased by 17% compared to 1H22 to $37.7 billion, interest expense has increased by 430% compared to the same period in 2022.

Average interest earning assets increased by 8.6% from 1H22 to $3.97 billion with all four banks reporting increases. This was primarily driven by above system growth in both mortgages and non-housing (i.e. business and unsecured lending) in the period increasing by 5.0% and 7.8% respectively across all the Major Banks from 1H22.

Net interest margin

Costs

The average cost to income ratio decreased from 49.3 per cent in 1H22 to 44.3 per cent. Overall, however operating expenses have increased by 2.6% compared with 1H22 reflecting an increase in personnel costs and investment spend, although offset by lower remediation costs. Personnel costs increased by $472 million (or 4%) from 1H22, with headcount increasing by 3%. Also of note, technology operating expense has increased by $103 million compared with 1H22 to $3.8 billion with inflation being the key driver.

Investment spending has been relatively stable across all four Australian major banks. However, there has been an overall shift away from risk and compliance investment spend, with an increasing share of investment in productivity and growth initiatives.

Liquidity

Across all our Major Banks, the average Liquidity Coverage Ratio (LCR) decreased to 131.0 per cent, down 100 basis points from 2H22. Although liquidity positions are well above regulatory minimums of 100 percent, the decrease was primarily driven by increased cash flows.

The average CET1 ratio across the four banks has increased by 62 basis points to 12.3 percent from 2H22, showing continual strong capital buffers. The completion of share buy-backs in FY22 drove this increase, with the two of the four Majors collectively completing $1.9 billion of share buy-backs in 1H23, substantially lower than $12.4 billion in 1H22. The average leverage ratio decreased by 8 basis points from 2H22 to 5.2 percent, driven by an increase in exposures due to higher lending volumes.

Liquidity coverage ratio

Asset quality

Average provisions as a percentage of Gross Loans and Advances (GLA) have increased in 1H23 by 1 basis point compared to 2H22 to 0.7 per cent, while the average is 3 basis points lower than 1H22. This is primarily due to a 6.1% increase in the Collective Provision, reflecting ongoing inflationary pressures, rising interest rates and a decline in house prices. 90 day+ delinquencies have also continued to decline.

The four banks booked $1.3 billion in collective impairment charges in 1H23, which is a sharp turnaround from releases in 1H22. The primary factor was the shift from rising house prices in the prior period to falling house prices in 1H23, combined with increases in early arrears. Specific impairment charges of $112 million, down $75 million compared to 1H22, primarily relate to Business and Private Banking, with a small number of impairments.

Provisions as a percentage of Gross Loans and Advances (GLA)

Shareholder returns

Return on Equity (ROE) continued on an upward trend in 1H23 across the Majors. Average ROE increased by 191 basis points compared with 1H22 to 12.6 percent, continuing the momentum from last year's double-digit ROE.

Interim dividend payments across the Majors have increased in 1H23 with the average amount per share rising by 16.5% to 111 cents per share compared to 1H22. The average interim dividend payout ratio decreased by 8 basis points from 1H22 to 65.2 percent.

Return on equity

Major Australian Banks

Download our 9-page summary including results snapshot and KPMG insights.

Download PDF (893KB)