A formal appointment, whether it is a voluntary administration, liquidation or receivership is required to follow processes and time-lines governed by legislation. This section provides background information on the three key formal insolvency pathways as well as information for creditors on all current appointments.

Select an option to find out more.

- Voluntary Administration

- Liquidation

- Receivership

A Voluntary Administration (VA) is a flexible option available to directors and secured creditors to restructure a company. The process is governed by the Corporations Act 2001 Cth (the Act).

The overall objective of the process is to administer the affairs of the company in a way that results in a better return to creditors than they would have received if the company had been placed directly into liquidation. Where it is possible to restructure the company or its underlying businesses, the mechanism for achieving this is a Deed of Company Arrangement (DOCA).

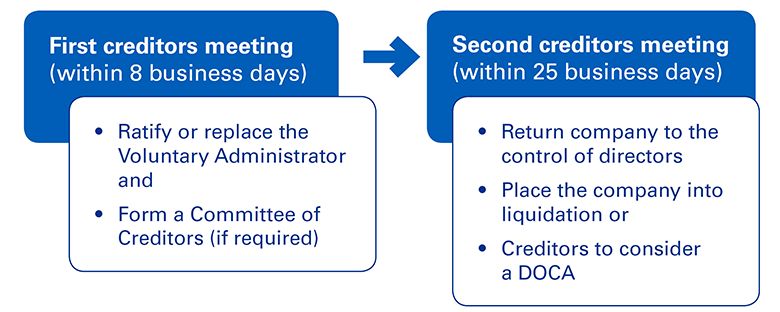

The VA process is time driven and there is a relatively short timeframe for the potential restructure of the company, unless creditor or Court approval is given to extend the convening period under the VA.

What does a VA do?

After the appointment of the VA, control of the company's business and assets is transferred to the VA and the powers of the company's directors are suspended.

The VA take control of the company and its affairs, investigate the Company's business, property, affairs and financial circumstances to develop a proposal and in the majority of cases concurrently explore the commercial merits of divesting the Company's assets. In doing so, the VA attempts to determine the best solution to the company's problems and compares the possible outcomes of the proposals with the likely outcome in a liquidation.

Issues to be considered in respect of any restructuring strategy include:

- impact on key contracts to enable operations to continue

- legislative or government approvals if required

- creditor support

- asset preservation and security

- timing of implementation and cost of any proposed restructure

- ongoing employee and supplier support

- funding requirements.

The VA must then convene a meeting of the company's creditors to enable them to consider the VA's recommendations for the future of the company and then decide whether to:

- end the VA and return the company to the directors' control (uncommon)

- approve a DOCA which dictates the terms and conditions of any restructure and/or sale as well as the return to the various classes or stakeholders, or

- wind up the company and appoint a liquidator.

Effect of the appointment

The effect of the appointment of a VA is to provide the company with time within which the stakeholders can determine the company's future. While the company is in VA:

- unsecured creditors cannot begin, continue or enforce their claims against the company without the Administrator's consent or the Court's permission

- owners of property (other than perishable property) used or occupied by the company, or people who lease such property to the company, cannot recover their property

- except in limited circumstances, secured creditors cannot enforce their security over company property

- a Court application to put the company in liquidation cannot be commenced

- a creditor holding a personal guarantee from the company's director or other person cannot act under the personal guarantee without the Court's consent.

Liquidation is the orderly winding up of a company's affairs. It involves realising the company's assets, cessation or trade and sale of its operations, distributing the proceeds of realisation among its creditors and distributing any surplus among its shareholders. There are four principal forms of liquidation:

- Provisional Liquidation – an interim procedure aimed at preserving the status quo until the Court determines the future of the company.

- Court Liquidation – starts as a result of a court order following an application made to the court, usually by a creditor to wind up the company.

- Creditors' Voluntary Liquidation – initiated by the company in circumstances where the company is insolvent.

- Members' Voluntary Liquidation – wind up of a solvent entity initiated by the company or its members.

What does a liquidator do?

The Liquidator's role generally is to:

- collect, protect and realise the company's assets. The outcome of this process, will directly affect the ultimate recovery by creditors, and in the case of a surplus, by members

- investigate and report to creditors about the company's affairs, including any potential antecedent transactions, such as unfair preference payments which may be recoverable, any uncommercial transactions which may be set aside, any unfair loans which may be recovered and any possible claims against the officers of the company for unreasonable director-related transactions or insolvent trading

- enquire into the failure of the company and possible offences by people involved with the company and report to ASIC

- after payment of the costs of the liquidation, and subject to the rights of any secured creditor, distribute the proceeds of realisation – first to priority creditors, including employees, and then to unsecured creditors.

Effect of appointment

Control of the company's assets, conduct of any business and any other affairs transfer to the Liquidator. The directors cease to have any authority to act and all dealings must be undertaken by the Liquidator.

The Liquidator has full authority to conduct and sell any business in the name of the company. The Liquidator will dispose of the company's assets and distribute the proceeds of the sale to proven creditors.

The rights of secured creditors are not affected by the liquidation and they are able to recover assets subject to their security. The secured creditor may prove in the liquidation for any shortfall after their security has been realised.

All proceedings against the company are stayed and cannot continue without the written consent of the Liquidator or leave of the Court. Creditors lose their rights to recover debts directly from the company, but are able to prove their debts and share in any distribution made by the Liquidator.

A Receiver may be appointed by a secured creditor, or in special circumstances by the Court, to take control of the assets that are the subject of the security.

The charge, or security, held by the secured creditor under which the appointment of a Receiver is made may comprise:

- a non-circulating security interest (fixed charge) over particular assets of the company (e.g. land, plant and equipment); and/or

- a circulating security interest (floating charge) over assets that are used and disposed of in the course of normal trading operations (e.g. debtors, cash and stock).

The powers of the Receiver are governed by the charge document and Corporations Act 2001 Cth (the Act).

If a Receiver has, under the terms of their appointment, the power to manage the company's affairs, they are known as a Receiver and Manager.

What does a receiver do?

The Receiver's role is to:

- collect and sell enough of the charged assets to repay the debt owed to the secured creditor (this may include selling assets or the company's business)

- pay out the money collected in the order required by law, and

- report to ASIC any possible offences or other irregular matters they may be uncover during their control of the company.

Effect of appointment

The Receiver and Manager will have control over the company's assets to which the appointment has been made, in accordance with the security documentation and reports directly to the secured lenders. A Receiver and Manager does not have a statutory reporting obligation to all stakeholders, nor does it need to conduct detailed investigations of a statutory manner under the Act unless it is apparent that people associated with the company may have breached provisions of the Act.

Unlike a VA process there is no freezing of unsecured creditors' debts during the receivership process and whilst there is no obligation on the Receiver and Manager to make payment of those unsecured claims, creditors may take action to wind up the company.

The Receivership has the primary aim of dealing with the assets and undertakings of the company the subject of the appointment to repay monies owed to the secured creditor.