The leases standard (AASB 16) grosses up balance sheets with right-of-use assets and lease liabilities. Here we respond to some common questions relating to the impact of this in performing impairment testing required by AASB 136 Impairment of Assets.

1. Is the ROU asset included in the carrying amount of a CGU?

Right-of-use (ROU) assets are generally included in the carrying amount of a CGU as they generate cash inflows only in combination with other assets. Where this is not the case, ROU assets should be tested for impairment individually.

2. Is the lease liability included in the carrying amount of a CGU?

As with other liabilities, the lease liability is only included in the carrying amount of a CGU if a buyer would be required to assume that lease liability on disposal of that CGU. Some factors to consider when assessing whether a buyer would assume the lease liability on disposal of the CGU could include:

- Legal composition of the CGU – disposal of a CGU which is also a legal entity may help support that a buyer would take over the lease

- Strategic importance of the underlying asset – a buyer may require the transfer of a lease when that asset is key to the operations of the CGU; and

- Contractual terms of the lease arrangement – clauses which contemplate assignment of the lease and associated approvals shall be considered.

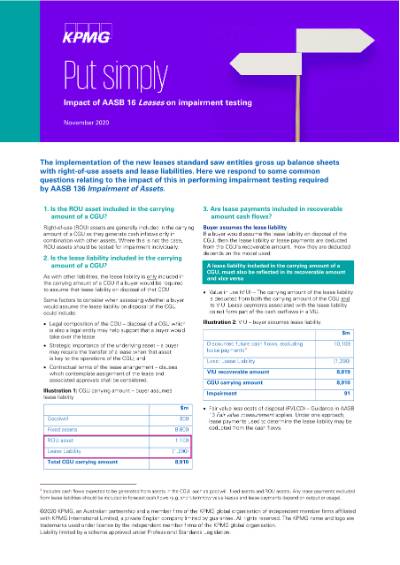

3. Are lease payments included in recoverable amount cash flows?

Buyer assumes the lease liability

If a buyer would assume the lease liability on disposal of the CGU, then the lease liability or lease payments are deducted from the CGU’s recoverable amount. How they are deducted depends on the model used:

- Value in use (VIU) – The carrying amount of the lease liability is deducted from both the carrying amount of the CGU and its VIU. Lease payments associated with the lease liability do not form part of the cash outflows in a VIU.

- Fair value less costs of disposal (FVLCD) – Guidance in AASB 13 Fair value measurement applies. Under one approach, lease payments used to determine the lease liability may be deducted from the cash flows.

Buyer does not assume the lease liability

If a buyer would not assume the lease liability on disposal of the CGU, for both VIU and FVLCD approaches, lease payments associated with that lease liability are not deducted from the recoverable amount cash flows.

4. What is the impact of lease term on forecast cash flows and terminal value?

When the lease term is shorter than the forecast period for the CGU and the operations of the CGU are dependent on the continued use of the underlying asset or a similar asset, the replacement of the lease through a new lease arrangement or acquisition is included in the cash flows.

- If the lease term ends prior to the terminal value year, lease replacement cash flows are included in all forecast periods after the lease ends, including the terminal year.

- If the lease term ends after the terminal value year, the terminal year includes lease replacement cash flows. In addition, adjustments to the terminal value are required to eliminate double counting of the lease in the years before the lease ends.

5. How is the recoverable amount of an ROU asset determined when allocating impairment expense within a CGU?

When allocating impairment across assets in a CGU on a pro-rata basis, the carrying amount of an individual asset cannot be reduced below the higher of its recoverable amount and zero. This rule applies equally to any ROU assets within the CGU.

FVLCD is one possible method that can be used to determine the recoverable amount of a ROU asset that forms part of a CGU. One possible way to determine the FVLCD of this asset is by reference to the present value of amounts a market participant would pay to lease the underlying asset using market lease rates.

In our view, this approach can be applied for ROU assets irrespective of whether the lease contract permits subleasing. However, restrictions relating to the use of the asset, for example zoning regulations, should be considered when determining market rent.